One should have three major principles. Talk, boldness and strategy. – Fujibayashi Yasutake

Today sees the launch of my latest paper for Common Weal, Claiming Scotland’s Assets, in which we discuss the consequences of independence with regard to debt and asset negotiations.

Actually it seems like only March that the last edition was out. What’s happening here?

Well, there was a consultation that almost no-one knew about which discussed a few methodological changes to GERS in line with the ‘new powers’ we’re getting and it also asked if the next report should be brought forward. I’m completely convinced that the fact that this means that we’re getting the report well before the Council election campaign next year is absolutely just a convenient side effect(!)…but no matter. We’ve got the data.

Tomorrow’s Headline Today

Scotland’s budget deficit remains at a little under £15 billion. As with last year, don’t expect a single news outlet to go one single step further with the story than that. Except maybe to say that oil revenue has dropped from £1.802 billion last year to just £60 million this year.

So what’s happened? Why hasn’t Scotland, which is “totally dependent on oil”, completely collapsed now that oil revenues have basically dropped to zero?

Last year, total revenues dropped by around £500 million on 2013-14. This year, total revenues have INCREASED by £181 million. In fact, total revenue is higher than it was in 2012-13 when we received some £5.3 billion in oil revenue.

It’s also worth noting that if you only look at GERS 2015-16 then it looks like our deficit has increased by a couple of hundred million in the past year but if you look a bit deeper, and compare the numbers to previous GERS reports then something interesting happens.

In GERS 2014-15 our deficit was recorded as £14.8 billion but in GERS 2015-16 the 2014-15 deficit has somehow dropped by £622 million to £14.3 billion. Essentially, this shows one of the limits of GERS in that it is based on sometimes highly speculative estimates which get revised over time. It may be five years before we finally know the “true” accounts figures for this year. This accounting adjustment is extremely significant compared to, say, our “budget underspends” but unless you’ve read it here I expect it to pass entirely unnoticed.

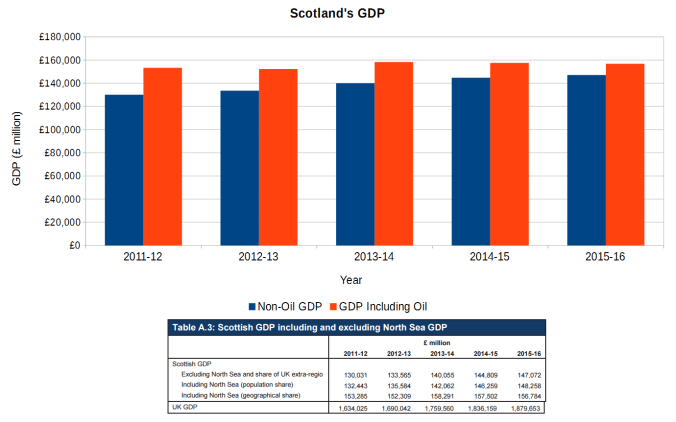

Now, what about our all hallowed GDP? It’s down by 0.45% from £157.502 billion in 2014-15 to £156.784 billion in 2015-16 (with non-oil GDP having increased by over £2.2 billion, the highest it’s ever been).

You know, perhaps it’s time we started measuring our economy in terms other than just GDP. We know it’s flawed. We know it throws up extremely strange results like Ireland’s “economy” growing by 25% because a few American companies moved their nameplates around. We know it doesn’t even particularly correlate to things like tax and ability to service debt very well.

Maybe it’s time we started measuring (and taxing) our country based on the things which actually matter.

But back to GERS.

Dutch Disease with Scottish Characteristics

So what’s going on here? Essentially it’s the same pattern first picked up last year. As oil prices drop, so do fuel costs. Which means everything from the costs of transporting goods to the heating and lighting costs for your home drops. This means you have more money to spend in the economy and companies have fewer overheads leading to either greater profits (thus, ideally, more tax revenue) or more room to invest in expansion.

This is a clear demonstration of the so-called “Dutch Disease” where high oil prices choke off the non-oil based economy in the form of the aforementioned fuel costs (it also tends to harden one’s currency but this is less of a factor in the Scottish case given that we don’t yet have one).

At the time of the last report I was criticised for pointing this out on the grounds that the oil price collapse “hadn’t fully fed through” hence I was jumping the gun on the observation. It shall be interesting to see if anyone says the same thing now. Could revenues drop any lower?

