“We bailed out the City 10 years ago when the crash came, we poured hundreds of billions of pounds into it. Since then £100bn has been given out in bonuses in the City. So we are asking for a small contribution…to fund our public services.” – John McDonnell MP

Last night, Labour announced one of their keynote policies ahead of the 2017 General Election. A financial transaction tax on the City of London. Time for a blog to outline just what in the name of Jim it actually is and what it’s supposed to do.

A Financial Transaction Tax, also known as a “Robin Hood” tax or a Tobin Tax – after one of its early proponents – is essentially a form of stamp duty on the purchase of stocks, shares, currency exchange and derivatives based on them. Every time you buy one of these applicable items or services, you pay a small tax on it. Often on the order of 1% or less of the value of the stock or share. If you later sell it, the person who buys it from you pays the tax again but there is no further payment should you simply hold on to it.

This policy is being largely sold on the basis that it could raise a substantial amount of revenue for the UK Treasury. Estimates are that Labour’s scheme of a 0.5% FTT could bring in up to £5.6 billion per year (about the equivalent of that brought in by insurance premium tax and all betting and gambling duties combined). There’s another, potentially more important, aspect to a tax like this though and that’s its power to reshape behaviour and the economy of the country.

The history of the idea is solidly rooted in the Keynesian school of economics with Keynes himself being a solid proponent of the tax in the mid-1960’s and with American economist James Tobin bringing it to attention again in the 1970’s as the Bretton Woods monetary arrangement broke down.

When Bretton Woods collapsed the advanced economies, including the UK, started experiencing exchange rate fluctuations between their trading partners. Tobin realised that this would present an opportunity for market speculation to profit from these fluctuations or for speculators to outright attack currencies which tried to maintain stable exchange rates. By taxing this activity at a level which discourages making these trades, especially those to try to make them rapidly and repeatedly, you can hopefully prevent them destabilising the greater economy.

Through the 1980’s and the Regan/Thatcher this fear would become magnified. The deregulations supported by those administrations coupled with increasing computational power brought in the ability to massively ramp up the frequency of trades. Now, instead of talking about holding on to shares for years or months or even weeks, traders increasingly started looking at holding on to shares for days, or hours, or minutes or even seconds. At this point one is no longer even pretending to invest in a company and hoping to support it as it grows. One is simply gambling on the basis of near-random noise and froth in the system.

And it gets more divorced from reality yet. The 1990’s saw the rise to prominence of the financial derivative market. Where before one would have to actually buy a stock or share in order to sell it for profit, the derivative market opened up something else entirely.

Imagine me buying a share on Monday, waiting for it to go up in value then selling it to you on Friday. Imagine instead I simply said to you “See that share? It’s worth £100 now. On Friday, if it goes up, you pay me the difference. If it goes down, I’ll pay you the difference. Deal?”

This is the wonderful world of the derivatives market in a nutshell.

Of course it gets worse. Maybe your friend sees our deal and says to his friend “Bet you £1,000 that Craig makes a profit on that contract”. And then people can create further deals and bets based on those deals and bets until the amount of money being traded is many, many times larger than the original real share on which the whole rickety pile rests.

Or, as it was so wonderfully outlined in The Big Short:

Today, automation and the derivatives market means that the London foreign exchange industry turns over some £730 billion worth of transactions PER DAY. and automated stock trading can turn over millions of shares every minute with barely any human interaction. The entire industry is now so complex that I doubt that anyone truly understands its complexity or from where the next big flaw or crash could emerge.

What is clear is that with the speed and ease of this kind of trading, those with the cash to splash have ever less incentive to invest in the real economy of actual goods and services. And why would you? Why would you go to all the effort to build a factory, fill it with plant and people and then wait months or years for it to start making money when you can just throw a pile of (someone else’s?) cash into the aether, move it from one pile to another until it magically comes back larger than it started and you make out with a profit in a couple hours tops?

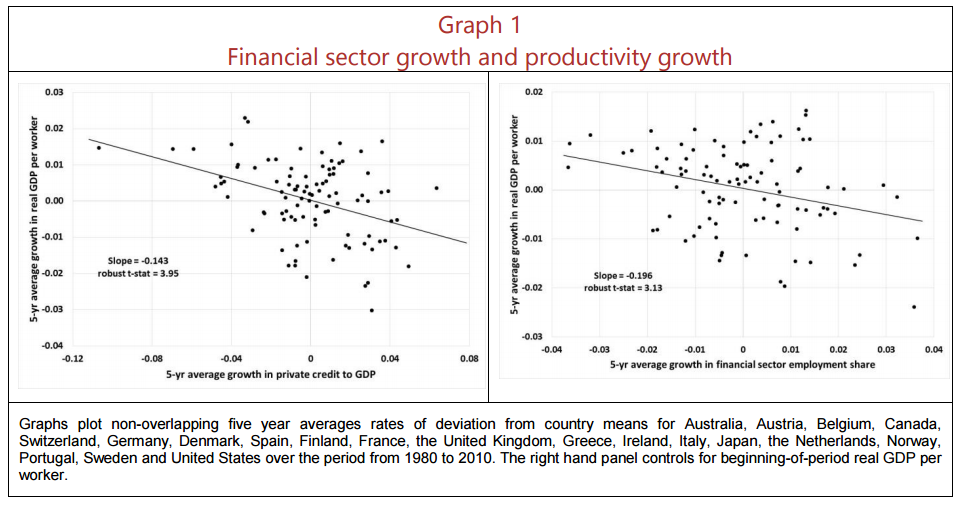

It’s no wonder that there’s a clear correlation between the growth in a country’s financial industry and the drop in productivity elsewhere. This kind of activity crowds out everything around it.

