Understanding is a three-edged sword. Your side, my side, and the truth. — J Michael Straczynski

This week – amidst several weeks of some of the most fraught politics both south and north of the border – saw the re-emergence of a political topic that is both quite defining of my political career so far and has been the source of some of the most vicious and personal attacks levied against me by folk on the other side of my political leanings (albeit, even that was far less abuse than many folk receive on the internet as a matter of course simply for the “crime” of having an opinion in public while not being a straight, white, middle-class, cis-male). But hey, what’s one more time into the breach amongst friends…

(Source: Centre for Ageing Better)

I am, of course, talking about the matter of how state pensions are likely to operate in the transition years immediately after Scottish independence. Sparked by some senior members of the SNP catching up with and seemingly now adopting the position that I introduced six years ago. Namely that:

After Scottish independence and unless there is a political deal to the contrary or a drastic shift in current policy, the State of the remaining United Kingdom (rUK) – assuming it successfully claims Continuing State status with regards to the former UK – shall continue to pay its state pension to people who have paid UK National Insurance in proportion to their years of payment regardless of their citizenship, their geographic location during their period of working or their location upon reaching retirement age and this includes qualifying pensioners living in post-independent Scotland.

It is important however to discuss each of the clauses in that statement and to do so while remaining, as far as possible, above the emotive statements and political bias that have characterised this topic. Perhaps no other – except perhaps the topic of the physical customs infrastructure at the border – is more emblematic of the complexities of disentangling two states and even that exception will ultimately affect far fewer people and in far less tangible ways. Not all of us frequently or regularly cross the border into England. Many more of us face the prospect of growing old and having to prepare for eventual retirement.

Private and Occupational Pensions

This debate is limited the state pension. Many folk will also have private and/or occupational pensions (though estimates are that up to a third of pensioners rely solely on the state pension and several hundred thousand people, as a result of multiple and major policy failures on the part of the UK, don’t even get that).

Private pensions will remain a contract between you and your provider. The state of the UK’s private pension landscape has improved in recent years with the introduction of auto-enrolment into workplace pensions though this hasn’t offset the decline of Defined Benefit pensions or the general risky and fragmented nature of the private pension sector. An independent Scotland should offset any potential risk in differences of currency by offering transfers of pensions into Scottish currency and other improvements to the sector are suggested in the book recently published by I and my co-author Bill Johnston called All of Our Futures. It suggests policies such as creating a publicly-owned occupational pension scheme similar to that found in Sweden which would allow you to take the same pension pot with you throughout your working career – eliminating the problem of having to deal with multiple small pension pots when you retire. Other than this, the private pension system plays little role in the state-to-state negotiations that this debate orbits.

Public sector pensions are slightly different but if anything even more straight forward. Many such pensions are paid to employees in already-devolved sectors such as health and education. It makes complete sense that such pensions will be paid by the Scottish Government or Scottish Local Authorities (most already are). Conversely, there will be pensions paid by the UK Government to, for example, civil servants working on reserved issues in Scotland that will continue to be paid by the UK Government post-independence just as such pensions were paid to former employees of British administrations in Ireland or British colonies after their independence.

In all three pension cases, state, private and public sector, there will be questions about currency. If the Scottish currency appreciates significantly against the British pound then pensions paid in GBP would lose buying power in Scotland and the Scottish Government may have to consider some kind of mitigation mechanism – possibly via a Universal Basic Income or a Minimum Income Guarantee (both of which are currently under investigation as policies already). Of course, Unionist campaigners often claim that the Scottish currency would depreciate against the GBP – something that could have implications in other ways such as folk who choose to continue to pay their mortgage in GBP despite their right (via legislation that will almost certainly be ported from UK to Scots law just as it was from EU to UK law) to have it redenominated to avoid this exact scenario. Indeed, it’s a curious tale in Unionist campaigning sloganeering that the Scottish currency would simultaneously strengthen and weaken and that voters would be affected by the downsides of both but the upsides of neither. Perhaps a future blog post shall look in more detail at this Schrödinger’s currency.

Qualifying Pensioners

To qualify for a UK state pension, you need to pay UK National Insurance. With certain exceptions, to qualify for the full UK state pension you need to pay 35 years worth of NI. Your citizenship is irrelevant (my German wife has as much right to a UK state pension as I do).

With regards to the transition to independence we can essentially think about three different groups of people in Scotland on Day 1 of Independence:

- Folk who have already reached retirement age and have already been claiming UK state pension for days, weeks, years or decades.

- Folk who have not yet retired but have paid some number of years less than their full 35 years and who shall continue to work in an independent Scotland for some period before retiring.

