The Croatian National Bank shall be the central bank of the Republic of Croatia. The Croatian National Bank shall be autonomous and independent, and shall report on its work to the Croatian Parliament. The Croatian National Bank shall be managed and its operations shall be conducted by the Governor of the Croatian National Bank. The organisation, purpose, tasks and remit of the Croatian National Bank shall be governed by law.

– Article 53, The Constitution of the Republic of Croatia.

Today sees the launch of my latest contribution to the Common Weal White Paper Project on the very important topic of Central Banking in an independent Scotland.

It has received a front page splash in The National which can be read here alongside a summary by me here.

And the paper itself can be downloaded here or by clicking the image below.

If, as I hope we should, Scotland uses the opportunity of independence to launch our own sovereign currency then one of the departments of government that we’ll need to set up is our own Central Bank. This paper outlines the principles that we’ll need to examine and follow as we design that bank.

“The Treasury…may by order give the Bank directions with respect to monetary policy if they are satisfied that the directions are required in the public interest and by extreme economic circumstances” – Section 19, Bank of England Act 1998.

Theresa May is getting nervous. She’s seen the polls slip away from her. She’s seen the abject rejection of conservative politics first in Scotland and now in England too. She has just admitted that she jumped into her personal snap election whilst her party was completely unprepared to fight it. She is far from “strong and stable.

And now she’s getting worried by the growing pull towards the more interventionist economic policy advocated by Jeremy Corbyn and has responded with a speech defending Austerity and celebrating free market economics on the day of the 20th anniversary of the independence of the Bank of England. And so has begun fairly vapid tirades warning against the “dangers” of nationalism and populism.

“Annual income twenty pounds, annual expenditure nineteen nineteen and six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.” – Dickens, David Copperfield

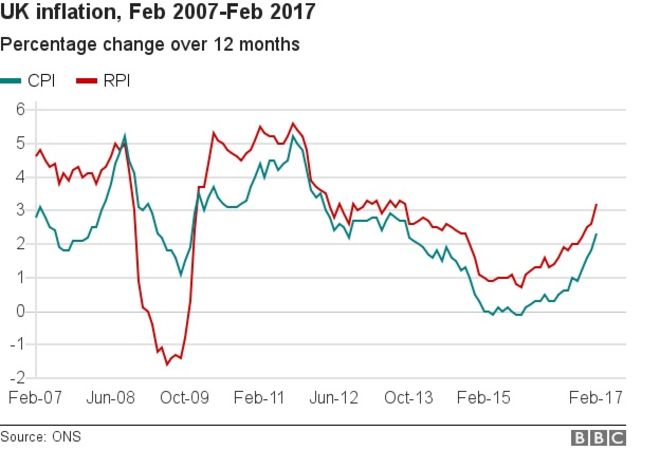

The shape of the next UK economic crisis has become apparent. It may have already begun and it’s not at all clear how it can be avoided or mitigated.

On the 23rd June 2016, the United Kingdom, for a variety of reasons, voted to leave the European Union. The immediate impact of this was an almost unprecedented drop in the value of the pound with respect to its major trading partner currencies.

Not much of a problem, the defenders said, as a weakened currency has its merits as well as demerits. Exports should become cheaper, which would boost foreign trade.

This may have been true in times gone by but economies have grown vastly more complex than this. Many products manufactured in the UK consist of sub-components drawn from multiple countries and globalised supply chains have grown STAGGERINGLY complex.

What this has meant is that even the goods that Britain manufactures here have seen their “input prices” increase, which has pushed up the price of goods even despite the fall in currency strength. Add to that, the fact that the UK imports far more than it exports – it has one of the largest trade deficits as %GDP in the OECD – and it becomes clear why prices have started rising again in Britain. After five years of declining inflation rates and almost a year of zero price increases, inflation has returned with a vengeance.

But this needn’t be a terrible thing. In fact, inflation can often be quite useful as it erodes the value of debts (which is why creditors and asset holders hate it so much). So long as wages keep up with the rising prices then for those who don’t depend on the rising value of assets or debts it can be manageable. So how are we doing on that point?

So inflation is rising and wages are declining, so we’re in the situation where meeting our needs and maintain a decent standard of living is becoming more and more difficult. But even this could be mitigated or reversed if the government were to step in and support the economy by investing or by otherwise injecting money into it.

And so this is the root of the coming crisis. Prices are rising, wages are stagnating, savings have been drained, credit cards have been maxed out, and the government is pulling out of the business of providing government and public services so you need to spend even more to replace it. We no longer have enough money to meet our basic needs, never mind the disposable income to buy the widgets we need to consume to keep the wheels of the economy turning.

Up here in Scotland, there are signs that the crisis is already upon us. The Fraser of Allander Institute published a report today warning about the precarious nature of the Scottish economy saying that it was stagnating with relation to the UK economy as a whole. Some will almost certainly be quick to blame this on the Scottish government (the phrase “uncertainty of a divisive second independence referendum” comes to mind). There are certainly some things that the Scottish Government could do to help – a National Investment Bank should be high on the list and a good shake up of the domestic agenda would be welcome – but the ultimate cause of this slow-down does not originate in Scotland nor will its solution come from here (at least until the levers of power are returned to the country upon independence).