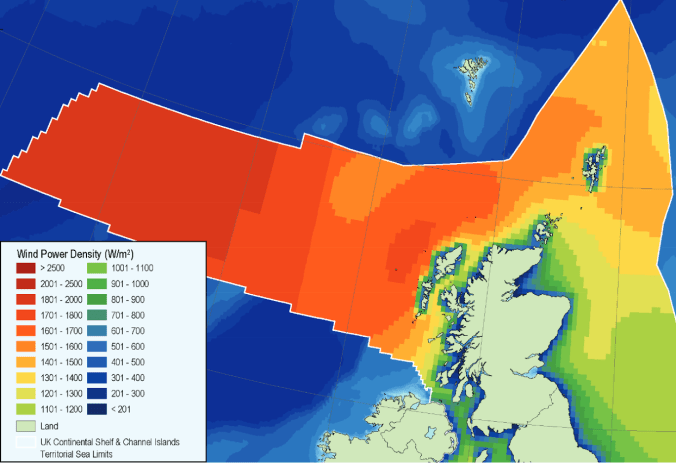

This should serve as somewhat of a warning to those itching for the return of high oil prices and certainly for those desperate to “replace” offshore oil with onshore fracking. It’s maybe time to have a good hard rethink about what kind of resources we want to develop in Scotland. Now, to be sure, I’ve nothing against our offshore industry and for those folk out there it’s been a pretty dreadful time. It’s just that, certainly as a Green, I think our offshore industry is on the wrong side of the country and should be based on wind/wave and tide rather than oil. You can be sure that if the wind and tide stops flowing we’ll be dealing with problems a little bit larger than the state of our finances.

Scotland’s offshore Wind Power Density map

Sweet Fiscal Autonomy

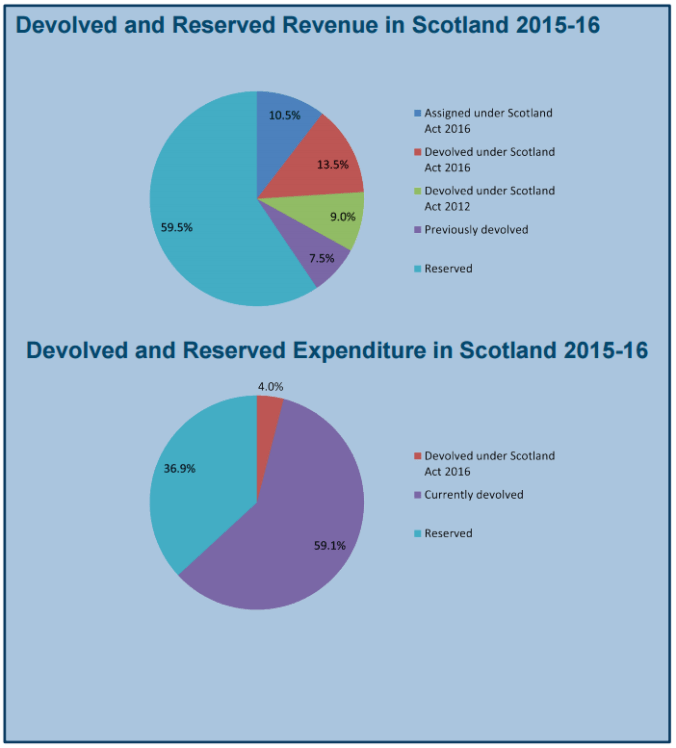

As mentioned earlier, part of the methodological changes discussed in the GERS consultation was to do with looking at the taxes to be devolved to Scotland under the series of “vast, new powers” we’ve been generously granted.

In terms of actual revenue, chief amongst these is income tax (excluding interest and dividends, the ability to move the Personal Allowance or to adjust the definition of “income”) and VAT (excluding any actual control at all. We’re getting the VAT added to Scottish coffers and then an equivalent amount removed from the block grant. Yay.) along with comparatively minor taxes like landfill tax, aggregate levy and air passenger duty.

In total, the Scottish government will directly receive 40.5% of Scottish revenue (£21.8 billion this year) and, given the limitations on VAT and income tax, have actual, practical control over perhaps half of that. Devolved expenditure, however, will soon sit at 63.1% of total (£43.3 billion). Basically the Scottish government can only directly control enough income to fund perhaps about a quarter of what it’s directly responsible for delivering.

There’s a side issue in all of this related to that old topic of the budget underspends. Tucked away on page 47 of GERS there’s an interesting line which looks at the confidence intervals for some of the tax revenues used. Remember that the revenues given are estimates and are subject both to revision over time and change due to circumstances that the government cannot control. For example, if you move job half way through the tax year your income, therefore income tax, can change. If your job moves you to England, your entire income tax contribution moves from the Scotland side of the budget to the rUK one. Hence, the total income tax revenue estimate is subject to a margin of error, in this case of 1.0%.

The same goes for other taxes to greater or lesser degree to the effect that the margin of error over all of the taxes measured there is 1.6% or ±£570 million.

Remember that the Scottish Government has extremely limited borrowing powers. It can only “overspend” on the current budget by £200 million in a single year and cannot exceed a total current debt of £500 million. And yet income revenue, on which expenditure must be planned, has a margin of error of ±£570 million.

In the event, this year Scotland’s “underspend” was only £150 million. If you think you can plan a budget better than this then please, send it in. If not, might be a good idea to stop reporting and moaning about underspends.