The financial transaction tax hits this kind of business the hardest. You might not notice at all an extra 50p on top of a £100 trade you make once to buy a share that you hold for ten years but you might notice if you were bouncing that £100 trade in and out once per second for a year. It’d cost you £15.8 million to do that. You might decide that investing in that factory suddenly starts to look like a better way to invest your money and we can move some of the UK’s economic activity outside of the Great Attractor that is London.

GDP/capita regional disparity in the EU28+EFTA. Compared to the rest of the EU, Britain isn’t Great. Britain is weird.

Of course it might also mean that you decide to move your gambling operation to another country which doesn’t have an FTT to which many might be just as fine with. This money isn’t part of the productive economy but you can bet as surely as you can that the finance houses which glut themselves with this business and demand ever lower taxes and fewer regulations will be the first to beg for a bailout and protection when the next crash they cause comes around. Maybe we’d like to insulate ourselves from that crash before it happens. Either way, our economy will be better for it.

So yes, I support Labour’s proposed Financial Transaction Tax, as the Green Party of England & Wales, the Scottish Greens and the SNP have for some time now. It offers a genuine chance to boost revenue and redistribute and rebalance the economy. It’s an exciting idea in an increasingly politically moribund age and I hope it should spark some passionate discussion on the topic. I’ll finish up with the Artist Taxi Driver who is currently doing a good job of infecting us with just that kind of enthusiasm. Let me know what you think in the comments.

![]()

Discover more from The Common Green

Subscribe to get the latest posts sent to your email.

Great article and clips. The finance sector clearly has many issues that should have been addressed ten years ago and still needs to be addressed sooner or later. It seems to me that the size of the banks/finance companies in the UK and their ability to control what changes are made, make sure that these are only done when it suits them.

Here’s a good video clip about banking in the UK. It would appear that a more local banking system similar to Germany may be part of a solution to the speculative focus and power of the big banks.

‘In the UK five banks account for 90% of deposits. In Germany big high street commercial banks account for just 12% of the deposit base. Over 70% of deposits are held by more than 1,000 local, not-for-profit community banks. In the following clip Prof. Richard Werner explains how the UK became one of the most concentrated financial sectors on the planet, and what it means for British people.’

https://renegadeinc.com/the-finance-curse-2/

LikeLike

This is top drawer! Excellent blog!

LikeLike

There is of course already a 0.5% Stamp Duty on share purchases in the UK. The Labour proposal would therefore double this existing tax. In my opinion, it certainly won’t change behaviour.

LikeLike

While I appreciate Dr Craig Dalzell’s explication of a very complex issue, I find it curious that he omits the SNP from his list of political parties which support the principle of a Financial Transaction Tax. This omission is highly regrettable as it sullies an otherwise excellent article with the taint of a political agenda. Or, at least, the possible perception of such.

LikeLike

I can assure that any such omission is simply because I would not presume to speak for the SNP. If you have a recent link to their plans for or support for an FTT at a Scotland, UK or EU level though I’d be happy to edit it in.

LikeLike

Please accept my apologies for taking so long to get back to you on this. As someone once said, events, dear boy, events.

The SNP’s support for a Financial Transaction Tax has been stated on a number of occasions. For example, the following from Alyn Smith MEP in May 2012,

SNP MEP Alyn Smith said:

“The SNP supports the principle of a tax on financial transactions, and is working alongside organisations such as Oxfam to promote this concept on a global level.”

http://www.alynsmith.eu/financial_transaction_tax_passed_by_parliament

The official SNP position was, perhaps, most concisely stated by then Finance Secretary John Swinney in an answer given in the Scottish Parliament on 17 April 2012.

Question S4W-06337: Mary Fee, West Scotland, Scottish Labour, Date Lodged: 20/03/2012

To ask the Scottish Executive whether it would implement a financial transaction tax in a Scotland separated from the rest of the United Kingdom.

Answered by John Swinney (17/04/2012):

The Scottish Government’s proposal for Scotland is independence with a new relationship of equality between Scotland and the other nations of these islands and a voice in Europe and the wider world.

The Scottish Government supports measures that enable a well functioning financial system and that improve access to finance, particularly for small and medium-sized businesses. We support the global application of the financial transaction tax to provide maximum benefit while avoiding the relocation of financial services.

LikeLike

Good article, thanks for that. The SNP support a banking tax as well by the way.

Cheers.

LikeLike

A great article (as always).

Apologies if this is an obvious question, but I was trying to figure out the gdp/capita graph: what are the two blue dots on the UK bar? Are they Edinburgh and London (“capital regions”)? I followed the link but couldn’t find anything.

LikeLike

It took me a little while to work out too when I first saw that dataset. The lower blue dot is the average for the whole London region. The upper blue dot is just the City of London.

LikeLike

I’m actually shocked, I did not expect that. The London dot is about right – it’s a normal European capital. ‘The City’ is some kind of abnormal growth on top of it. How do we even start sorting this? I know a transaction tax is the start, but do we know how much of this it’s going to solve?

LikeLike