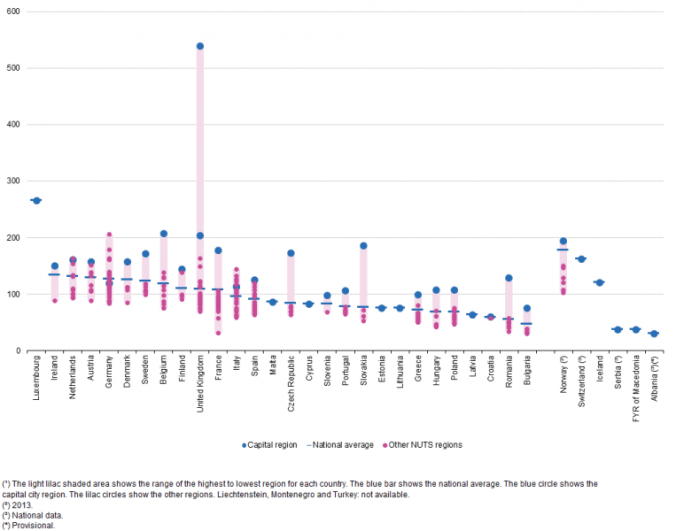

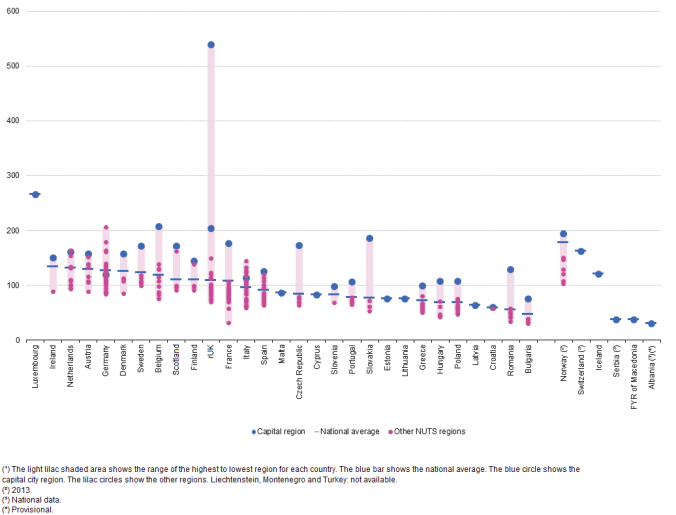

The problem, ultimately, is that Britain isn’t Great. Britain is Weird. Britain is a deeply unequal country on a scale which, compared to its neighbours, is utterly baffling.

In many countries, the capital city will be the richest region of the nation. This is normal – Money wants to be close to power – but the UK’s disparity really needs to be seen to be believed. Here is the GDP/capita for each of the EU28 and EFTA countries broken down by region. Spot the odd one out.

(Note that the UK has two capital dots. The lower one is London as a whole. The upper one is just Inner London)

Whenever statistics about Scotland are produced, they’re often given with reference to the “UK average” or the “UK as a whole” but the extreme disparity of Britain masks the picture. Detailed analysis by Prof Mike Danson of Heriott-Watt University has shown that Scotland’s GDP per capita is the third highest region of the UK (after London and the South-East) and, if we were an independent state, we’d be the 9th highest in Europe. In fact, we can disaggregate out the Scottish data from the chart above and catch a glimpse what we’d look like as an independent country.

Taken on this view, Scotland no longer looks like a “below average” region of the UK but a fairly normal Western European country. Far more like Finland or Denmark than, say, Greece.

As Prof Danson says, the obsession with comparing Scotland to misleading “UK average” figures leads to commentators ending up unable to take a step back and ask what is happening across and within the UK and where the problems really are. Until this happens, Scotland will continue to stagnate within the UK as the overinvestment of London continues (and is likely to get worse through the Brexit process in a desperate attempt to prop up the financial sector there).

As said earlier, there is a way out of the coming credit crisis but it’s going to involve not more Austerity but a whole lot less. Economists are increasingly coming around to the realisation that the Government’s debt is your surplus and that governments can take on that debt almost without limit (unlike you who have hard limits on credit and the ability to repay it) and – if they have their own currency – can print money in order to provide services (unlike, again, you who would go to jail if you tried that).

Once again, there is a certain amount that the Scottish government can – and should – do at the moment to help but it will always be stymied by the very tight rules of devolution. There’s little to no hope of the UK changing course any time soon (even Corbyn’s Labour is solidly committed to “balancing the budget“) and the hard Brexit the Tories and Labour are both pursuing is being increasingly differentiated by the amount of damage the plans will cause rather than any attempt to prevent it. The Sick Man of Europe seems destined to return to the UK. I only hope that Scotland doesn’t catch its cold.

“We bailed out the City 10 years ago when the crash came, we poured hundreds of billions of pounds into it. Since then £100bn has been given out in bonuses in the City. So we are asking for a small contribution…to fund our public services.” – John McDonnell MP

Last night, Labour announced one of their keynote policies ahead of the 2017 General Election. A financial transaction tax on the City of London. Time for a blog to outline just what in the name of Jim it actually is and what it’s supposed to do.