- Folk who have not yet started to pay National Insurance to the UK and who will live, work and retire entirely within an Independent Scotland

For the purposes of this section, I’m going to assume that the policy in both rUK and Scotland will remain more or less the same (even with the same inadequate state pension rates). Group 3 is the easiest to deal with as they would fall entirely under the remit of the Scottish Government’s social security system. Group 1 is perhaps best thought of as equivalent to the 1.2 million people currently receiving their share of the £4.2 billion paid out each year in UK state pensions to people already living outwith the UK. Group 2 lies within a blend of the other two. Imagine, for instance, you had worked in the UK for 20 years and then in an independent Scotland for 15 years. Assuming current policies don’t change, you could then expect to receive 20/35ths of a UK state pension and 15/35ths of a Scottish state pension. In that regard, Group 2 are equivalent to folk who have lived and worked in two or more countries for part of their lives.

Sharp eyed readers will have already noted that the total non-UK pension figures above only distilled down to an average of around £3,600 per pensioner, per year. Some of that is due to folk falling into Group 2 – working in the UK for part of their working life but moving elsewhere for a period before retiring, but some is also due to a combination of the UK state pension being one of the lowest in the developed world and recent reductions affecting “ex-pat” pensioners. More on how that could affect Scotland below.

The Cost of No Deal

According to GERS, some £8.5 billion was paid in state pension “for” Scotland in 2020-21. Most of this will involve pensions paid to people in Scotland although GERS also notes that it includes a population share allocated to Scotland’s accounts of the amount paid to “ex-pat” pensioners. That probably amounts to about £350 million. Any “deal” may include the Scottish Government taking on responsibility for some of these pensioners but as we’ll see below, that could be a complex problem.

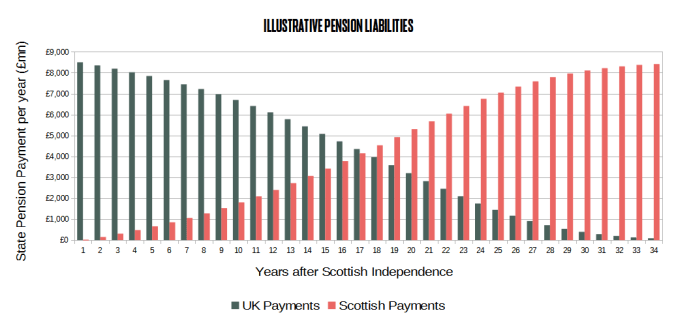

So if there is No Deal on pensions, then the UK would be liable to close to that full sum but this wouldn’t be the case indefinitely. As the years wind on, fewer Group 1 people will live in Scotland having worked their full lives in the UK. More will fall into Group 2, having their pension split between Scotland and rUK and then, eventually, we shall start to see Scottish pensions paid to Group 3 people. Eventually, all of Group 1 and 2 will live out their lives (which could take many decades especially in Group 2’s case as the latter may include an 18 year old who pays one year of UK NI before independence but who then goes on to live till age 118), the transition will complete and Scotland would be solely responsible for pension liabilities with the exception of new immigrants to Scotland or folk who leave Scotland to work elsewhere (perhaps within rUK) then return.

So the UK’s liability under a No Deal will peak (possibly at the point of independence or possibly slightly after given shifts in demographics and the fact that people can pay their 35 years NI but still have some years of work ahead of them) and then decline. You’d have to break out the Actuarial Tables to work out the precise rate of decline and combine that with policy changes affecting things like pension age, changes to NI contributions (what if the UK decides you need to work 40 years to claim full state pension?) and the rate of pension itself but it could end up looking something like the graph below.

(For the avoidance of doubt, don’t take the numbers too literally)

As many have noted, independence won’t be a single event but a transition. This is rarely more apparent than in pension politics where the decisions of a certain Minister on a certain day can have implications far into the future, long after the Minister is out of office and no longer in charge of that policy or even long after they themselves are no longer alive and cannot be held accountable for their decisions.

Continuing the State

There are essentially two main ways that a state can break up into two or more states. The first is a “dissolution”. In 1993, Czechoslovakia dissolved and ceased to exist. In its place, two new states were formed – The Czech Republic (Czechia) and the Slovak Republic (Slovakia). Both of these states are considered “new”, with no legal continuity with the previous one.

The second is a “secession” where one or more parts of the state become independent but a rump or core of the previous state remains and claims “Continuing State” status – essentially, retaining the identity, history and obligations of the previous state as its own – just with a reduced territory. Often, the “Continuing State” is the largest part of the new political formation but raw political power is also important – if only area or population defined such a thing, the capital city of the United Kingdom would currently be New Delhi following the creation of the Republic of India in 1950.