Paying For It

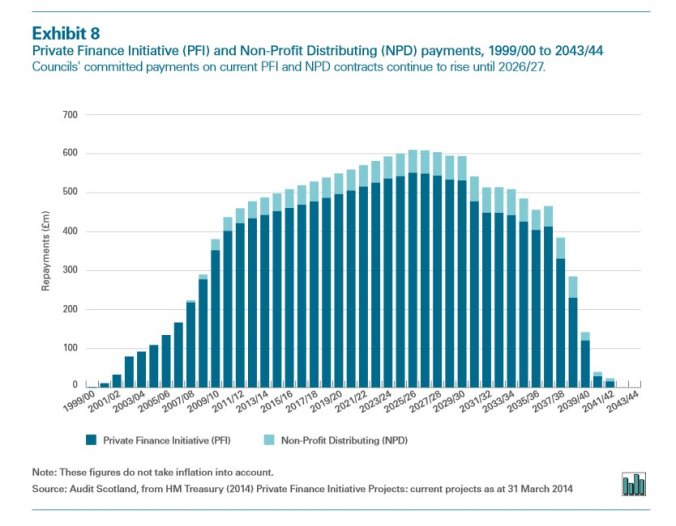

Another little line that seems to have been added to GERS this year (on page 37) is a breakdown of the annual costs of financing Labour’s PFI and the SNP’s replacement NPD loans. There’s been a bit of a milestone reached there with the availability costs of PFI now exceeding £1 billion per year or over 15% of Scotland’s total capital budget and slated to increase even further over the next decade unless something is done about it. Don’t be surprised if this becomes a major issue for the council elections next year.

Of course and once again you wouldn’t know this if all you did was watch our Great British Broadcaster, the BBC. Their recent “investigation” into PFI couldn’t even bring itself to mention the name of the party which lumped this crippling financial burden on us.

Finally

I could go on. We could nip-pick at details like the mysterious addition to the expenditure budget of net EU contributions (there’s always been an annex discussing this but this is first year it has explicitly been counted in a separate line in Total Expenditure) or notice that for the first time in at least five years our debt interest paid has increased as our UK debt increases have started to outweigh the effect of falling bond yields.

It’s all a shell game though. We know that GERS isn’t nearly as important as people hold it to be nor is it nearly as informative as it should be. It’s not going to change many minds on its own nor does it tell us one single thing about the finances of an independent Scotland. If we want to do that, we’re going to need to build a national budget from scratch, taking into account all of the taxes (existing and new) that an independent Scotland might choose to levy. We also need to have a look again at what Scotland actually needs to spend its money on. Could we use Citizen’s Income to create from scratch a welfare system worthy of the name? Would a Scottish Government able to issue its own bonds on its own debt be able to get a better deal than the one we have right now?

Quite simply can Scotland as a nation see ourselves as better than others would prefer us to be seen?

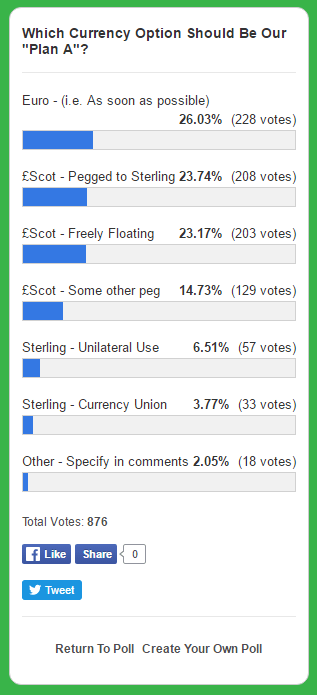

I’d like to run a straw poll to help inform some thoughts I’m having on currency.

So imagine you are in charge of the newly reformed indyref2 campaign. You’ve been asked to direct the currency question strategy. What’s your preferred “Plan A” going into the campaign?

Poll now closed – Results below. Thank you for voting.

Feel more than free to expand on your thoughts in the comments below.

(If it’s your first time commenting on this blog you may end up in a moderation queue. I’ll approve as quickly as I can)

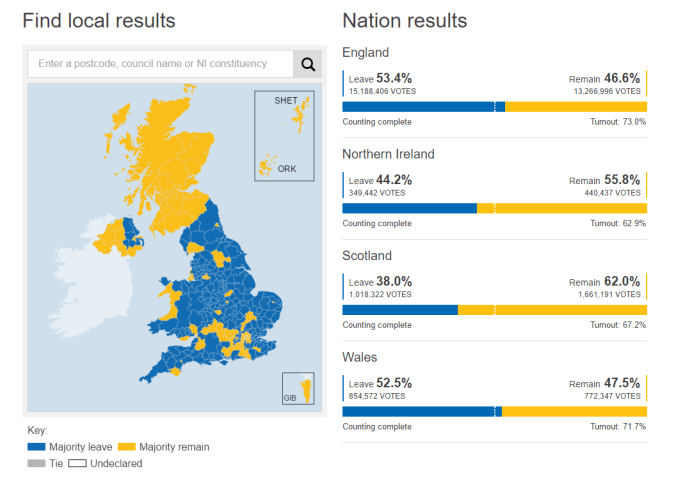

Well that’s that then. Votes cast and counted and the UK, by a margin of 51.9% to 48.1% have voted to Leave the European Union. The long, fractious and never really embracing journey that the UK has been on shall now enter a new phase. I can only guess as to where it’ll end up.