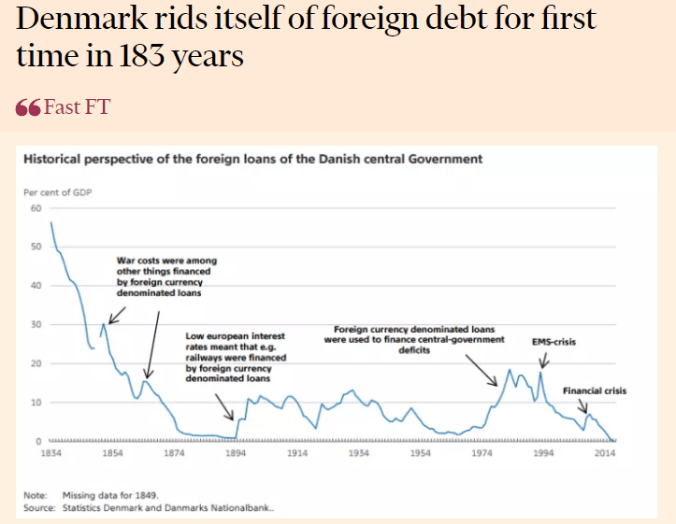

There’s an interesting wee story doing the rounds that moment regarding Denmark and their foreign debt.

I’ve seen a few folk get a bit over excited about the story and have misinterpreted it as saying that Denmark is now debt free. First up, it’s not. Their national debt is at about 38% of GDP (compared to the UK’s 85.4%). This isn’t about the Danes paying off all of their national debt, it’s just saying that they no longer have any debt which is denominated in foreign currencies. All of the Danish national debt is, for the moment, denominated in Danish krone.

There’s a more interesting story under here about why it has happened though. It’s the story of managing one’s currency and maintaining a currency peg with regard to another. This is something that folk in Scotland should be watching closely as our own debate about currencies heats up again.

Not long ago I wrote an article on defending one’s currency against speculative attacks but many of the lessons also apply to more gradual changes in currency value and the effects are being borne out in Denmark as we speak.

Recently the instability in the Eurozone and reduction in confidence in the euro has seen investors selling euros and buying krone, seeing it as a safer investment. This is pushing up the value of krone which, if it was freely floating, would affect the exchange rate between it and the euro. But Denmark seeks to maintain a stable exchange rate between the krone and the euro (At a rate of 7.46038 DKK/EUR ± 2.25%) so its central bank must intervene to prevent the rise in value. It does this by cutting interest rates (to make further purchases less attractive) and selling DKK and buying foreign currencies. This influx of foreign currency has allowed it to pay off foreign denominated debt but has also caused its foreign reserve holdings to boom from 200,000 million krone in 2008 to over 400,000 million krone today.

If the opposite case had been true, if the DKK was weakening with respect to the EUR, we might expect the levers to be pulled in the opposite direction. Interests rates would increase to attract investment and foreign reserves would be drawn down as foreign currencies were sold to buy up krone holdings and support the value of the currencies and we might see the central bank issue bonds marked in foreign currencies rather than paying them off.

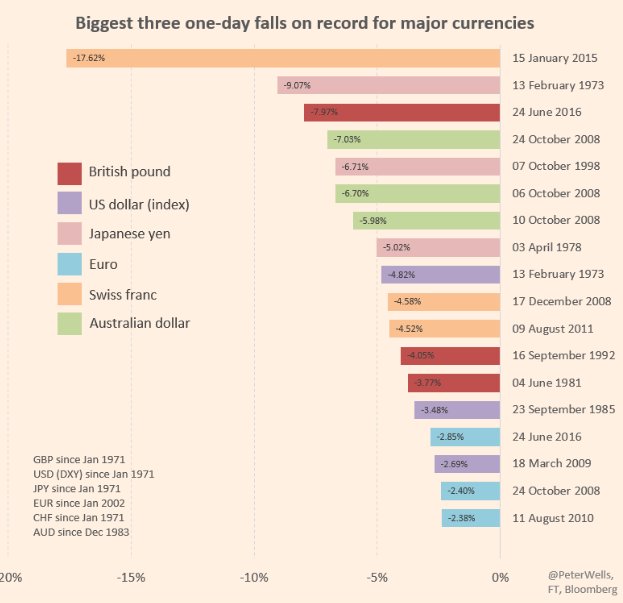

It may well be that Denmark can continue do defend its currency peg for some time, although some have eyed the possibility of a break similar to the one Switzerland went through in January 2015. A couple of years on from the Swiss break the risk of Denmark following suit appears to have receded for the moment.

All in Denmark – currently the 2nd happiest county on Earth – is showing what happens when a small country of 5-and-a-bit million people, its own currency and the will to manage it can do and whether or not Scotland specifically chooses a path similar to this (by pegging a £Scot to the GBP or, indeed, the EUR), Denmark should be taken as an example of what can be done. A small island of light and clarity in a world where the people of Scotland are about to be told repeatedly and in detail what some folk think we can’t do.

