“Journalism is what we need to make democracy work.” – Walter Cronkite

It’s that time of year again. Amazingly, despite the looming catastrophe that is Brexit, this week has been one of those “slow news” weeks. Of the kind that manage to get pages out of very minor things like essentially reprinting old stories with the numbers slightly updated.

I am, of course, talking about the perennial “Scottish Government Underspend” story.

I covered this before back in the early days of this blog (it remains the most read article on here so far – even excluding the annual reposts). Others, like Wings Over Scotland, have covered it pretty much every year since.

Here’s the short version though.

- Opponents are complaining that the Scottish Government aren’t spending everything they’ve been given in the Block Grant or raised through taxes and are claiming that the Government are starving services of resources.

- This year the “underspend” is “almost £500 million” (actually, the article later says that it’s £453 million).

- But the Scottish Budget is pretty much fixed annually.

- And the Scottish Government has extremely limited borrowing powers for revenue – £600 million per year, £1.75 million maximum.

- If it DID try to use them, you can bet that the same opponents would be raging at the thought of the Scottish Government going into debt.

- The solution to avoid debt is to budget conservatively – if you had to set an ice-cream cone budget at the start of the year but your ice-cream purchases varied between 800 and 1,200 cones depending on weather – you’d need to budget for 1,200. If you only bought 800, then you’d have a 400 ice-cream cone underspend.

Without borrowing powers or an independent currency, budget underspends are an inevitable feature of the annual budget.

Though complicating the above point is that until 2006-07, Scottish Executive underspends were, in great part, retained by the UK Government. This was corrected after a negotiation between the UK Government and the then new SNP Scottish Government and the accumulated £1.5 billion was gradually fed into the budgets of the next several years.

Since then, underspend money gets carried over to next year’s budget (though, as that budget will have an underspend too it’s a bit of a moot point).

One thing often missed in the “Budget Underspend” headlines is the actual nature of the sum involved. It’s not all cash sitting in the bank. Some of it will be due to underspending due to less-than-projected spending items (like the ice-cream cone budget issue). Some of it will be due to projects coming in underbudget possibly due to good management, possibly due to currency or price fluctuations (if your ice-cream cones cost £1 in January but drop to £0.80 by June, you might underspend even if you still buy 1,200 cones).

But a good chunk of the underspend could be from things like depreciation of assets which can’t be spent on other things at all – even if the asset is sold (The metaphor gets a little strained here, but if your ice-cream cone is worth less as a half-eaten, melted pile than it was when you bought it fresh, it’s not as if you can sell the cone and pocket the difference in price).

Another thing often missing from these headlines is the inevitable revision afterwards – calculating National budgets down to the penny turns out to be quite tricky. If you remember last year’s headline that the government had underspent by £191 million, you probably missed the reporting that that figure was later revised down to only £85 million after final accounting adjustments were made.

Indeed, this year’s figures have ALREADY been revised downwards. Stripping out the non-cash items and money already budgeted for but not yet spent then it only leaves around £66 million to be spent on something else.

But £66 million is still a fair bit of money though isn’t it? Surely, the government could just, you know, budget better?

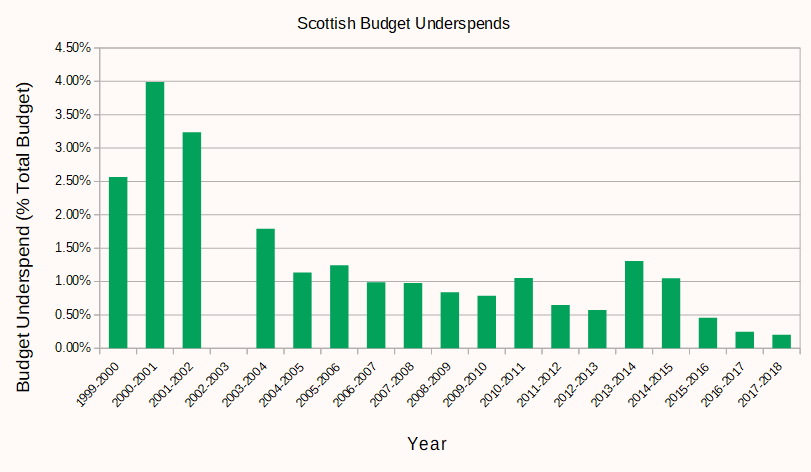

To answer that question we’d be best to do another thing that doesn’t really come across in reporting if one looks at the situation one headline at a time. Examine the trend.

To that end, I’ve spend a fair bit of time trawling through annual Consolidated Accounts to pull together the underspends from this and previous years. I managed to get back to the accounts for the year 2005-2006 before the trail gets fragmented. Before this point, the Scottish Executive accounts operated in a substantially different way (see the segment on Resource Accounting and Budgeting here). Underspends still happened, but comparing them like-for-like with years after 2004 may not be strictly fair. I also haven’t been able to locate the 2002-03 underspend at all.

As far as I can tell though and if the revision mentioned stands, this year’s underspend may well be the lowest since the start of devolution.

And if we compare the underspends to the budget as a whole we begin to see just how small a story this all becomes. The Scottish Government’s devolved budget is on the order of £32 billion. A £66 million underspend is about 0.21% of that budget – or about 18 hours worth of spending across the year.

Even the initial estimate of £453 million was about 1.4% of the total budget – if it really was all spendable cash, it’d be the equivalent of about five days worth of spending.

This is not to say that the budget underspend won’t become an issue. It was simplier back in the days when the bulk of the Scottish budget came from the block grant and tax powers were both limited and largely unused. Now, with divergent income tax rates and bands and an impossibly complex Fiscal Framework, there is a risk that the devolution settlement gets strained to breaking point. The David Hume institute has described it as an “interesting cocktail” of arrangements.

I don’t know what the future holds for this story. I could see a time, possibly as soon as next year, where the Scottish Government revenue budget slips from “underspend” to “overspend”. I already know what the reaction of the opponents will be if that happens.

I could hope that the media will up its game here and try to explain these issue in more detail than an attention grabbing headline.

Sadly, I can see my 2015 article just being reposted again in 2019.