A more direct example is found, again, in the UK in 1922 with the ending of the United Kingdom of Great Britain and Ireland and the creation of the United Kingdom of Great Britain and Northern Ireland. The latter subsumed the former’s identity so thoroughly that many in Britain fail to see the distinction at all. Another would be the successful claim of the Russian Federation as Continuing State to the Union of Soviet Socialist Republics. This last example is of particular note for the UK as Russia used its Continuing State status to claim the USSR’s Permanent Seat on the UN’s Security Council. This is a seat that the UK would also dearly like to hold on to. Losing Continuing State status would add severe complications to the negotiations over other debts and liabilities and would also mean tearing up all of its trade deals (including the recent Brexit deal – though some hard-line Conservatives might see that as a bonus at this point) and might force rUK to dissolve its nuclear weapons arsenal as it would no longer have an opt-out on maintaining such weapons under the Non-Proliferation Treaty. The UK could theoretically push for this dissolution as a nuclear (sic) option to avoid paying pensioners outwith its territory, but I’d estimate that the price of doing so would be a lot higher than the price of those pensions. For my part, I believe that Scotland should go into post-indy negotiations with a firm statement that we shall support and recognise rUK’s Continuing State claim on the provision that they treat the negotiations in good faith and with a commitment to protect the wellbeing of people affected by the democratic decisions – in other words, so long as they do not hold vulnerable pensioners hostage for political gain.

The Empty Pot

One of the objections often heard against the claim of some kind of enduring “right” to a state pension is the lack of a “pension pot”. Your state pension isn’t paid out of a pot of invested income grown from your National Insurance payments the way that your occupational pension is paid out of savings and investment income built up by your contributions to it. This isn’t quite true. There is a UK National Insurance Fund that was set up in the wake of the Beveridge Report and it was designed to fulfil this purpose but it has not kept up with growing population and extended lifespans. In practice, NI contributions do not match its obligations and outgoings and so it is topped up by the Treasury’s Consolidated Fund. For all practical purposes it makes no difference and the UK state pension operates as it would if such a pot didn’t exist.

Hidden within this line of argument however is another one that says that “workers pay for pensions”. This is a topic that we address All of Our Futures. It is an attitude that comes, fundamentally, from neoliberal economics which defines “workers” as “productive consumers” and “pensioners” as “unproductive consumers”. Your utility as a person is defined only as your ability to consumer goods and services. It inevitably boils pensions down to an argument of its “affordability” in the face of the ratio between workers and pensioners – something that is divisive, ageist and poisons politics outwith pensions such as discussions about immigration by defining migrants’ as only having utility only so far as they can “pay for” and “care for” older, native folk.

The same divisive and ageist politics is seen when folk – even on the Left of the Unionist campaign – ask “why should British workers pay for pensions in Scotland?”. If there is no “pension pot” then, by definition, workers don’t pay for state pensions – neither others’ nor their own futures selves’. Instead we should look at the full gamut of tax and spending (or spending and tax if you prefer the MMT lens) and consider where the priorities of the nation and its social security should lie. I’d suggest by not starting with cutting taxes on banking profits.

Changing Policy

A less drastic way that the UK could weasel out of paying state pensions to folk in Scotland is one flagged up by the Fraser of Allander Institute yesterday and is a line I’m familiar with having had it boldly asserted to me multiple times over the past six years. Given that UK doesn’t have a Constitutional protection wrapped around the state pension then its very existence is a mere matter of policy. It could be increased, reduced (see the link above on the recent reductions for some “ex-pat” pensions) or even eliminated altogether.

This is true but the UK would have to tread very carefully if it wanted to walk this particular ground. As the opening statement says, the pension is paid without regard to geographic location or citizenship. Yes, there are exceptions around things like an inflation-indexed uplift to that pension but broadly speaking, if you live outwith the UK you will get some form of UK state pension according to your previous contributions.

If the rUK actually carried through the threat as Unionist campaigners would have you believe and they simply refused to pay a pension to qualifying pensioners in Scotland and only in Scotland then they will almost certainly open themselves up to the mother of all discrimination cases. I would not be surprised if the inevitable court case ruled that discriminating against pensioners living in a single country would be unlawful. Despite the lack of a citizenship basis to the pension, wouldn’t it be better for the rUK to signal to British nationals living in Scotland – as elsewhere – that the UK still maintains some sense of respect for them, their identity and their past contributions to the country they no longer call home?