“Whenever politicians and rulers, from Nero onwards, interfere with monetary arrangements for political ends, disaster follow.” – John Chown, A History of Monetary Unions.

Currency remains one of the great potential uncertainties surrounding the debates about Scottish economics and independence. Last year I published the various options facing an independent Scotland along with the merits and demerits of each. Having selected as the preferred option an independent £Scot initially pegged to the Pound Sterling, Common Weal subsequently published a detailed plan on how precisely to go about making this currency a reality. Rather pleasingly, the news this week coming from the Scottish Government’s Growth Commission hints that they are looking at things from very much the same point of view as we have and may well be coming to the same conclusion.

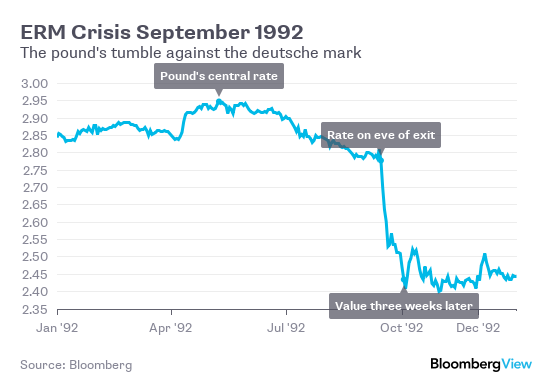

The main lesson of discussion about currency options is that all of them have their disadvantages along with their advantages and one of the primary disadvantages of this option lies in the peg to Sterling, particularly if it is to be maintained beyond the transition and launch period of the new currency. There could be the potential for the international speculative market to mount an attack on the currency in order to knock it out of the peg (as infamously happened to the Sterling in 1992 when it was knocked out of the European Exchange Rate Mechanism). A discussion of the likelihood of this happening and how one can defend against it is therefore required.

As with many things of this nature, the detailedstudyof thiskindof thing can run rather to the technical (the links there are made available for those who wish to study them) so I’ll attempt to break it down into something a little more accessible.

What Makes a Currency Vulnerable To Attack?

The entire purpose of a currency market is to allow that market to determine the most efficient price of the currency. This is generally only considered an attack when the currency is pegged to another. When the currency floats, a market driven price movement is considered the entire point of the exercise. This is part of the reason why “Black Wednesday” came close to bringing down the UK government whereas the 2016 Brexit devaluation was much less politically damaging despite being a larger depreciation in percentage terms.

So why attack a currency in the first place? There are multiple reasons but they essentially boil down to one. The peg is perceived as being “wrong” for the currency and the economy it supports. Either it is over or under valued. Usually it is the former as politicians tend to link a “strong” currency to national pride cases of undervaluation such as in China or Germany do exist (It should be noted that neither of these economies are under serious speculative attack at present).

Assuming an overvalued currency, the attack generally takes place by speculators “short selling”, or “shorting” the currency on the markets. To do this, they will borrow a great deal of the currency at the overvalued rate and sell it on the foreign exchange markets. This floods the markets with supply of the currency and depresses the price. The speculator can then buy back the currency he sold at the new lower price, pay off the loan and pocket the difference.

Before an attack happens though the speculators need to be sure of one of two things. Either A) The country under attack lacks the will to defend the currency peg or B) It lacks the tools to successfully defend against it. If the attack fails, then the speculators could be out of pocket to a very significant degree. Whilst George Soros infamously made off with £1bn in 1992, there are reports that he had to borrow some £6.5bn to do it. He was sure of his bet and it certainly paid off for him that time, but that’s still a big gamble to take and lose.

How to Defend a Currency

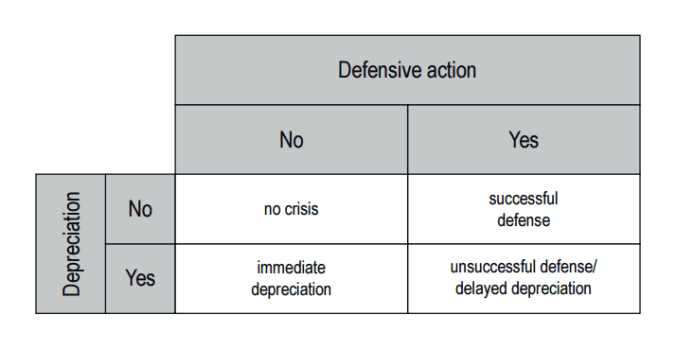

An attack can be defended in one of two ways (or a combination of both). First, the Central Bank can raise interest rates to discourage further borrowing of the currency (if interest payments on the loans exceed the expected gain, speculators will back off) and to encourage investors to start buying currency at the same rate as it’s being sold (so they can benefit from the increased returns on the interest). Or Secondly, the Central Bank can sell foreign reserves and buy their currency back themselves to limit supply and force the value back up. If they do this until the attackers themselves run out of the ability to borrow more of the target currency then the attackers give up and take the losses. (For an undervalued currency, the tools are used in the opposite direction as China is currently doing)

The third option is to consider both the economic and political situation and decide that if the currency really is mis-valued and that the political cost of unsuccessfully (or perhaps even successfully) defending the currency is too high then the defence simply isn’t viable. In this case the peg is dropped and the currency is intentionally allowed to revalue.