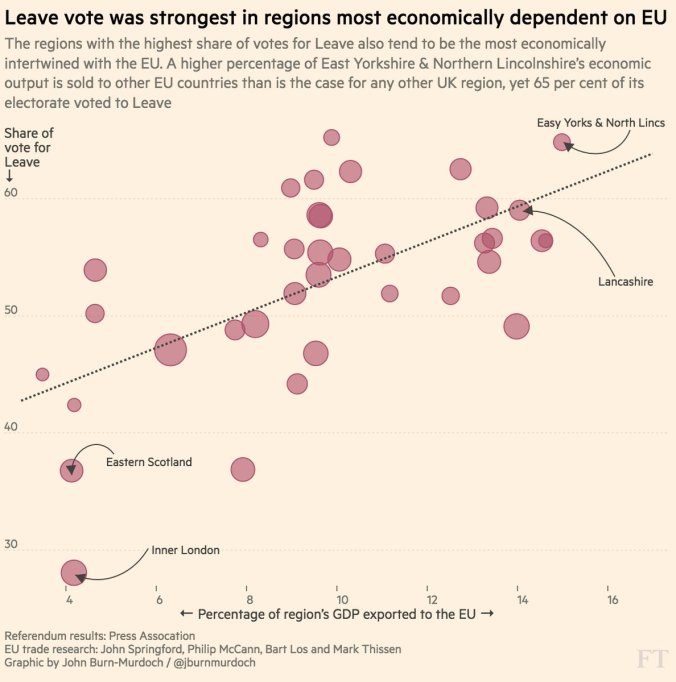

You may have heard by now though that the vote across the nations and regions of our “One Nation” was not homogeneous.

England and Wales voted to Leave. Scotland and Northern Ireland voted to Remain. It represents yet another rejection by Scotland of “UK” politics and I believe that, as previously stated, a second independence referendum is now inevitable. The First Minister has herself confirmed this morning that the Scottish Government is now going to actively pursue one whilst also seeking to negotiate directly with the EU to try to preserve and protect our relationship. I do not believe that we will find that door to be particularly tightly closed.

As for Leave, once they’ve dealt with the resignation of David Cameron, probably a few key allies too, and have taken over the Tory party they’ll have to get into the grit of actually disengaging with the EU.

The EU Commission has already made it clear, understandably, that they would prefer Article 50 to be triggered as soon as possible so that they can get the whole business done and dusted. Leave, however, are still trying to be cagey. Some of the talking heads in the media today are still even hinting at an “alternative” plan like a Vienna Convention type disengagement. The big problem with that idea is that, even if it’s possible, it can be vetoed by any of the remaining 27 states. If the EU insists that Article 50 and a formal discussion is the way to go then it can indeed insist that it shall be.

It’s still very far from certain what the UK’s future relationship with Europe will actually be once all is done and dusted.

Indeed, there’s an outside chance that a Brexit may not yet happen. It could be that the Tory leadership changeover results in a General Election…which the Tories then lose. Labour, especially one which actively campaigned on the point, could well ignore the referendum result. At this point I wouldn’t discount any possibility, no matter how unlikely.

Assuming though that Boris Johnson and chums take the reigns and we go through Article 50 and Brexit happens, there’s still several possibilities (ranging from EFTA, through a set of Swiss style biateral treaties, through a CETA/TTIP type deal and out to the “default” WTO regulations only) which I outlined here.

I’m particularly disturbed by some of the rhetoric which stuck. Lord Ashcroft’s on-the-day polling found a solid correlation between likelihood of voting Leave and support for the argument that it would help “Take Back Control”.

I mentioned in my article on sovereignty that countries which pin themselves to the idea of national level politics, especially to the point of it becoming a geas, can bind themselves into the Globalisation Trilemma. If, as I suspect they will, Leave use their win to forge towards turning the UK into some kind of Free Market paradise then the concept of democratic politics could find itself severely compromised.

