Source: Flickr

Next year brings in the Scottish Parliamentary Elections and with it comes the proposals from each of the parties on how best to use the limited powers that the Scottish Government will have at its disposal. No doubt, much of the news and comment will be around whether or not the (marginally) expanded powers over income tax coming in under the Scotland Bill 2012 will be used and by how much.

Our approach towards local taxation, however, will perhaps lead to a far more fundamental change to the fabric of our society. There is also far greater scope within the devolution powers to do something a bit more radical that simply raising or lowering the rate of tax by a penny or so (or repeatedly defending one’s reasons for not doing so). It is therefore important, before the campaigning season begins in earnest, to understand what our options are and the potential impacts of them.

The Principles of Taxation

Why do we tax people in the first place? It’s a substantial chunk out of your paycheck every month and there’s not one of us who has, at some point, wondered what they could have done with that money instead.

The reasons for taxation are broadly covered by three principles:

Revenue Generation:- There are many services, such as roads, emergency services, healthcare, education etc, which we, as a society, have decided are best funded collectively. We may argue over just how much is paid for in this way and how much is funded ad hoc or privately but there are vanishingly few full blown anarcho-libertarians, especially in Scotland, who believe that absolutely everything should be in private hands and that Government shouldn’t exist at any level. For everything else, taxes are collected to fund the State and its operations.

Redistribution:- Societies are rarely entirely equal at every level. Some people end up earning or accumulating more than others, some people end up not earning enough money to meet their basic needs. Some regions end up with a greater concentration of wealth than others. Some, due to size or geographical constraints (such as the Highlands and Islands) simply require more funds to deliver the same level of services than others. It is well known that more equal societies experience greater levels of wellbeing and lower levels of ill health and other negative effects. Most societies, therefore, employ tax, alongside policies such as social security and welfare, in a progressive manner such that the richer pay more according to their abilities and the poorer gain more according to their needs.

Reshaping:- This is the carrot-and-stick approach of taxation. Governments often develop policies designed to encourage their citizens towards certain activities or discourage them from others. One prominent example at the national level would be the levies on tobacco and alcohol which are, at least partly, there to try to encourage us to smoke and drink less (obviously, taxes can fall into multiple categories and the Revenue Generation aspects of these taxes cannot be discounted, especially when used improperly)

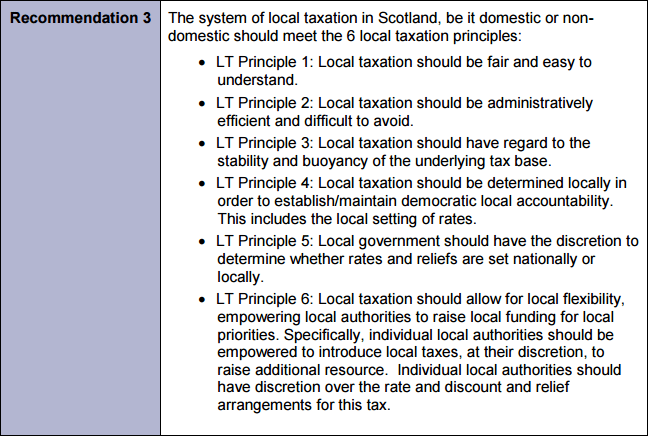

In addition to these principles on the purpose of a tax, we must consider how it is structured so that it works in an effective manner. In 2013, local council body COSLA published a report into the effectiveness of current local taxes and in it laid out six principles outlined below.

Essentially, these principles boil down to taxes being fair, easy to manage and employing a sense of subsidiarity whereby local powers should, wherever possible, be used to effect local solutions. Whenever discussing a potential local tax, all of these principles must be upheld or accounted for.

So what options are either currently used in Scotland or open to us?

Local Taxation

The “Poll Tax”

Let’s start with the most infamous one, shall we? If you’re much over the age of 30 then you’ll probably remember this period of Scottish history first hand and even if not you’ll probably know something of the long shadow it has cast to this day.

Throughout her tenure as Prime Minister, Conservative Margaret Thatcher made repeated attempts to reform the then existing system of local property rates based on the notional rental value of said property with a flatter tax levied on residents instead. The eventual result was the Community Charge which saw a flat tax per person regardless of income (although there was a reduction for those on lower incomes). The Poll Tax was introduced in England and Wales in 1990/91 though, through the machinations of Tory politicians saw the tax introduced in Scotland a year earlier (It was never introduced into Northern Ireland at all). This move was widely seen as using Scotland as a “guinea pig” to test public tolerance of the tax.

Needless to say, the public tolerance was rather low. One of the largest protest campaigns Scotland and the UK had ever seen was born on the outrage caused by this policy and many figures currently at the top of Scottish politics today cut their teeth at hustings and protests against the tax. Ultimately, the protests intensified to the point of violence in London and the infamous Poll Tax Riots of 1990. The tax would eventually be abolished in the 1992 budget and replaced with the Council Tax.