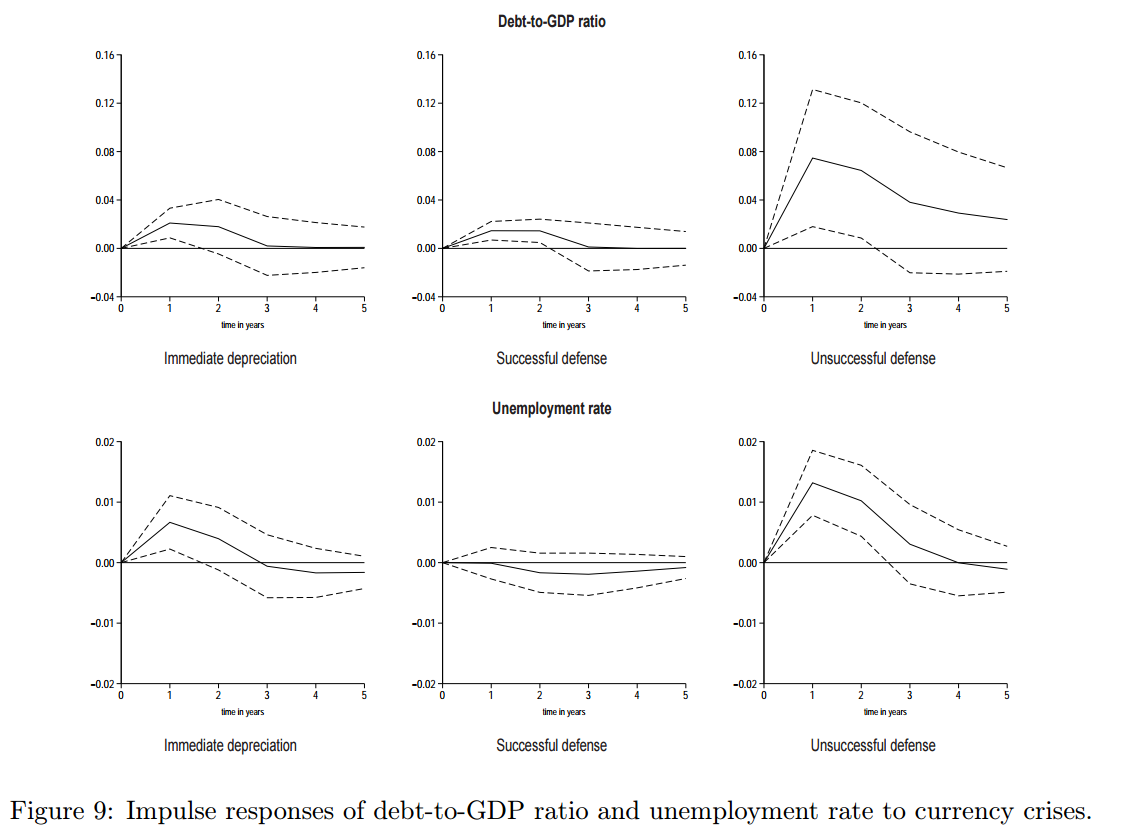

Herein lies the risk for Central Banks. The cost – which can take the form of higher interest rates, higher inflation, depleted national reserves, lower GDP and higher unemployment – of unsuccessfully defending the currency may be much higher than not defending it at all but not defending may carry a higher cost than a successful defence.

It is important to note that the failures to defend a currency are often higher profile than the successes which, by their nature, do not generate so many tabloid headlines or history books. At least one study has noted that of the 163 speculative attacks identified between 1960-2011, 42 were not defended against, 34 were defended unsuccessfully and 87 were successfully warded off.

To look at the 1992 Black Wednesday example caused when the GBP dropped out of the Exchange Rate Mechanism. The ERM (which was the precursor to the Euro) essentially pegged member currencies to the German Deutsche Mark. The value at which the GBP was pegged on entering – 2.9 DMK/GBP – was considered far too high and opened the road to the infamous speculative attack. The Bank of England responded by raising interest rates from 10% to 15% on the day of the attack and they sold £4bn worth of reserves (almost £8bn in 2017 pounds and about 1/3rd of what they had in reserve at the time). This turned out to be insufficient and the peg was eventually abandoned. The exchange rate fell to 2.413 DMK/GBP and the GBP fell out of the ERM. Papers released from within the BoE in the years since have mulled over the impacts and costs of their defence strategy, the causes of its failure and whether or not it was worth mounting in the first place.

Is Scotland Vulnerable?

So would this apply to Scotland in the event of our independence? There’s never a certainty with these things and the state of the international money markets are that size of one’s economy is probably no sure defence against all possible attacks (short of erecting massive capital controls and isolating Scotland from the global trade market, but this too carries its own consequences). However, I do believe that Scotland would be less vulnerable to a speculative attack than some may suppose for the following reasons.