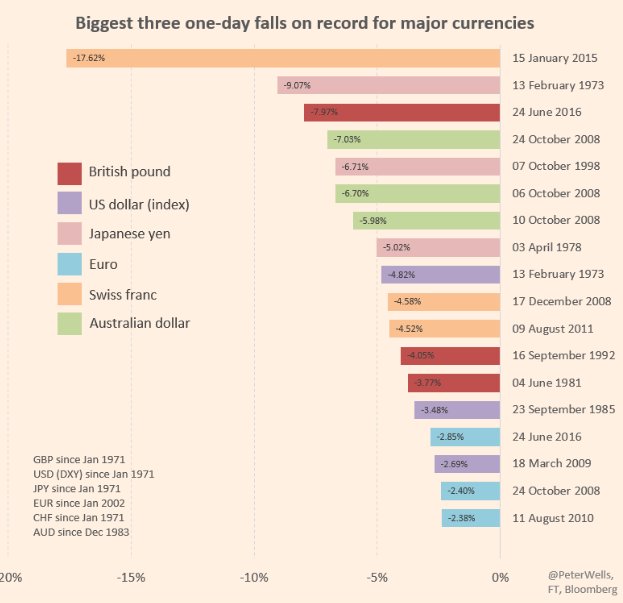

Speaking of the Free Market, it was in the financial world that the most “excitement” of election night was to be found. The polls, public and private, in the days running up to voting day had starting indicating a Remain vote. This had pushed the value of the GBP up significantly as traders started “buying the rumour“. When the Sunderland vote came in though it was the first indication that things were not going to go well for Remain. That one result caused a panic sell in the markets which did not improve as the night went on. By morning, the “Great” British pound had fallen to the weakest point seen since 1985 and, after a morning-after retracement, had lost 8% of its value. This is the worst single day hit that the pound has ever taken, twice as deep as plunge as 1992’s “Black Wednesday” and the third deepest single day hit ANY major currency has taken in modern times. History books shall be written on this point alone.

It should be of very careful note that against the Euro, the Pound lost about 10% of its value compared to 2015. This is important because the UK had a trade deficit with the EU of about £68 billion in 2015. Assuming all things other than currency being equal then that trade deficit could be expected to rise to £75 billion simply because it’s now more expensive to import goods and services from Europe.

This difference in trade, around £7 billion, represents almost exactly the amount that Leave claimed that we’d “save” in net contributions to the EU. There may well be no gains, no money for the NHS or anything else that was promised. I hope I’m wrong. Because if I’m not, the areas which most voted Leave are also the areas most likely to be dependent on the EU for trade. They will be the areas most reliant on a good deal and/or economic plan for what comes after.

As for Scotland, it’s looking now almost inevitable that this result will hasten another go at an independence referendum and, this time, not only will it not be called until we’re ready but it’s looking rather like a lot of former No voters who had been promised that their vote would ensure their EU membership have now seen that whisked away. It has been enough to convince many that independence is now the best option ahead of Scotland. If you happen to be one of them, Welcome.

The Greens and the SNP, will now be exploring all options to protect and preserve our EU relationship. We’re in very uncertain times now with few precedents to guide us so what form this will all take is a matter of pure speculation.

My own preferred option could take the form of direct negotiations between the Scottish Government and the EU resulting in some kind of deal whereby if an independence referendum is held and won in the period before formal Brexit then a newly independent Scotland could “inherit” the UK’s old seat with no loss of continuity. Of course, this would require the co-operation of the Westminster government to allow such negotiations to take place or to even acknowledge that the result in Scotland is significant. It would be a tragedy of democracy if we were simply ignored.

I’ve got no easy answers for the next few months, or years. I’m as much an unwilling passenger as everyone else who voted Remain yesterday. I’ll try my best to work out where we’re going just as soon as it becomes apparent though. And who knows. Maybe, just maybe, we’ll get off early.

“It can be concluded that both shale oil and shale gas are unlikely to be economically viable in this current low hydrocarbon price environment and even if there is a return to recent higher prices; it is likely that the industry would require significant subsidy or significant efficiency progression before it could be used at any kind of scale.”

“Even if the extraction can be proven to be environmentally ‘safe’ the experience of the United States shows that it risks bringing boom-and-bust to our communities as waves of temporary jobs move rapidly through without rooting themselves in local economies.”

My first paper written for the Common Weal has been published today. The Economics of Shale Gas Extraction is the first major paper to be published in Scotland focusing on the economic, rather than environmental, impacts of the industry particularly on the local communities which will be hosting the wells.

Key Findings:-

The SGE market in the US and, so far, in the UK is dominated by larger companies occupying the most profitable licences. There is little scope for community owned or small company development to occupy a significant market share.

Individual wells become largely non-productive within a few years of development which, due to market demand for constant production, forces companies to continue drilling new wells in new locations at a rapid pace.

The low recoverable volumes and high capital and running costs of wells may render profit margins comparatively small and extremely sensitive to oil and gas pricing. There appears to be little scope for economic development of SGE in the UK until and unless wholesale prices return to historic highs and even then significant subsidy may be required.

Communities are likely to be significantly adversely impacted by nearby SGE fields. The concentrated pattern of land ownership and comparatively weak situation of local government renders communities vulnerable to being unable to capture wealth generated by nearby wells whereas the burden of environmental degradation or even simply the threat of such degradation can lead to community stress and negative economic effects.

The jobs created by SGE appear to be short-lived and highly mobile. The job demographic of the planning, drilling and production phases are each relatively exclusive meaning that they will move to the next site more rapidly than the wells themselves do. This creates the risk of a “Boom-Bust” effect in communities.

Shale oil and gas is considered a relatively poor source of fuel due to high extraction costs. The UK’s reserves are also likely to have an insignificant impact on global markets and hence a negligible impact on end-user prices.

Significant externalities have been identified in the form of environmental degradation due to methane leaks. The costs to mitigate these may exceed the lifetime revenues generated by the well which produced them. Further, the UK has a poor record in terms of ensuring adequate decommissioning and restoration bonds which may lead to further public funding being required after the SGE companies have left an area.

