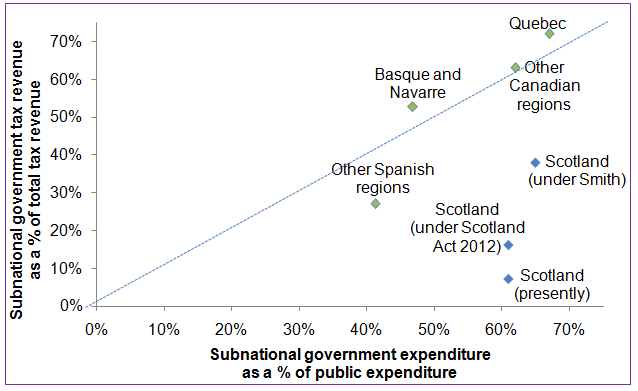

A comparison of the % of devolved control in Scotland now, as it will be under the Scotland Act 2012 and under Smith Commission recommendations as well as a comparison with Spain and Canada. Source: Scottish Government.

Monday the 9th of November saw the Scotland Bill 2015 make a further step towards completion. This Bill, which has been the result of the aftermath of the 2014 independence referendum, will mark another milestone on the devolution “journey” Scotland is traveling upon.

Some of the commentary both during the actual debate in the House of Commons and in the days since have shown considerable confusion at just how the system of devolution in the UK works at the moment and how it is to change with the implementation of the Bill. Before we really settle into a meaningful debate on whether or not any “additional powers” for Scotland will be to and for Scotland’s benefit we need to actually understand what those new powers are, what we have now and how they can be used.

This article shall focus on the powers over taxation devolved to the Scottish Parliament as this area will be undergoing several rapid changes over the next few years and much of the confusion amongst members of the public has arisen from the conflation of several phases of devolution.

One must understand the rather unplanned and piecemeal nature of the progression of devolution for Scotland, there is certainly no clear “destination” to that “journey”, and this reflects and contributes to the confusion but there are three major points in the form of the Scotland Act 1998 which formed the Scottish Parliament after the success of 1997 Devolution Referendum; the Scotland Act 2012 which resulted from the 2007 Calman Commission and the aforementioned Scotland Act 2015 resulting from the Smith Commission of 2014.

The Scotland Act 1998 to Present

Revenue from all taxation gathered in Scotland. Source: GERS 2014-15

In 1997 the people of Scotland voted, by substantial majority, for the creation of a Scottish Parliament with tax-varying powers. The Scotland Act of 1998 which followed led to the creation of that Parliament and the Scottish Executive (later renamed the Scottish Government) and bestowed upon it several powers of legal competence in many areas of government but only very limited powers over taxation. Specifically, the act devolved three areas of tax varying powers to Scotland.

1) The local Council Tax, which since 1993 has been controlled by individual local councils, would remain at a local level but oversight of the tax would transfer from the Scotland Office to the Scottish Parliament.

2) Non-Domestic Rates, or Business Rates, would be devolved in full.

3) The ability to adjust the basic rate of income tax by plus or minus 3p in the pound was granted under powers known as the Scottish Variable Rate (informally portrayed by some as the “Tartan Tax”).

Using the 2013-14 figures from GERS as shown above, these powers of taxation amounted to around £5 billion worth of revenue (assuming the full 3p SVR was applied and collected and that no change was made to NDR or Council Tax) which represents less than 10% of the tax collected in Scotland.

Further, significant issues have been raised with both the Council Tax and the SVR.

The Council Tax is largely considered to have been a fudge put in place in the aftermath of the Poll Tax. It is only marginally more progressive than the flat Poll Tax it replaced; no matter how large your mansion is or how vast your income, you’ll never pay more than three times the rate of the cheapest bedsit. The Scottish Government did, in 2009, look into replacing the Council Tax with a flat rate income tax of 3p in the pound (distinct from the SVR) but this plan was blocked by warnings from HMRC over issues surrounding collecting and distributing the tax as well as a view that it was stripping local councils of their locally controlled power. Whilst the argument over local taxation is still very much ongoing, with a variety of options including local property taxes, local income taxes and land value taxes being mooted. A white paper in 2006, linked to here and pretty much a must read for anyone interested in the topic, came to the conclusion that many local councils around the world are, in fact, in control of many of these forms of taxation simultaneously and no single tax is likely to fulfill all functions adequately. The exact blend of taxation to be used in the future will, of course, become a motion of great interest for each of the political parties seeking election in Scotland in coming years.

