It has been an interesting year. On one hand, a lot of dirt has been cast about and many of us are feeling just a bit covered in it all. On the other, a lot of seeds have been planted. A few have already started to sprout. It’s a good time to have a look back over the blog this past year and see where we’ve been.

Month: December 2017

Having a Laff

The Sunday Times has published a hack-job of a piece attacking the Scottish Government’s proposed plans to change the rates and bands of income tax in Scotland.

They’ve clearly tried to use the Scottish Conservative’s current favourite economic soundbite, the Laffer Curve, to try to build their case that we should be cutting taxes and have sought out a quote from the originator of the idea to try to back it up.

The problem is, I’m not entirely sure that the paper really understands what this idea actually says about tax.

The Scottish Budget 2017

“70% of taxpayers get a tax cut as a result of yesterday’s budget” – Nicola Sturgeon

“One million Scots to pay more income tax than rest of UK” – The Scotsman

Yesterday saw the unveiling of the first draft of the Scottish budget for 2018-19. You can read the proposals by clicking here or on the graphic below.

My own brief comments have already been published via Common Weal and in The National but I wanted to expand on a few of the points here too.

Income Tax

Of course, this is the big headline grabbing policy change. Last year was the first year that Scotland had the power to adjust rates and bands of income tax and it used those powers then to not uplift the Higher Rate by inflation as was done in the rest of the UK. Cue howls of outrage from the Tories that for folk earning more than £44,000 per year, Scotland was now the “highest taxed part of the UK”.

This year, the Scottish government spend a good deal of time consulting with the other parties about their proposals for what to do next with income tax as well as offering several options of their own.

In the end, the government has written their budget around a plan which doesn’t quite look like any of the proposals brought up before. From next year, Scotland’s income tax bands will change from this

| Income up to | Tax Rate |

| £11,500 | 0% |

| £43,000 | 20% |

| £150,000 | 40% |

| >£150,000 | 45% |

to this

| Income up to | Tax Rate |

| £11,850 | 0% |

| £13,850 | 19% |

| £24,000 | 20% |

| £44,273 | 21% |

| £150,000 | 41% |

| >£150,000 | 46% |

Two new bands have been added – one “Starter Rate” on income between £11,850 and £13,850 which offers a 1% tax cut and one on income between £24,000 and £44,273 which offers a 1% tax rise compared to last year – and the Higher and Additional rates have been increased by 1%.

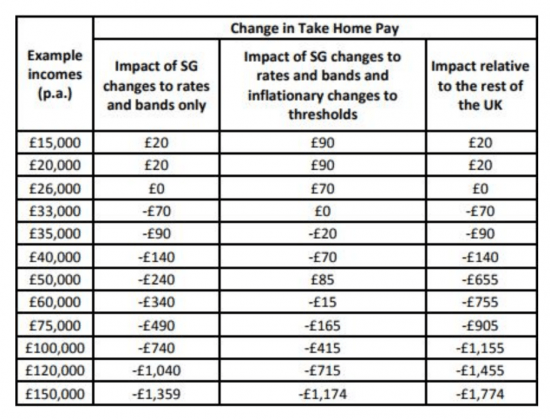

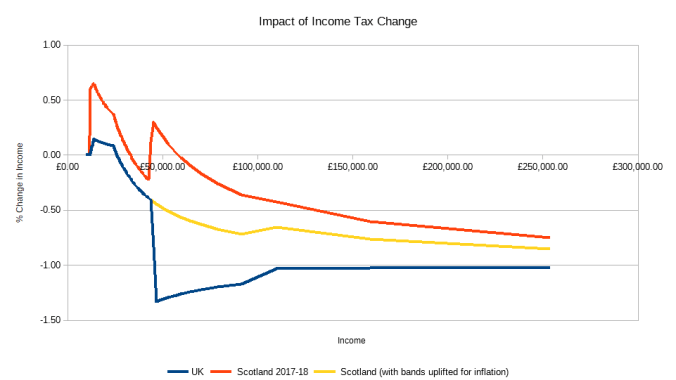

Folk online have been arguing about who will be better or worse off under this plan. The truth is, it depends on what you’re comparing to. You could compare to the Scottish tax rates last year. You could uplift the bands by inflation and leave the rates as they were last year or you could compare to the 2018-19 UK rates.

At my most cynical, I can see immediately that the comparison to the rest of the UK gives the Scottish Government a soundbite with which to counter the Tories. For folk earning less than £26,000 per year, Scotland now has the lowest income tax rate in the UK.