Whilst much of the attention on the shale oil/gas and fracking industry has been focused on the environmental impact, less attention has been paid to the economic effects. Even if the extraction can be proven to be environmentally “safe” the experience of the United States shows that it risks bringing boom-and-bust to our communities as waves of temporary jobs move rapidly through without rooting themselves in local economies. Scotland’s history of concentrated land ownership and comparatively poor local government also risks creating a vast transfer of wealth benefiting the already wealthy whilst potentially leaving communities to foot the bill for cleaning up. All for a fuel which the government has been told will not even benefit us in the form of lower energy bills.

There should be no place for fracking in Scotland or the UK.

“I would say is that every public-private partnership in Scotland has delivered new hospitals or new schools in Scotland on time and within budget and that’s the sort of success I want to see in every building.” – Jack McConnell, 2002

Oxgangs Primary School, 2016. Built by PFI in 2005

The dramatic news from Edinburgh in the past couple of weeks has put into sharp focus the failures of some of the finance models used by our regional councils to build schools, hospitals and other public buildings in recent years. Public/Private Partnerships (PPP), Private Finance Initiatives (PFI) and, less well known, Lender Option, Buyer Option (LOBO) Loans have burdened our councils with near-crippling financial obligations and, as we now know, have too often failed to deliver on even the basic standards of results required. Just what these deals are and why they have been used is a topic which requires a bit of discussion.

PPP/PFI

Public Private Partnerships, of which Private Finance Initiatives are a specific type, are a form of capital investment introduced to the UK in the early 1990’s by Major’s Conservative government as an alternative to tradition procurement methods of the time. In traditional public investment models a local authority might decide to build an asset such as a school itself in a purely publicly funded model or it might contract a private source to build the school and then take over the full running costs of the project afterwards. The Tories were driven by an ideological pledge to reduce the budget deficit (then known by the catchy title of “public sector borrowing requirement“) and identified the use of PFI as a means to do this.

Instead of paying for a project out of the capital budget either up-front or over the span of the construction phase, PFI would spread the costs over a medium or long term contract, often more than 20 years. This reduced the single year outlay and hence massaged the budget figures.

It was under the Labour government though that PFI really took off as it had the advantage of taking capital debts “off-book” and allowed Gordon Brown to simply stop counting them towards the deficit entirely. This gave the illusion of the fiscal prudence on which he banked much of his reputation. This was doubled down in Scotland by Jack McConnell’s Labour/Lib Dem government which led to Scotland, with 8.5% of the UK population, ending up with some 40% of the UK’s PFI funded schools.

The lie to the illusion can be found in the realisation that the private sector doesn’t work for free. These contracts almost certainly mean that the total cost to the council over the lifetime of the council is significantly larger than the up-front capital costs.

To take a recent example concerning some of the schools in Edinburgh, the private company involved will be paid £12 million per year for 30 years for a project valued at £68 million in up-front costs and an additional £84 million in management costs. Subtracting the running costs, this represents an annualised return on capital investment for the company of 10% per year. For contrast, David Cameron’s offshore tax haven shares “only” earned him about 6.75% per year.

And this doesn’t even represent the worst example of increased costs due to PFI. Contracts worth three or four times the capital investment are common. Some have been found to be worth a staggering ten or even twelve times the total outlay.

It is these ongoing payments which are particularly affecting our own regional councils and the problem is only going to get worse with the peak of the outgoing payments not expected to hit till the mid 2020’s.

Whilst one of the advantages of PPP’s often touted is the obligation for the private company to maintain the asset over the lifetime of the contract this can be a double-edged sword. One of the other “advantages”, mentioned in the UN ESCAP video above, is the “realisation of private sector efficiency savings”. That can mean “cutting-corners” to you and me. If the company is required to maintain a school for only 30 years but is then free from that obligation on year 31 then the inducement to build to the minimum possible standards to see out that contract is strong. Indeed, there is some anecdotal eyewitness evidence that exactly this has taken place. Schools which, by today’s standards are insufficient but which nonetheless stood for more than 100 years are being replaced with buildings designed to last less than a quarter of that and, has been seen, sometimes don’t even make it that far. This is not “long term planning”. It is certainly not helped by the generally low standards of our building regulations. A private company will rarely build at anything other than barely above the minimum legal standards so if we’re going to continue involving “the market” in our infrastructure projects then we’re going to need to have a discussion about increasing those standards to something more suitable for the 21st century. Whilst PFI specifically may have been abandoned in Scotland, this discussion over standards remains.

LOBO Loans

Lender Option, Buyer Option loans make up a far smaller proportion of council borrowing than PPP/PFI and have hit fewer headlines but they are still a symptom of the chronic dysfunction of our public borrowing system.

These loans were launched in 2000 as an alternative to the National Loans Fund which, whilst cheap and stable due to being funded by UK gilts, are sometimes quite limited in scope and therefore not always avaliable when required. Instead, the public body can approach a commercial bank for a long term, often more than 40 years, loan which is offered at an initially low “teaser rate” but which includes a clause which allows the lender to change the interest rate, usually upwards, are regular, often annual, intervals.

Sometimes these rate adjustments carry with them a contract exit clause but one can imagine the conversation in that case.