[The Scottish Greens preferentially favour the Land Value Tax as a means of breaking up Scotland’s iniquitous distribution of land ownership.]

The Scottish Variable Rate is the one of the three areas of devolved taxation to have never actually been employed. The one attempt to do so was the SNP’s 1999 push to counter Gordon Brown’s basic rate reduction from 23% to 22% in their “Penny for Scotland” campaign. It was roundly seen as a disaster for the party and was later dropped. The major problem with the SVR is that it is an unprogressive addition to what is supposed to be a progressive tax. The Scottish Government must apply the tax to all bands of taxation equally. It could not, for example, apply a -1p rate to the lower bands and a +1p rate to the higher rate bands. The rate also would not apply to certain areas of income such as interest and dividends.

Further, it was found in 2010 that the lack of use of the Rate had led to HMRC removing the infrastructure to apply it from as early as 2000. Despite the promise of the power in 1998, it turned out that the actual practical ability to use it had never been maintained by Westminster.

In effect, therefore, the Scottish Government only actually, practically, had effective control over only a fragment of total revenue gathered within Scotland and even those powers have come with tight limits and caveats.

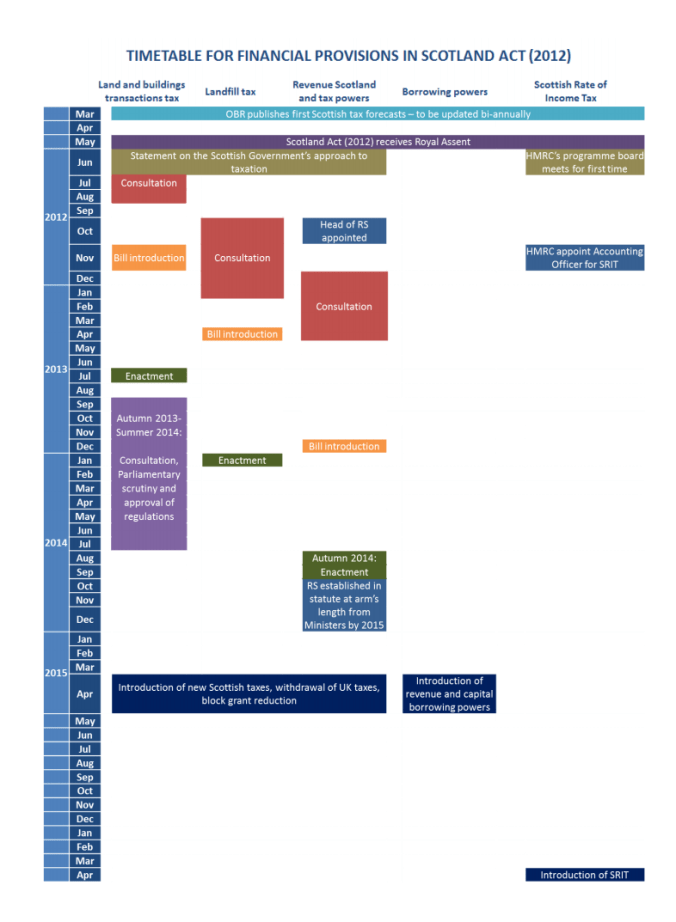

The Scotland Act 2012 – Available from April 2016

The proposed timetable of the implementation of financial powers outlined in the Scotland Act 2012. Source: Scotland Act 2012: Financial Provisions

In 2007, in the wake of the elections which heralded the SNP minority government, the now Opposition Labour party successfully won a motion to establish the Calman Commission which held its first meeting in March 2008 and filed its final report in June 2009. The Scotland Act 2012 implemented most (but not all) of these recommendations and the tax specific powers are due to come into force by April 2016, eight years after the Commission held its first meeting.

In terms of tax powers, this Bill shall expand the Scottish Government’s list of levers by some way. Several relatively minor taxes shall be devolved, notably the Land and Buildings Transaction Tax (which replaces the UK Stamp Duty Land Tax) and Landfill Tax. The Aggregates Levy (a tax on mining, quarrying and dredging sand, gravel and rock or from importing the same) shall also be devolved at some future date when legal issues are resolved. These taxes combined represent around £800 million worth of revenue or an additional 1.5% of the tax revenue raised in Scotland. Additionally, a new tax office, Revenue Scotland, was set up to administrate some of the new devolved powers.

