“I would say is that every public-private partnership in Scotland has delivered new hospitals or new schools in Scotland on time and within budget and that’s the sort of success I want to see in every building.” – Jack McConnell, 2002

Oxgangs Primary School, 2016. Built by PFI in 2005

The dramatic news from Edinburgh in the past couple of weeks has put into sharp focus the failures of some of the finance models used by our regional councils to build schools, hospitals and other public buildings in recent years. Public/Private Partnerships (PPP), Private Finance Initiatives (PFI) and, less well known, Lender Option, Buyer Option (LOBO) Loans have burdened our councils with near-crippling financial obligations and, as we now know, have too often failed to deliver on even the basic standards of results required. Just what these deals are and why they have been used is a topic which requires a bit of discussion.

PPP/PFI

Public Private Partnerships, of which Private Finance Initiatives are a specific type, are a form of capital investment introduced to the UK in the early 1990’s by Major’s Conservative government as an alternative to tradition procurement methods of the time. In traditional public investment models a local authority might decide to build an asset such as a school itself in a purely publicly funded model or it might contract a private source to build the school and then take over the full running costs of the project afterwards. The Tories were driven by an ideological pledge to reduce the budget deficit (then known by the catchy title of “public sector borrowing requirement“) and identified the use of PFI as a means to do this.

Instead of paying for a project out of the capital budget either up-front or over the span of the construction phase, PFI would spread the costs over a medium or long term contract, often more than 20 years. This reduced the single year outlay and hence massaged the budget figures.

It was under the Labour government though that PFI really took off as it had the advantage of taking capital debts “off-book” and allowed Gordon Brown to simply stop counting them towards the deficit entirely. This gave the illusion of the fiscal prudence on which he banked much of his reputation. This was doubled down in Scotland by Jack McConnell’s Labour/Lib Dem government which led to Scotland, with 8.5% of the UK population, ending up with some 40% of the UK’s PFI funded schools.

The lie to the illusion can be found in the realisation that the private sector doesn’t work for free. These contracts almost certainly mean that the total cost to the council over the lifetime of the council is significantly larger than the up-front capital costs.

To take a recent example concerning some of the schools in Edinburgh, the private company involved will be paid £12 million per year for 30 years for a project valued at £68 million in up-front costs and an additional £84 million in management costs. Subtracting the running costs, this represents an annualised return on capital investment for the company of 10% per year. For contrast, David Cameron’s offshore tax haven shares “only” earned him about 6.75% per year.

And this doesn’t even represent the worst example of increased costs due to PFI. Contracts worth three or four times the capital investment are common. Some have been found to be worth a staggering ten or even twelve times the total outlay.

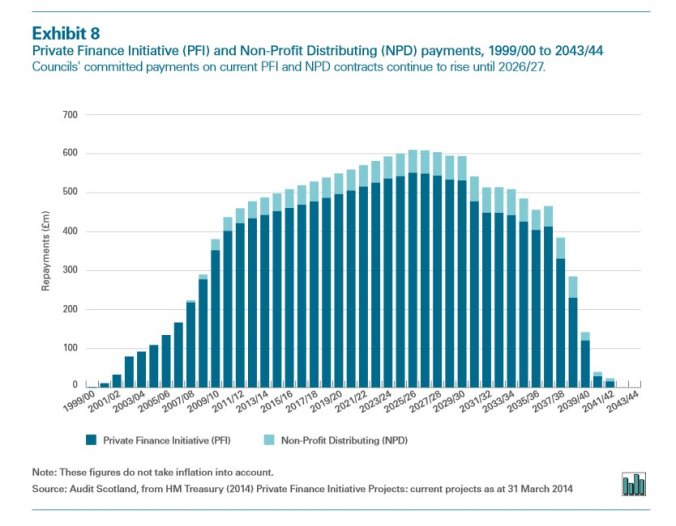

It is these ongoing payments which are particularly affecting our own regional councils and the problem is only going to get worse with the peak of the outgoing payments not expected to hit till the mid 2020’s.