First (and possibly most importantly): If we peg to Sterling then it’ll be on a 1:1 basis therefore will be at the same value that it is currently. To believe that the £Scot is over or under valued is to believe that the GBP is currently, right now, unsuitable for the Scottish economy which begs the question of why we’re even in a currency union with rUK. This may change post-independence as our economies diverge but in that case the question of whether or not to continue that 1:1 peg opens up. I personally think we’ll either float the £Scot or move to some kind of basket peg shortly after the three year transition and launch period but this is ultimately a political decision as well as an economic one and it may be that the option to move away from the Sterling peg is one debated and decided by the second independent Scottish Parliamentary elections. If a party wishes to hold to the Sterling peg (or any other) then it’ll be for them to determine if that’s a viable option and to convince voters of the same.

Second: We’re proposing to hold rather substantially more foreign reserves than the UK holds as a proportion of GDP. We’re looking initially at somewhere between £15bn-£40bn (Common Weal is currently working on a formal paper looking at how precisely we’d generate these reserves though I have spoken about it somewhat here) with options to use the normal tools available to normal, independent countries to adjust this amount as required. Combined with the lower available trading volume of being a smaller currency (one can only even potentially borrow as many £Scots as exist, especially if it is issued solely by the Central Bank) then this should be sufficient to hold off an attack or even just to display that we’d be willing to do so. Combined with tighter regulation and legislation on the financial industry Scotland should present itself to the world as a country upheld by its strong and reliable approach to fiscal and monetary policy.

Third: Interest rates are at an all time low which gives a fair bit more scope to raise them in the event of an attack than was the case in 1992. One has to be a bit cautious with this though as our private debt levels (particularly mortgages) are leveraged to the hilt so there will be severe consequences if this lever is pulled too hard. This said, the low interest rates are also crippling savers, investors and pension holders. They could well benefit from a raised rate such that an “attack” by the market may well come to be seen as a signal to change political and economic policy rather than a simple profiteering exercise by the speculators. As with life, balance in all things is best.

Conclusion

In short, Scotland is probably less likely than feared to suffer a speculative attack on the currency in the short term following independence and more than able to defend against more should it happen, particularly if we keep the heid and approach the separation rationally and in a well planned manner. Beyond this, it shall be a matter of analysing both the economics and the politics of the situation and never becoming too attached to any particular choice so that if a successful defence of the currency can be mounted, it should, if not, it shouldn’t and if a peg should be modified, changed or abandoned then it must.

“Work as if you live in the early days of a better nation.” – Alasdair Gray

Today I get to announce the launch of a very long awaited project I and the rest of Common Weal have been working on for quite some time now. We announced back in September that we have been working on renewing the case for Scottish independence by publishing a successor to the Scottish Government’s “Scotland’s Future” document.

Version 1.0 of the Common Weal White Paper can be download here or by clicking the image above.

This is a leaner document than Scotland’s Future was. That document was as much a party political campaign device as it was a blueprint for independence. It not only sought to describe the powers which would come to Scotland independence but also sought to convince voters of the SNP’s own vision for independence. There was nothing inherently wrong with this latter task per se and other parties too sought to promote their own distinct visions as well – as they will all do so again throughout the next independence campaign but this is not the task of an independence White Paper. This paper shall, as far as possible, not seek to propose a list of policy ideas which an independent Scotland could do nor shall it attempt to convince you of the merits of those policies. It merely lays out the technical and structural requirements which must be in place for Scotland to become an independent country once we, the voters, decide that it should become so.

It is a “consolidated business plan for the establishment of a new nation state”.

To this end, the White Paper is split into several broad sections. Part 1, Process and Structures, covers the foundation of a National Commission – a cross party and cross administration body which will be tasked with designing and implementing the institutions and systems which need to be set up in the time between the independence referendum and the formal independence day. It is one thing to state, for instance, “There shall be a Scottish Central Bank”. It is quite another to decide how large it needs to be, where it needs to be based and who needs to be hired to run it. The National Commission shall also be given interim borrowing powers so that it is able to issue bonds, raise capital and fund the construction of the vital infrastructure Scotland would need to either move from rUK or build from fresh.

Part 2, Key Institutions of an Independent Scotland, covers all those things we kept being asked questions about during the last referendum. Would we have a constitution? A currency? What would we do about borders? Defence? All these and more. Of course it’s not yet possible to answer every question in this regard. Some of it will be up for negotiation with rUK, some of it will be dependent on the shape of the Brexit deal between the UK and the EU and Scotland’s relationship with both in the run up to independence but we’re making a stab at as much as we can and this is the section which will perhaps be most expanded upon as the Project is iterated in future versions.

Speaking of negotiations, Part 3 covers the prospective shape of some of these – chiefly the allocation of debt and assets and what rUK’s response to our leaving shall mean for our claim on them. Also covered to some degree is how Scotland will interact with various international and supranational organisations although it should be stated once again that no case shall be strongly made for Scotland’s joining or refusal to join any of these organisations. That shall be left to the party or parties which seek to form the first independent Scottish parliament.