Slightly more importantly, however, than the amount of revenue generated is the ability to shape and reshape our country (in however slight a manner) as we see fit. The LBTT is probably the most powerful of these as it allows Scotland to set taxes on housing and house trading to better fit the market Scotland both has and desires rather than being pulled along by the London housing bubble. There is probably also scope within Landfill taxes and the Aggregates Levy to help encourage recycling, reduce waste and environmental degradation and to generally make Scotland a nicer, healthier place to live.

The major new change in taxation will be the abolition of the abovementioned Scottish Variable Rate and the introduction of its replacement the Scottish Rate of Income Tax (SRIT). This will be administered in a slightly different and more complicated manner than the previous SVR but will allow the Scottish Government to vary the tax rate by up to 10p in the pound above or below the rate set by Westminster.

Crucially though, this tax provision doesn’t materially change the situation from the days of the SVR. The tax will still be collected by HMRC. Westminster will still set the rates and bands (as well as the zero rate Personal Allowance) and, very importantly, Westminster will still control the definition of “income”. Other than going into some more specific detail about defining who is and is not a “Scottish taxpayer” the SRIT is, quite frankly, just as useless as was SVR. The Scottish Government will still not be able to make our income tax system more or less proportional according to our needs and demands and we shall still have to deal with possible ideological conflicts from Westminster over the importance of the Personal Allowance and just what income actually means.

Under this scheme, the Scottish Parliament would now control something in the region of £9.7 billion worth of Scotland’s approximately £54 billion worth of tax revenue. Just 18% of our tax base. This comes also with no power over many of the actual levers of economic control such as VAT, corporation tax, fuel duty, National Insurance or alcohol and tobacco levies.

A Summary of the changes in taxation due to the Scotland Act 2012 Source: Scotland Act 2012: Financial Provisions.

It’s worth noting as an aside that the Scotland Act 2012 also devolved several non-tax related powers such as the provisions over air guns and technical issues surrounding the running of the Scottish Parliament.

There was also the provision put in place to allow the Scottish Government to borrow up to £2 billion per year for capital projects.

One humourous example though stems from the manner in which devolution was set up in the first place. Rather than Westminster specifically denoting which powers are to be devolved, when the Scottish Parliament was set up it was under the conditions that Westminster devolved ALL power to Scotland and then specifically denoted which powers were to be reserved.

A major oversight took place during this process. It was noticed in 2012 that the UK’s territorial claims over Antarctica were omitted from the reserved powers list. Scotland had been granted full control over 660,000 square miles of the icy continent by mistake. The 2012 Act re-reserved this claim.

The Scotland Act 2015 – Currently being negotiated. Available circa 2018

Which taxes each of the parties think Scotland should control compared to what we’re ultimately going to get in the next few years.

And so we come to the bleeding edge of our “journey”. It is a mark of just how profoundly the Establishment was shaken by the 2014 referendum result that all of the tax powers outlined in 2012 are already obsolete before they’ve even been implemented and that the commission set up to “strengthen Scotland’s place in the Union” has failed utterly to do so.

The Smith Commission of 2014 had a nearly insurmountable challenge ahead of it given that it had to satisfy two irreconcilably split philosophies whilst juggling internal party politics, to do it in a way which all but divorced a newly politicised civic Scotland which had led to its creation and to do all this in a timescale of weeks where previous commissions had taken months or even years to do far less. Whilst I’ve spoken before about Smith failing to meet my own expectations and that my response to the Commission was largely less than congratulatory, that it managed to achieve anything at all in the circumstances is actually rather quite surprising.

It was rather less surprised by the scenes of the 9th of November during the debate of the Scotland Bill in the House of Commons. Only six hours were given to debate the entire bill. Two of those hours were lost to Westminster’s archaic voting system which saw hundreds of MPs waiting outside the debating chamber, neither contributing nor listening, until called to stomp in and follow their party whip into which ever lobby had been pre-ordained for them. Another two hours were lost also to those members who did turn up to the debate but wasted time with divergence and slur upon even the very concept of devolution. This left just two hours to debate examine, and consider the acceptability of some 200 amendments to the Bill. I can’t imagine many people who previously supported independence becoming enamoured Unionists based on those displays.

Still. That debate is said and done for now and, assuming the Bill passes both the House of Lords and the Scottish Government without major change, what can we look forward to when it arrives?

Income Tax is once again up in the airs of change. SRIT will be abandoned and the Scottish Government will receive full control over the individual rates of each tax band. This means that, finally, the Government could, for example, raise income tax for the upper rates whilst simultaneously reducing rates for the lower bands.