Whilst one of the advantages of PPP’s often touted is the obligation for the private company to maintain the asset over the lifetime of the contract this can be a double-edged sword. One of the other “advantages”, mentioned in the UN ESCAP video above, is the “realisation of private sector efficiency savings”. That can mean “cutting-corners” to you and me. If the company is required to maintain a school for only 30 years but is then free from that obligation on year 31 then the inducement to build to the minimum possible standards to see out that contract is strong. Indeed, there is some anecdotal eyewitness evidence that exactly this has taken place. Schools which, by today’s standards are insufficient but which nonetheless stood for more than 100 years are being replaced with buildings designed to last less than a quarter of that and, has been seen, sometimes don’t even make it that far. This is not “long term planning”. It is certainly not helped by the generally low standards of our building regulations. A private company will rarely build at anything other than barely above the minimum legal standards so if we’re going to continue involving “the market” in our infrastructure projects then we’re going to need to have a discussion about increasing those standards to something more suitable for the 21st century. Whilst PFI specifically may have been abandoned in Scotland, this discussion over standards remains.

LOBO Loans

Lender Option, Buyer Option loans make up a far smaller proportion of council borrowing than PPP/PFI and have hit fewer headlines but they are still a symptom of the chronic dysfunction of our public borrowing system.

These loans were launched in 2000 as an alternative to the National Loans Fund which, whilst cheap and stable due to being funded by UK gilts, are sometimes quite limited in scope and therefore not always avaliable when required. Instead, the public body can approach a commercial bank for a long term, often more than 40 years, loan which is offered at an initially low “teaser rate” but which includes a clause which allows the lender to change the interest rate, usually upwards, are regular, often annual, intervals.

Sometimes these rate adjustments carry with them a contract exit clause but one can imagine the conversation in that case.

Bank: “So, we’re planning on increasing your interest rate from 2% to 5%. Under Section 4 of our contract, you can exit the loan by paying back the outstanding primary plus our exit fee.”

Council: “If we had that kind of money, we wouldn’t have needed the loan.”

Bank: “Ok. 5% it is. See you next year!”

These loans were often offered to and accepted by councils without the council quite appreciating the potential volatility and uncertainty that these changes would represent, which is quite understandable as these contracts have been criticised as being some of the most complex in the financial world and as our locally elected representatives aren’t necessarily chartered accountants it’s perhaps understandable that some would have simply been sucked in by those teaser rates which, at the time, undercut even those bonds offered by the NLF.

What Next?

I’m not going to pretend I have a magic solution to all of this. Some have discussed simply canceling and renationalising PFI funded assets but whilst I have some sympathy for this I have concerns also. Right now, we simply don’t know how far the record of substandard workmanship within the works built runs and, in fairness to the companies behind this disaster, they are upholding their obligation to pay the costs of repair and, if required, rebuild of these schools. If the contracts were canceled before we know the extend of the repair bill then we might simply be bailing out a huge debt. I can see some kind of scope for some kind of renegotiation over the annual payments or contract terms, perhaps with some kind of profit cap. Perhaps the companies could be offered an exit but made to put up a bond in case future issues arise although as we’ve seen from the coal and, more recently, the steel industry those bonds themselves need to be planned carefully lest they prove insufficient or evadable.

In future, a more sustainable method of public borrowing and investment needs to be examined. The Common Weal has a proposal to use a mutual limited company to leverage funds backed by Scottish issued bonds to invest in our public infrastructure which is perhaps one of the better ways to go about this issue although it is acknowledged that Scotland’s very limited borrowing powers even under the “new powers” of the Scotland Act 2015 will likely cap the viability of such a scheme. Obviously, an independent Scotland wouldn’t have that problem but until that’s sorted, we may need to think of something else.

![]()

Discover more from The Common Green

Subscribe to get the latest posts sent to your email.

Pingback: We Need To Talk About: GERS (2015-16 Edition) | The Common Green

Pingback: The Common Green’s 2016 Retrospective | The Common Green