These changes are quite small though. Only about 1% up or down across the income scale. The overall changes are projected to bring in only about an extra £160 million per year and greater increases in the upper rates were ruled out for fears that those on higher incomes would leave Scotland or otherwise evade or avoid the tax increase. This idea is, of course, subject to a great deal of dispute by the various parties.

There is substantial evidence that tax does not cause a great deal of migration across borders. The rich are people with friends, families and connections to the place they live just as much as everyone else.

On the other hand, the frankly Byzantine tax code in the UK does make it easy to move money around so the experience of other states and countries may not reflect onto Scotland and the data about upper income tax flight in the UK is very limited (see from 50min in the video above and from 56min for information about Scotland). The bold might say that there’s only one way to find out…

Far more important than the actual revenue impact of the income tax changes is the willingness to change itself. Scotland now has a more progressive tax system than the rest of the UK and has now set a precedent for adjusting tax to suit the needs of Scotland rather than to just constantly look over the shoulder at what the UK is doing. It will be interesting to see how this idea beds in and develops in coming years.

It remains a shame that Scotland still can’t have a comprehensive discussion about taxation and we’re reduced to either lumping everything on income tax or tinkering around with the more minor devolved taxes. I’ve spoken at length about the Air Departure Tax but even I can’t work up much excitement about the prospect of radical change to the Aggregate Levy.

Public Sector Pay

There was a pleasant addition to the budget here. After years of pay being capped at 1%, public sector workers will be getting a pay increase of 3% if they earn less than £30,000 per year, 2% if they earn less than £80,000 per year and a flat increase of £1,600 if they earn more than that.

Of course, their taxes are likely to be changing too but only if said worker is earning in the region of £170,000 or more would the increase to their taxes exceed their pay rise (and I’m reasonably certain that there won’t be too many in that position).

This is welcome news although it should be tempered by the fact that inflation is now running at 3.1% and rising. This pay increase still represents a wage squeeze for public sector workers and doesn’t even begin to start undoing the damage caused by the years of the cap. This increase certainly isn’t news to be condemned but it’s still not much more than a short term salve.

Housing

The housing policies in the budget don’t seem to be making too many waves. There’s extra money for housing but a good deal of it seems to be aimed at the private market which has already been the recipient of substantial subsidy.

The proposal to cut the Land and Buildings Transaction Tax for first-time buyers is a major error of judgment. Unlike the divergence with the rest of the UK on income tax, this proposal is a mirroring of the UK policy. Under this cut, 80% of first-time buyers will no longer pay LBTT on properties priced below the threshold. At least they recognised the lower house prices in Scotland and set the threshold at £175,000 instead of the UK’s threshold of £300,000.

But the logic of the tax relief is similarly misplaced though. If you can afford a house at £175,000 without the tax relief, you can afford the house with it. But if you can’t afford the house at £175,000 then it’s very unlikely that a £600 discount is going to make any difference.

This means that there is absolutely no barrier at all to the seller increasing the price of the house by £600 and swallowing up the tax. This cut will merely cause £5 – £7 million per year worth of tax revenue to transfer to those who are selling property.

Regional Council Funding

When the UK budget came out last month and we were told by Westminster that the Scottish government was gaining money in the capital budget but losing it in the revenue budget but if the Scottish Government wanted to make up the different by raising taxes then it was absolutely free to either do so otherwise it could take responsibility for passing on the cuts.

Well, this same rhetoric appears to have been repeated from the Scottish Government with regard to our regional councils. Their revenue budgets will be frozen in cash terms but with inflation running at 3% this means quite a substantial real terms cut. In addition, the public sector pay increase will likely have to come out of that regional authority resource budget which will further increase pressure on councils. The have the “freedom” to increase council tax to make up the shortfall but it remains to be seen how many choose to do so, especially now with every council in Scotland governed by coalitions of various stripes.

This is the area where I expect most of the fighting to occur during the negotiations before the budget is actually voted on in Parliament next year. The SNP can’t pass it on their own. They’re going to need another party to either vote for it or at the very least abstain to get it through.

The Greens were fairly enthusiastic about the approach to income tax but have set this funding freeze as a red line against their support for the budget as a whole. I don’t believe the Lib Dems are any happier with it and with the Tories certain to oppose and Labour not much less so, there’s going to be a bit of trading required to gain enough support to pass the final bill. I wouldn’t be surprised if Derek Mackay has another rummage down the back of the sofa for some extra cash as he did last year.

One more radical solution would be to recognise that wealth inequality is far higher in Scotland than income inequality and that maybe it is time to explore news forms of local taxation like local land taxes or other taxes on wealth.