Rather crucially though, the Scottish Government will still not control the Personal Allowance nor the definition of income nor shall the Scottish income tax apply to interest rates and dividends even if your bank account is based entirely in Scotland (although it must be said that concerns were raised over the state of larger cross border funds like pensions if two rates were applied). It is also not quite clear if the Scottish Government will have the power to create new income bands to smooth out the progression of the tax system or to target extremely high earners or other specific groups. I rather believe that the Scottish Government would not be seriously challenged on that account should it choose to create a new tax band but the power does not appear to be specifically laid out. In any case, the ability to create entirely new taxes is available and could be used as a workaround.

Other devolved taxes involve air passenger duty and a reaffirmation of the commitment to devolve aggregate levies as soon as possible though no date is given for this. Borrowing powers have also been further expanded with the Government soon to be able to borrow for revenue spending (which may help reduce the consistent need for budget underspends in future years) and to retain surpluses in a cash reserve in those years which do “underspend” rather than being forced to roll the funds immediately into the next budget. The Scottish Government will also gain the ability to issue its own bonds instead of having to rely on comparatively expensive commercial rates or to ask Westminster to borrow on our behalf as it has had to do up till now.

Taken as a whole, once again, the Commission has settled on devolving a couple of minor “sweetener” taxes amounting to just 1% or so of the total revenue as well as changing how income tax works. The logic there is quite clear. Income tax is a very “visible” tax as every single worker in the country gets a line in their paycheck every month detailing how much they are paying. Any changes to it, as we saw a decade and a half ago with the “Penny for Scotland” campaign, tends to attract very charged comment often beyond the actual impact of the changes.

Once again though, the Scottish Government shall lose out on any kind of tax power with the ability to actually influence the economy of Scotland. There are still no powers over corporation tax, none on National Insurance, alcohol, tobacco or other health taxes (although the provision is there, in theory, for taxation on other legal substances even if we lack the power to change the legal status of said substances as drugs policy as it remains firmly reserved). Road and energy taxation remains reserved and with Westminster’s recent cuts to the renewable energy sector Scotland is set to become increasingly vulnerable to a Tory ideology which will cost the energy payer a substantial amount of money in the long run whilst doing irreparable damage to our environment and planet.

All in, with this Bill, Scotland’s ability to collect its own taxes shall rise to around 30% of total revenue (again based on GERS 2013-14) whilst its responsibilities over expenditure shall rise to around 65%. I deliberately omit the planned partial re-assignment of half of VAT to the Scottish Government from these figures as they are offset by an equal amount of the Block Grant and the Scottish Government will have no power to actually change or influence rates, definitions or applicability of that tax. VAT is not being devolved, money is simply being moved from one pile to another by an accounting trick.

A comparison of the % of devolved control in Scotland now, under 2012 and under Smith as well as a comparison with Spain and Canada. Source: Scottish Government.

This does lay out the obvious “trap” for Scotland. With ever increasing levels of expenditure being devolved to our “responsibility” but with far fewer means of influencing income raising and with any changes which are made either occurring in minor powers with little actual revenue generation (Even APD will only adjust the Scottish budget by ~0.5% in the best case) or it will fall on the most visible tax of all, the income of every worker in Scotland. This is something which can be ill afforded by Scotland especially when the Government cannot simultaneously raise minimum wage and implement other inequality leveling policies to ensure that people have enough money to live on and contribute to the economy and social after having paid their taxes. The Scottish Government, if it approves this Act, will have to tread very carefully. This will apply no matter which party or parties have the majority when these powers come into force.

Conclusion

Westminster has claimed that the Scotland Bill 2015 shall make Scotland “one of the most powerful devolved governments in the world”. Even with only a cursory reading, this is true only when one considers that no other country devolves power the way the UK does. All this statement means is that Scotland shall have more autonomy than Wales and Northern Ireland but less than Canadian provinces, many Scandanavian regions and local councils and even UK crown dependencies like the Falklands or Gibraltar (which actually do currently enjoy the full Devo-Max that many Scots would have wanted at the outset of the independence campaign).

I suspect that Westminster would quite like this to be the very final round of moving power to Scotland. I suspect that they shall fail in this desire. This is an inevitable consequence of the motivation for all of these changes. That is, to try to head off the day when Scotland becomes independent by throwing some goodies at the Nationalists. The only possible way that devolution could work in this manner would be if it were designed with the motivation of actually working out what powers are best used at a local and Scottish level and placing them there. Subsidiarity, of the kind which the EU prides itself on, may create a family of nations within these islands which actively works for the good of all rather than simply to ‘shut down annoying voices so that our betters can work’. Even if it doesn’t, it would ensure that if and when Scotland does decide to stand on its own we leave the UK from a point of mutual understanding and respect rather than acrimony and divorce. A gradual withdrawal and realisation that Westminster rule did not suit and did not work was the solution that was found for Australia, New Zealand, Canada and many other now independent countries. Scotland should be no different.