Bank: “So, we’re planning on increasing your interest rate from 2% to 5%. Under Section 4 of our contract, you can exit the loan by paying back the outstanding primary plus our exit fee.” Council: “If we had that kind of money, we wouldn’t have needed the loan.” Bank: “Ok. 5% it is. See you next year!”

These loans were often offered to and accepted by councils without the council quite appreciating the potential volatility and uncertainty that these changes would represent, which is quite understandable as these contracts have been criticised as being some of the most complex in the financial world and as our locally elected representatives aren’t necessarily chartered accountants it’s perhaps understandable that some would have simply been sucked in by those teaser rates which, at the time, undercut even those bonds offered by the NLF.

What Next?

I’m not going to pretend I have a magic solution to all of this. Some have discussed simply canceling and renationalising PFI funded assets but whilst I have some sympathy for this I have concerns also. Right now, we simply don’t know how far the record of substandard workmanship within the works built runs and, in fairness to the companies behind this disaster, they are upholding their obligation to pay the costs of repair and, if required, rebuild of these schools. If the contracts were canceled before we know the extend of the repair bill then we might simply be bailing out a huge debt. I can see some kind of scope for some kind of renegotiation over the annual payments or contract terms, perhaps with some kind of profit cap. Perhaps the companies could be offered an exit but made to put up a bond in case future issues arise although as we’ve seen from the coal and, more recently, the steel industry those bonds themselves need to be planned carefully lest they prove insufficient or evadable.

In future, a more sustainable method of public borrowing and investment needs to be examined. The Common Weal has a proposal to use a mutual limited company to leverage funds backed by Scottish issued bonds to invest in our public infrastructure which is perhaps one of the better ways to go about this issue although it is acknowledged that Scotland’s very limited borrowing powers even under the “new powers” of the Scotland Act 2015 will likely cap the viability of such a scheme. Obviously, an independent Scotland wouldn’t have that problem but until that’s sorted, we may need to think of something else.

Economics: The art of explaining why all of your models fail to predict either the future or the past.

Click image above for data

It’s that time of year again when everyone starts looking at the first page of a dense booklet of economic data and uses it to wildly forecast despite long known limitations in doing so. So it’s also, once again, time for me to try looking a little further to tease out some details that others might have missed.

First, to get some of the headline figures out of the way. There has been a slump in offshore oil revenue due, largely, to the crash in the oil price resulting from the ongoing economic conflict going on between Saudi Arabia and the US.

This has caused oil revenues to drop from £4.0bn in 2013-14 to £1.8bn in these current figures. And thus came sic a cry of a “>£2 billion BLACK HOLE” from certain sources…

…except…total current revenue is only down £600 million. Down from £54.050 billion last year to £53.443 billion this year. That’s just a touch over 1% of a change and is comparable to some of previous year’s “budget underspends“, thus it could even be said to be within the margin of error of budget estimates. So what is going on?

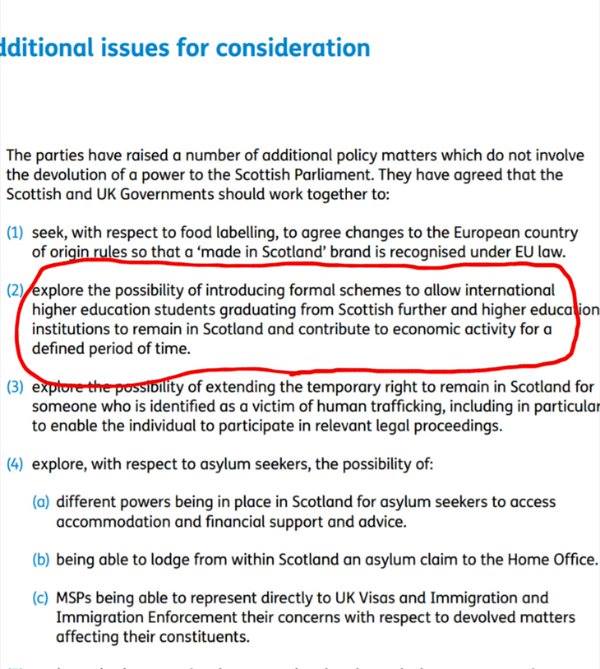

The relevant passage from the Smith Commission Report. Page 28.

David Mundell, who is currently crowing that the Smith Commission has been delivered “in full”, has just blocked a key element of it.

All of the Smith parties agreed to consult on the possibility of allowing Scotland to issue post-study visas for visiting students to allow them to continue working (and paying taxes) in Scotland, the country which educated them, after they graduate.

Mundell has just blocked that proposal without such consultation and before the Scottish Affairs Committee looking into it has even had a chance to report back. (Story here)

One of the most upsetting moments in my own personal indyref campaign was hearing from a young lass whose partner was one such visiting student. He had come to Scotland to study engineering and, after falling in love both with our country and one of its inhabitants he decided that he wanted to stay, to build his career and to make Scotland his home. Just two weeks after his graduation, the UK Government rewarded his endeavour with arrest, incarceration in Dungavel and deportation.

Protests outside the Dungavel Detention Centre. Source: Wikipedia.