The tax itself was indeed, extremely unfair as its deeply regressive nature saw the poorest paying a greater proportion of their income towards the tax (even after reductions) than richer people and poorer people lost out comparatively compared to the old rates system whereas many of those who were actually implementing the tax would see personal savings compared to the old system. Scottish politics in particular were profoundly affected with the Tories becoming deeply poisoned by the episode. To this day, the words “Tory” and “Poll Tax” are very nearly the worst curses one can accuse of another or their policies within Scottish political circles. It’s fair to say that any politician who wished to re-introduce this tax to Scotland may find themselves very quickly leaving office.

Council Tax

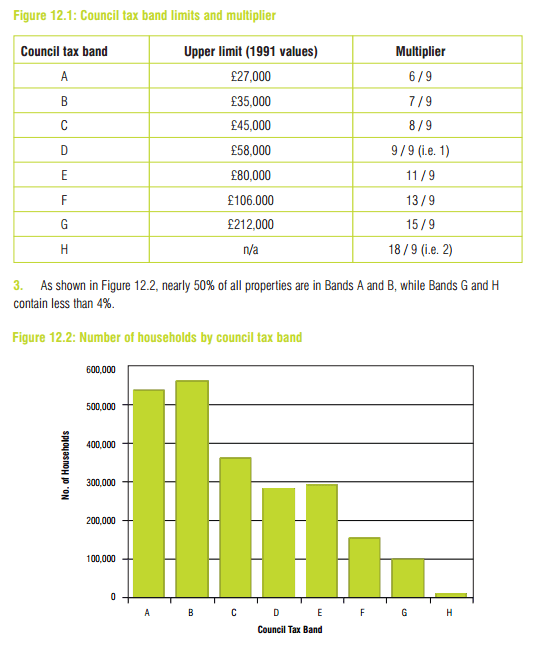

The abolishing of the Poll Tax led to a crisis for the Conservatives as they couldn’t go back to the old Rates system for ideological reasons (and, anyway, people often complained that they couldn’t easily calculate what their house value was so what rates were due and house price changes led to a need for frequent revaluations). Instead, a fudge was constructed in the form of the Council Tax. Instead of being calculated simply on house price, houses were divided into pricing bands based on their 1991 value (or value at construction if built after 1991) and a semi-progressive scale was introduced.

The Council Tax bands and number of Scottish houses in each band. Source: A Fairer Way, pg 121-122

Compared to the previous system, it was comparatively well received but now, more than 20 years later, it is starting to show its age. Governments of all parties have been loathed to touch the banding or even to revaluate the housing stock leading to many situations where a small, older house can attract a significantly higher council band than a larger, newer property. Whilst the scale is more progressive than the Poll Tax it is still not particularly progressive. A multi-million pound mansion will only attract three times the tax levy than a cramped bedsit despite the difference in property value being ten times or more. We have also witnessed in recent years a sustained property bubble taking place which has seen property values increase far faster than the income of the occupants. If a rebanding were to take place it could easily result in many poorer people losing out significantly. Hardest hit could be pensioners who have lived in home for decades and have seen the area gentrify around them.

Instead, both bands and rates have been frozen for many years which has been putting pressure on the funding sources for local councils as budgets are now routinely squeezed by Austerity. Whilst the Scottish Government have been making up funding shortfalls in recent years by increasing the council block grant to compensate this, itself, has been attacked as a breach of the principles of Subsidiarity and a sign of increasing centralisation by the government and a pulling away of council’s local powers. As with Income Tax, though, the Council Tax is an extremely “visible” tax. Almost every voter will notice it when it does change and whether a government is practicing the principle of “Do No Harm” or whether it is simply succumbing to the realpolitik of trying not to annoy potential swing voters I rather suspect that it is far easier for an opposition party to complain about lack of change than it is for a government to actually implement it. That said, even the current Scottish Government acknowledges that something does need to change and alternatives need to be explored.

Capital Asset (Mansion) Tax

Similar to the Council Tax, this is a tax on particularly valuable housing, primarily to combat the tendency towards the kind of speculative property bubbles currently being experienced. In principle, this could be thought of as an additional “band” of Council tax taking effect for property prices above a certain threshold (recent Liberal Democrat proposals suggested above £2 million). One of the principle criticisms of this tax was, again, due to the rampant housing bubble in the UK many of these “mansions” were, in fact, simply pensioners houses which had disproportionately increased in value without any control or input from the resident themselves. The principle of ability to pay would therefore be compromised. It was this (especially as pensioners tend to be rather more keen to vote than other age groups) which led to the Lib Dems largely dropping plans like this in the past year or so.

Another criticism of this tax is that any tax set for the UK would simply not be suitable for Scotland as house prices are so much lower than the SE that any single threshold simple wouldn’t make sense. There may be scope for the principle of subsidiarity to be applied and for individual councils to set the rates and thresholds to suit their own distribution which would be easiest done via integrating it into the Council Tax system but this itself would fall into the pitfalls of the Council Tax as outlined above.