This goes too if the rUK decided to refuse state pensions to Scottish citizens. Again, your pension is not currently based on your citizenship. I doubt this would even have much of the desired effect anyway. It is overwhelmingly likely that current UK citizens living in Scotland on I-Day who qualify for Scottish citizenship will be allowed to become dual citizens. A few Scottish nationalists may well renounce their British citizenship to become solely Scottish but I expect that only a few will (if nothing else, the process is complex and quite expensive). A few British nationalists may well refuse their right to Scottish citizenship and remain solely British despite remaining in Scotland (for my part, the transition process and Scottish Constitution should make that process as easy as possible – an independent Scotland must accommodate those who disagreed with independence even after it becomes a reality and accept them in our new country). But most will simply become dual-nationals (I probably will). There will also be a substantial population of folk resident in Scotland who hold neither citizenship. To bring up my wife’s example again, with only a few exceptions Germany does not generally allow multiple citizenships with non-EU countries so she cannot claim UK citizenship without renouncing her German – and therefore her EU – citizenship and could not accept Scottish citizenship either until Scotland re-enters the EU without the same renunciation. But, as said, she has paid her NI (and has worked in both Scotland and England) and thus is due a state pension. The rUK therefore couldn’t easily discriminate against solely Scottish citizens without “catching” UK citizens in that net or missing many folk who are neither.

The rUK might decide to try to split the liabilities not based on where someone lives at the point of independence (which could lead to an interesting case of someone living in Scotland their entire life except for that one day they lived in Carlisle which just happened to be I-Day…) but on where they were based when they paid each qualifying year of National Insurance. This would be a massive data challenge, especially since the UK doesn’t maintain a national identify system similar to most countries in Europe where you register with your local municipality. We’ve already seen the huge problems caused by analogous policies such as the EU Settled Status scheme. The rUK simply may not have the data it needs to accurately make the assessment of whether or not your pensions should be paid by the rUK, Scotland or split between them. Again, I foresee massive legal challenges when (not if) they get things wrong. A proxy might be possible in the form of the Scottish Income Tax but it simply hasn’t been running long enough to track everyone and there have been high profile instances of this system going wrong too.

The rUK could, however, simply cancel the state pension to everyone outwith rUK including all of the “ex-pat” pensioners mentioned above. That kind of blanket policy might be on safer legal ground when it comes to discrimination but especially given that there are more people receiving UK state pension outwith the UK than there are within Scotland and many of them have but don’t currently exercise their right to vote…I think it would be a bold politician who’d consider this as a “solution”.

But could the rUK take a step even further than this? Short of the nuclear option of dissolving itself as a legal entity, it could simply dissolve the UK state pension and stop paying it to anyone. Again, it might not face a discrimination case if it did this (though the pain of such a policy would likely fall disproportionately on people suffering other forms of systemic discrimination in the UK) but I can’t see how the people of Britain would consider this to be an upside of what would be a monstrously inhumane act inflicted on tens of millions of people simply to spite voters in Scotland for being insufficiently loyal to the British State. If the Unionist campaign really does want to take up this line of campaigning as an “enticement” to vote No then affected voters should probably ask themselves why they should vote in favour of a government willing to act so barbarously towards them even if they do but find themselves in the minority.

So no, whilst it is technically possible for the UK to dispense of its obligations under current policies I can’t see how it could do so without either opening itself to massive legal challenge or doing far more harm to itself than it’s worth to mitigate the “problem”.

Why Settle a Deal?

A liability transfer deal of the kind that the Scottish Government put forward in the 2014 Scotland’s Future White Paper is there for the making (though keeping in mind that the UK Government rejected that paper so can’t be too sanctimonious about us exploring alternative approaches…). It’s easy to see why the UK would want to settle such a deal as it would immediately take several £billion in liabilities off their books at a time when the neoliberal economics they espouse warns of an approaching “demographic timebomb“. It would also avoid the discrimination problems detailed above and go some way towards repairing the reputation that the rUK is a country that can deal in good faith with others.

There would be advantages for Scotland to accept a deal too. For one, it would eliminate the currency exchange risks mentioned above. It would allow all pensioners in Scotland to benefit from a higher rate of state pension should Scotland choose to do so (or, at least, avoid Scotland having to mitigate against the UK’s penurious pension policies) and it would increase the democratic accountability of pensioners in Scotland as they could petition the Scottish Government as voters and constituents whereas their ability to influence UK policies is likely to sharply reduce. For both governments, a deal would remove a link between the two independent states that could potentially become a diplomatic liability (or weapon) in the future.

I would suggest that when the Scottish negotiation team approaches this issue they should lay all of these issues in front of everyone. The UK’s ability to simply walk away from a potential deal is far, far less than they would have us believe – the consequences for them could be dire. Whereas for Scotland it is much more a matter of ensuring that those the UK walks away from are adequately provided for.