This is not how a civilised country should treat other human beings. Instead, we should be encouraging those who, after all, pay significant sums of money towards their education to find a place within Scotland should they choose to do so. Many will find high paid, highly skilled and highly sought after jobs. Many others will start businesses of their own and CREATE those same jobs. Even the graduates who choose to leave Scotland will, if they are treated with respect, go on to strengthen our trade and business links with the countries to which they go. Something to bear in mind with respect to the UK’s worrying trade deficit combined with a currency value currently at the lowest level since the Tories took power and which is rapidly approaching the weakest value it’s had in 30 years.

Think about it David. If you were incarcerated and forcibly ejected from here simply because you had graduated, would you look upon this country favourably afterwards? Of course not. Would you consider sending your kids to study in a country which threatened to do the same to them? Of course you wouldn’t.

As Smith notes, this policy doesn’t require any additional powers to be devolved, indeed the similar Fresh Talent scheme used to be implemented in Scotland between 2005 and 2008 and was rolled out successfully to the entire UK until 2012 when it was scrapped by the Coalition government. Mundell’s decision therefore seems especially arbitrary, short-sighted and, frankly, smacks of nothing less than a jumped-up Governor throwing his weight around simply because he thinks he cannot be challenged.

The European Court of Justice has released its judgment of the Scottish Government’s proposals to introduce a minimum unit price on alcohol.

Their judgment, published here, states that the proposals as written would be illegal on the grounds of being discriminatory towards cheap alcohol imports and thus would be a restriction on the free movement of goods within the EU.

They have, however, upheld the Scottish Governments arguments that MUP would lead to substantial health and social benefits and have agreed that it would, indeed, meet the goals of both reducing hazardous alcohol consumption and alcohol consumption in general (in an earlier article I noted that Scottish consumption of alcohol can be seen as substantially higher than the UK average simply by examining the tax records).

The court has therefore not banned MUP completely but has ruled that it cannot be implemented until and unless the national courts (i.e. Edinburgh and then the inevitable appeal to the Supreme Court in London) rule that the same alcohol reductions cannot be achieved via taxation. This sets out a test to be met by the Scottish Government.

But if that test is failed and taxation ruled appropriate, what form could it take?

The obvious first step would be alcohol duty but this is currently a reserved power and its devolution was ruled out of the Smith Agreement and the subsequent Scotland Act 2015 Bill. I would think it unlikely, given the current track record, that an amendment to devolve alcohol duty would succeed at this point so I think I’m safe in assuming that it will remain in Westminster hands. Nor, do I suspect, will George Osborne be keen to adjust his own plans for the UK simply to allow the Nationalists even a moment of victory so I can’t see him being amenable to changing alcohol duty at UK level either.

There is another way though, as pointed out by Andy Wightman on Twitter today, the Scottish Government currently DOES have the power to create new LOCAL taxes. If the courts ultimately agree with the ECJ that taxation would be just an effective method of reducing alcohol consumption as MUP then this would be a method within the competence of the Scottish Government to implement without further devolution or delay.

Such a tax need not be set locally, national legislation could fix the rate, though the advantages to doing so are quite strong. By keeping money within areas particularly blighted by alcoholism and alcohol abuse and by allowing the rates to be set to particularly target these areas the greatest good could be done the fastest. Conversely, those areas which perhaps see a lot of through traffic, people traveling into town for a responsible night out say, but suffer little actual harm from chronic abuse may wish to set rates somewhat lower so as to avoid driving away too much business.

While we’re looking at locally devolved alcohol sales taxes we could also take the advantage of the discussion to bring back proposals for alcohol production taxes too. Scotland is perhaps best known for its whisky exports but what is lesser known is the fact that many of the most famous distilleries actually employ comparatively few people and yet produce vast sums of money for their generally multinational corporate owners without doing all that much for a local area which often gives their very name to that drink. Given that these distilleries, and many brewers and other manufacturers, cannot easily move elsewhere (and certainly cannot move out of Scotland) then a local production tax seems particularly apt. Again, by setting it locally and by allowing local people a say in how it is set then they are in a position of power again and can directly benefit from our renowned exports.

Personally, I welcome the prospect of minimum unit pricing and do believe that it would be an effective aid to our national alcohol problem but my challenge to the government is that if the courts rule otherwise, there is still something we can do. Indeed, even if they don’t….why not both?

Next year brings in the Scottish Parliamentary Elections and with it comes the proposals from each of the parties on how best to use the limited powers that the Scottish Government will have at its disposal. No doubt, much of the news and comment will be around whether or not the (marginally) expanded powers over income tax coming in under the Scotland Bill 2012 will be used and by how much.

Our approach towards local taxation, however, will perhaps lead to a far more fundamental change to the fabric of our society. There is also far greater scope within the devolution powers to do something a bit more radical that simply raising or lowering the rate of tax by a penny or so (or repeatedly defending one’s reasons for not doing so). It is therefore important, before the campaigning season begins in earnest, to understand what our options are and the potential impacts of them.

(click image for full report)

(click image for full report)

{kind=link}

{kind=link}