Finally, Part 4 outlines the position of Scotland as far as finance and borrowing goes as well as outlining as best we can the default fiscal budget for year one of independence. It is, of course, almost impossible to place any kind of actual certainty or promise on such a budget as it is based on several key assumptions such as the desire to keep both public spending and the various tax revenue streams broadly similar to their position at present. If a party decided to scrap the entire tax system and replace it with one of their own devising then it would have to be up to them to explain how that worked and project the revenue to be gained from it and how it would be spent. Other assumptions include Scotland spending the money assigned to it in GERS for various “UK projects” on projects of similar value and in similar accounting lines (so that, to pick an arbitrary example, our “share” of UK economic development funding spent outside Scotland but from which Scotland “benefits” would instead be spent on economic development within Scotland). Again, whether or not this happens will be a case for the individual parties to make and will depend entirely on accurately and precisely how the current fiscal projections for a devolved Scotland within the UK map onto the fiscal situation of an independent Scotland.

Once again, this is not the completion of the White Paper. This is the beginning. You will see that there are several sections which need to be expanded and built upon and items like costs and figures will be updated as time goes on (the default budget, for instance, is based on 2015-16 figures but – as we’ve probably noticed by now – Scotland didn’t become independent in 2015-16 so these precise figures will be revised as and when they should be). Some areas require the attention of people with specific experience and expertise in them to be able to complete so we are openly calling for those experts who are able and willing to contribute. Please contact us if you want to be involved. Let’s work to build the early days of our better nation.

Actually it seems like only March that the last edition was out. What’s happening here?

Well, there was a consultation that almost no-one knew about which discussed a few methodological changes to GERS in line with the ‘new powers’ we’re getting and it also asked if the next report should be brought forward. I’m completely convinced that the fact that this means that we’re getting the report well before the Council election campaign next year is absolutely just a convenient side effect(!)…but no matter. We’ve got the data.

Tomorrow’s Headline Today

Scotland’s budget deficit remains at a little under £15 billion. As with last year, don’t expect a single news outlet to go one single step further with the story than that. Except maybe to say that oil revenue has dropped from £1.802 billion last year to just £60 million this year.

So what’s happened? Why hasn’t Scotland, which is “totally dependent on oil”, completely collapsed now that oil revenues have basically dropped to zero?

Last year, total revenues dropped by around £500 million on 2013-14. This year, total revenues have INCREASED by £181 million. In fact, total revenue is higher than it was in 2012-13 when we received some £5.3 billion in oil revenue.

It’s also worth noting that if you only look at GERS 2015-16 then it looks like our deficit has increased by a couple of hundred million in the past year but if you look a bit deeper, and compare the numbers to previous GERS reports then something interesting happens.

In GERS 2014-15 our deficit was recorded as £14.8 billion but in GERS 2015-16 the 2014-15 deficit has somehow dropped by £622 million to £14.3 billion. Essentially, this shows one of the limits of GERS in that it is based on sometimes highly speculative estimates which get revised over time. It may be five years before we finally know the “true” accounts figures for this year. This accounting adjustment is extremely significant compared to, say, our “budget underspends” but unless you’ve read it here I expect it to pass entirely unnoticed.

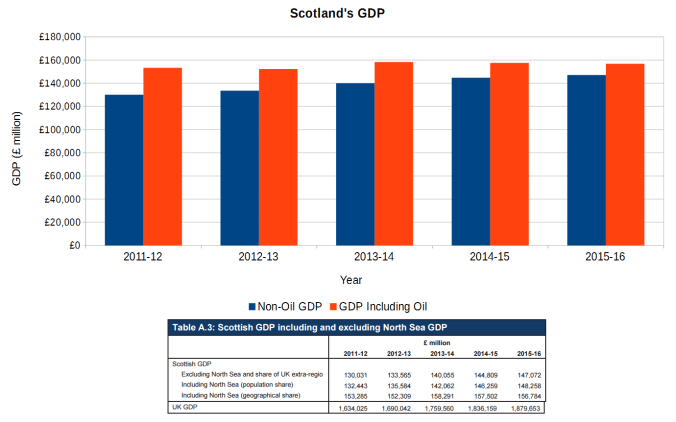

Now, what about our all hallowed GDP? It’s down by 0.45% from £157.502 billion in 2014-15 to £156.784 billion in 2015-16 (with non-oil GDP having increased by over £2.2 billion, the highest it’s ever been).

You know, perhaps it’s time we started measuring our economy in terms other than just GDP. We know it’s flawed. We know it throws up extremely strange results like Ireland’s “economy” growing by 25% because a few American companies moved their nameplates around. We know it doesn’t even particularly correlate to things like tax and ability to service debt very well.

Maybe it’s time we started measuring (and taxing) our country based on the things which actually matter.

But back to GERS.

Dutch Disease with Scottish Characteristics

So what’s going on here? Essentially it’s the same pattern first picked up last year. As oil prices drop, so do fuel costs. Which means everything from the costs of transporting goods to the heating and lighting costs for your home drops. This means you have more money to spend in the economy and companies have fewer overheads leading to either greater profits (thus, ideally, more tax revenue) or more room to invest in expansion.