Scottish National Investment Bank

Now here is a real good news story. The SNIB is on its way! The first two year tranche of funding, totaling £340 million, has been included in this budget as has the planning and infrastructure to continue that funding beyond the first two years. The Common Weal plan called for the bank to be capitalised to a total of £2 billion over several years so this is a very good first step. If we were a fully sovereign nation with full control over monetary policy it would, of course, be trivial to fully capitalise this bank but we’re not and Scotland only has limited capital spending powers so we need to build up the funds over several years. This is fine though, the bank still needs to be set up and ramped into operation anyway.

The bank is still in the very early planning stages but discussions with the government about its design and the need for it to look out for the common good have been received very positively.

In the long term, this bank will be a major factor in supporting local economies and helping Scotland’s overall economy remain flexible and adaptable in a rapidly changing world. This, if we stick at it and do it right, could be the most transformational policy of the decade.

Conclusion

In terms of political maneuvering, this budget sent out many of the right signals. Increased progressiveness on taxes, more money for public sector workers, the start of better economic investment. They are all good moves and show a willingness for Scotland to not just be different from the rest of the UK but for Scotland to be Scotland without having to compare itself to the UK in the same way that the UK doesn’t constant compare itself to Ireland or France when setting budgets.

But, and it is a big but, many of changes aren’t themselves going to do all that much. A <1% change in take home pay isn’t going to save the day or break the bank for many folk.

As a stepping stone though? As a definite signal that Scotland is willing to be better? I’ll take that. Let’s try to build on it next year and beyond.

![]()

Banking For Scotland

“We need a banking system that is built on trust from customers which comes from banks which care about their customers.” – Common Weal Key Ideas

Image: The National. Of course, Central Banks are a bit different from the topic of this article.

The news the closure of 1 in 4 RBS branches across Scotland is coupled with the now grimly ironic relaunch of their “Royal Bank for Scotland” advert. Once again, this bank, like others before it, is withdrawing its physical presence from many areas of the country and, as before, it cites the rise of online banking as the principal reason.

1 in 4 branches might not sound too bad to some. It might sound largely bearable. But this figure doesn’t account for regional disparities. For example, of the ten RBS branches within 25km of where I live, eight of them are now scheduled to close.

There will be places, particularly in rural Scotland, where the loss of their branch will result in the total loss of all physical banks in their community.

It is true that many people now do their day-to-day banking online but for those who don’t, this may be devastating news.

Perhaps more importantly than personal banking will be the loss of business banking services. Many small businesses require access to banks on a daily basis, particularly if they handle cash. This move, compounded with others like it past and future, may cause significant harm to the Scottish SME ecology.

Once again, the losses incurred during RBS’s casino banking glut have infected the real economy and, once again, we cannot hope to see the kind of bail-out that they were given.

Which brings up a point. RBS is more than 70% owned by the UK Government. What part have they played in these closures? Probably very little. As far as I can see, the strategy of the UK Government towards the nationalised banks has been to do absolutely nothing with them – to just let them keep doing what they would have done had they never been nationalised – and then to sell them off again.

A sensible and forward thinking government would have taken a far more proactive role in actually using its majority stake in the company. I’m not saying it would have been easy given the underlying structural issues within RBS – this is a bank which used to deliberately bankrupt small companies so that it could make a profit on seized assets – but if the UK Government had had the will to do so, it could have transformed the company into a network of local and regional banks which just solely focused on the business of providing deposits, credit and cash handling services. It could have dispensed entirely with the arcane financial shenanigans which have nearly crippled the country’s economy and could have become a very stable, very successful (if not quite so overtly profitable), “boring bank“.

Many folk will still remember how banking used to be. How you knew your bank manager and they knew better than almost anyone save yourself your business and your financial circumstances. They knew when a loan would be good for you or when it would be a burden. These things cannot be replicated via an automated helpline on a website or by an ever more complex next of “financial products” which are often more about extracting profits from you rather than supporting your business. The idea that you could become the product – to be sold and traded at the banks whim – would be utterly alien to such a system.

Of course, the UK Government isn’t going to do this. Financial gambling is just about the only thing that they have left in their economic strategy so they’re not going to say anything against it. I’m not sure if the Scottish Government has the powers to do so but it should certainly look into the possibility of setting up or encouraging the founding of a “boring bank” network – separate from but working mutually alongside the local development wings of a Scottish National Investment Bank.

Do this we’ll have a bank for Scotland. Till then, I fear that we’ll just be days or weeks or months away from another round of closures and “efficiency measures” which will be about pleasing shareholders or preparing for the next round of “investment opportunities” than it will be about actually supporting local economies and local customers.

![]()