Local Income Tax

When the Scotland Act 2015 provisions come into force in circa-2018 (assuming Scotland is still part of the UK then) then Income Tax will be nearly fully devolved to Holyrood. This will put Scotland in a position nearly unprecedented in the modern world. All of the income tax you pay will go to the devolved government in Edinburgh. None will go to Westminster and none will go to your local (directly) council. This stands in direct contrast to countries like, for example, Norway where roughly 46% of income tax paid stays in the local community (which is far smaller than our “local” councils), 9.5% goes to the regional council and 44.5% is sent to central government [Source here].

Back here there have been some limited attempts at replacing the Council Tax with a local income tax, notably the Scottish Socialist Party’s proposals in 2004, knocked back largely on grounds of the specifics of the numbers rather than the principle, and 2007 SNP proposals for a 3p flat rate income tax which was stymied by warnings from HMRC over issues surrounding collecting and distributing the tax, a view that it was stripping local councils of their locally controlled power (ironically, this led to the continuing Council Tax freeze which has met the same complaint about loss of council control) as well as a warning from Westminster that the tax changes would result in the loss of £400 million worth of Council Tax Benefit receipts.

There is a lot to be said about some kind of LIT though. It has a key advantage of being both proportional to income (even when used as a flat tax without a progressive element) and keyed directly to ability to pay. When taxes are levied purely on property the biggest losers are those who are capital rich but cash poor (such as pensioners) or those who lose their jobs suddenly yet still have substantial taxes to pay. On the other hand, the introduction of a local income tax would hit groups such as young workers still living with their parents who are earning but neither own nor rent property.

Land Value Tax

One of the Greens’ keystone policies, the Land Value Tax is designed less from a revenue generation perspective as the like of Local Income Tax are and more for their ability to reshape the fabric of our society. Specifically, the horrendous patterns of land ownership in Scotland, from vast estates owned by absentee landlords, or even companies based in offshore tax havens, who make it difficult for local people to develop their communities through to large supermarket companies buying land and then leaving it deliberately fallow to “bank” it against speculative price rises or even just to block their competition from a prime spot. A Land Value Tax is a levy on value of the land owned rather than the value of the property built (or not built) upon it. This means that an acre left banked and unused would cost the owner as much as if it were fully developed. The actual valuation can be adapted locally to suit local needs and various reductions or additional levies could, in principle, be applied to encourage particular types of development on land.

As far as revenue generation goes, the LVT can be used in a manner similar to the Council Tax where the size of your house plus garden etc determines the payment rather than strict value. One could, alternatively, imagine a system of multiple taxes where one’s first acre (for example) was zero rated (perhaps then increasing progressively depending on how much land is owned) and a Council tax or Local Income Tax is applied as well (though in this simple example care would have to be taken to not penalise people who rent from a landlord with a large portfolio).

This tax represents a significant departure from anything tried in Scotland in modern times so the assessment, collection and enforcement of this tax, especially with regard to the large estates, is likely to be challenging (and challenged, legally, by those with access to powerful and expensive lawyers). I remain hopeful that the ongoing Land Reform debates will be brave enough to tackle these problems and to find solutions to them.

Green member and candidate in the 2016 elections, Andy Wightman has been running a tour outlining his proposals for Land Value Tax including how, precisely, to set a fair rate and band for any given section of land.

Conclusion

As has been seen there are many and various aspects to be looked at with regards to local taxation and the ongoing debate must look beyond simple revenue generation and “how much this family will gain/lose”. These taxes are about a great deal more than this and their ability to shape our society in the direction we want it to (which, of course, may differ greatly from political party to party) will be the hardest aspect to grasp, explain and actually achieve. This must be attempted though if we’re going to have a chance at any kind of meaningful discussion.

The 2006 white paper “A Fairer Way” by the Local Government Finance Review Committee remains, in my opinion, one of the best primer papers on the subject of local taxation (the fact that it is almost ten years old and not much has changed since then perhaps highlights the difficulty of the problem and the growing need for a solution) and makes the point clear that no single tax will ever achieve all of the outcomes of revenue, redistribution and reshaping simultaneously and satisfactorily. To truly make a difference, local councils will need the power over several taxes and these taxes need to be set locally by the people who live there to best suit the needs of the community (we also need our “local” councils to be more accountable and a lot smaller…but that’s for another article).

Those wishing to learn more should also read the COSLA report referenced earlier, especially its section on comparisons with other EU countries.

Finally, Andy Wightman is quite probably Scotland’s leading expert on Land Reform and Land Value Tax. His blog can be read here.

![]()

Discover more from The Common Green

Subscribe to get the latest posts sent to your email.

Pingback: Senatus Populusque Caledoniae | The Common Green