Of course, as limited though our tax powers are and as limited though our non-tax powers will be there are still things which can be done. Everyone interested in this country will have their own ideas about what we could turn our country into. Until we’re independent we won’t be able to everything, this is true, but that shouldn’t distract us from the things we can do. And when we want to do something and someone tells us we can’t then we should most certainly challenge them to tell us why not.

Myths and Misconceptions

It’s no great surprise to learn that devolution is an incredibly complex topic. Even just scratching the devolution of just a few tax powers is to omit a vast area of governance. It is no wonder then that a few myths and misconceptions have been floating around in the past few days and weeks. I’ll try to address a couple here.

1) “I’ve heard that if we raise extra money through taxes, Westminster will cut our Block Grant next year so they don’t lose out.”

– No. This is a misconception of “The Principle of No Detriment” within the Smith Commission report. This states that if a power is devolved then neither Scotland nor rUK should lose out just because of that devolution. That is, when income tax is devolved, if both Scotland and Westminster keep the rates the same then income should be the same as if the power was not devolved. Talks are ongoing as to how precisely this will be achieved but will likely take the form of a cash transfer north or south of the border to compensate, for example, for any doubling of accounting.

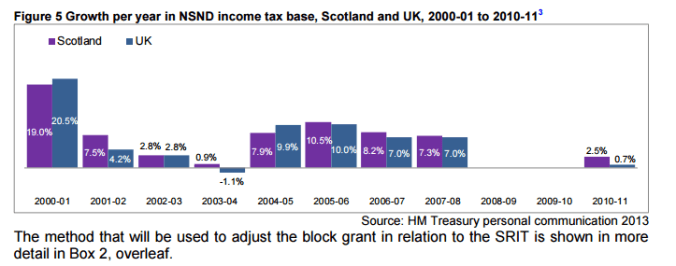

There is the possibility of Scotland losing out due to rUK growing tax receipts comparatively faster than we do as the Barnett Formula would no longer adjust for spending resulting from that but equally this could apply the other way too as it has in most years of the last decade and a half.

Growth in income tax receipts in Scotland and in the UK from 2000-2011. Source: Scottish Parliament.

2) “If Scotland doesn’t spend all of its money this year, is the Block Grant is cut next year?”

– No. The Block Grant is not determined by Scotland’s spending nor by Scotland’s needs but by a flat proportion of public spending in England as per the Barnett Formula. It is not adjusted due to Scottish Government surpluses or deficits.

3) “We’re now free from Austerity. We can just top up any Tory cuts.”

– Partially. This does delve into the welfare side of things where I’ve tried to focus here purely on tax but there are several challenges to this view. Once again, Scotland will only have access to 30% of Scotland’s tax revenue so will have very limited ability to raise money to actually pay for any top ups. If they can be shown to be paid for then this is a power we could use. This should be especially considered in light of consistent reductions in the size of the Block Grant.

However, top ups or additional benefits may be considered by Westminster to be “income” (remember that they control the definition) which would open them to themselves being taxed or, perhaps worse, other means tested benefits would be reduced. The net effect would be no increase in money for the claimant but hundreds of millions of pounds removed from the Scottish Government’s coffers and transferred down south.

Top ups also cannot be applied to those who lose their benefits entirely such as people who are sanctioned for missing their interview at the Job Centre because they were at an actual job interview.

![]()

Discover more from The Common Green

Subscribe to get the latest posts sent to your email.

Pingback: We Need To Talk About: A Negative Income Tax | The Common Green

Pingback: We Need To Talk About: GERS (2015-16 Edition) | The Common Green

Pingback: The Devolution Settlement for Scotland makes as much sense as a Rube Goldberg machine – Max Memos

Pingback: Beyond GERS:- A Response to Comments | The Common Green

Pingback: You’ll Have Had Your Devolution? | The Common Green

Pingback: Scotland’s New Deal | The Common Green

Pingback: Beyond The Headlines | The Common Green

Pingback: The State of This (Union) | The Common Green

Pingback: Grim Drama Parked | The Common Green

Pingback: Four Walls and a Roof | The Common Green

Pingback: Talking Tax | The Common Green

Pingback: The Scottish Budget 2017 | The Common Green

Pingback: The Devolving Union | The Common Green