However, if the Scottish Government does take on the liability for paying the state pension of residents in Scotland (again, regardless of whether they are Scottish citizens, British citizens, both or neither) then it shouldn’t be considered unfair to negotiate some kind of Equivalent payment from the UK to do so. This could be a lump sum or a time limited series of payments. It may even be a deal where the Scottish Government administers the state pensions in Scottish currency but then “bills” the UK Government for the appropriate amount in Sterling. It’ll be up to smarter heads than mine to come up with an appropriate amount for this but if we took the illustrative graph above more literally than we should then it suggests that 35 years of UK liabilities would sum to approximately £140 billion. Such a sum is curiously close to the amount suggested in the “worst case” negotiation over Scotland’s “share” of UK National debt.

Perhaps; taking the two together; Scotland and the rUK could just call it even.

Conclusion

You’d think that such an important topic would generate far less heat and far more light than it does. My experience indicates that this has so far not been the case. Perhaps because it is so complex and far reaching, some find it easier to deploy fear, uncertainty and doubt in order to intimidate voters into a preferred position. I find that kind of politics utterly reprehensible and would hope that it’s ultimately self-defeating. As said above, if the only way you can convince me to vote for you is to tell me that you’ll punish me if I don’t, then you don’t deserve my vote.

This kind of politics is made even more ugly by the fact that the only reason that people can be made to feel insecure about their pensions is because the UK state pension system is inadequate at providing proper social security and, indeed, as the UN has noted it is designed not to. When people are already insecure, it’s easier to threaten them with the loss of what little they have and it’s well known that humans are hard-wired to be risk-averse in such situations.

In the absence of more rational politics from the other side, the challenge for Scottish independence advocates will be to reframe our own arguments to counter the fear induced by the other side.

We shouldn’t have to. My appeal to the other side is to get out of the gutter, to appreciate the complexity of pension politics over cheap slogans and to start dealing with voters in the respectful, inclusive and non-discriminatory manner you would expect if our respective roles were reversed. It could start with a mutual agreement of no detriment – a promise by both sides of the campaign that no matter how pension deals shake out or who ends up paying for what, no pensioner in Scotland will get cut off without their state pension. If the leaders of the pro-Union campaign can agree to that, then perhaps it will make it easier to discuss everything else.

![]()

Discover more from The Common Green

Subscribe to get the latest posts sent to your email.

In the event of independence, Scotland would take on its share of UK assets and liabilities.

One of those liabilities is the responsibility of the UK government ( England, Wales, Scotland, and Northern Ireland) to pay future pensions to all UK citizens.

Another of the liabiliities is Scotland’s share of the national debt.

In your article, you suggest that both of these figures are roughly £140 billion. I don’t know whether that’s accurate or not. But assuming it is – that means Scotland’s share of these two liabilities is the SUM of these two figures. And yet you suggest they should be balanced off against each other and “call it even”.

If I borrow £50 off you today, then another £50 off you tomorrow – can we call it even ?

LikeLike

rUK paying the state pensions of former UK NI payers living in Scotland would represent a flow of money towards Scotland. Scotland paying a “share” of the former UK’s debt to the rUK (which would be the easiest way of doing it as taking on the debt itself would require the agreement of the holders of the bonds, See: https://commonweal.scot/policies/claiming-scotlands-assets-a-discussion-paper-on-the-division-of-assets-and-debts-to-an-independent-scotland/) would represent a flow of money from Scotland to rUK. If the two amounts were roughly equal, then they’d effectively cancel.

LikeLike

Continuing State status is irrelevant – it only affects International Agreements. UK has no International Agreements with Scotland as Scotland is part of the UK. And there are no International Agreements covering UK domestic pensions. There are treaties with a number of countries that the UK would presumably continue.

https://www.gov.uk/government/publications/state-pensions-annual-increases-if-you-live-abroad/countries-where-we-pay-an-annual-increase-in-the-state-pension#eea-countries-and-switzerland

“As the opening statement says, the pension is paid without regard to geographic location or citizenship. ”

Then the opening statement is wrong.

https://www.gov.uk/new-state-pension/print

“You can claim the new State Pension overseas in most countries”

It should be obvious that the very essence of Independence splits the Nation in National Insurance and the State in State Pension. The sysyem would be split, whether Scotland agreed or not. The Scottish state would be responsible for paying it’s own SP from its own NI, on the same pay-as-we-go basis as the UK does. That is the obligation that Scots pensioners would expect to be honoured.

The idea that Scotland would renege on pensions to it’s own people is frankly disgusting.

LikeLike

Pingback: Parting Ways | The Common Green