This is a clear demonstration of the so-called “Dutch Disease” where high oil prices choke off the non-oil based economy in the form of the aforementioned fuel costs (it also tends to harden one’s currency but this is less of a factor in the Scottish case given that we don’t yet have one).

At the time of the last report I was criticised for pointing this out on the grounds that the oil price collapse “hadn’t fully fed through” hence I was jumping the gun on the observation. It shall be interesting to see if anyone says the same thing now. Could revenues drop any lower?

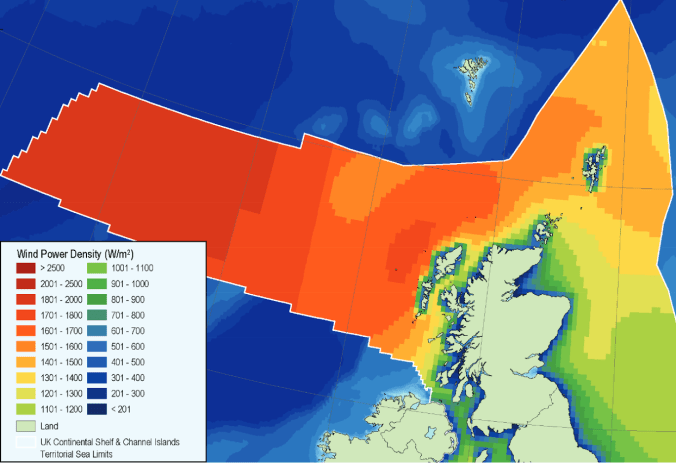

This should serve as somewhat of a warning to those itching for the return of high oil prices and certainly for those desperate to “replace” offshore oil with onshore fracking. It’s maybe time to have a good hard rethink about what kind of resources we want to develop in Scotland. Now, to be sure, I’ve nothing against our offshore industry and for those folk out there it’s been a pretty dreadful time. It’s just that, certainly as a Green, I think our offshore industry is on the wrong side of the country and should be based on wind/wave and tide rather than oil. You can be sure that if the wind and tide stops flowing we’ll be dealing with problems a little bit larger than the state of our finances.

Scotland’s offshore Wind Power Density map

Sweet Fiscal Autonomy

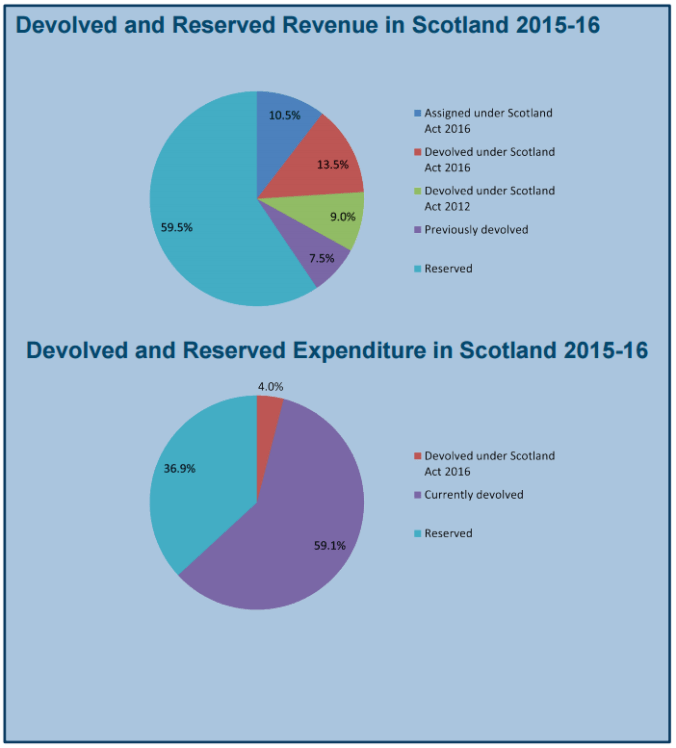

As mentioned earlier, part of the methodological changes discussed in the GERS consultation was to do with looking at the taxes to be devolved to Scotland under the series of “vast, new powers” we’ve been generously granted.

In terms of actual revenue, chief amongst these is income tax (excluding interest and dividends, the ability to move the Personal Allowance or to adjust the definition of “income”) and VAT (excluding any actual control at all. We’re getting the VAT added to Scottish coffers and then an equivalent amount removed from the block grant. Yay.) along with comparatively minor taxes like landfill tax, aggregate levy and air passenger duty.

In total, the Scottish government will directly receive 40.5% of Scottish revenue (£21.8 billion this year) and, given the limitations on VAT and income tax, have actual, practical control over perhaps half of that. Devolved expenditure, however, will soon sit at 63.1% of total (£43.3 billion). Basically the Scottish government can only directly control enough income to fund perhaps about a quarter of what it’s directly responsible for delivering.

There’s a side issue in all of this related to that old topic of the budget underspends. Tucked away on page 47 of GERS there’s an interesting line which looks at the confidence intervals for some of the tax revenues used. Remember that the revenues given are estimates and are subject both to revision over time and change due to circumstances that the government cannot control. For example, if you move job half way through the tax year your income, therefore income tax, can change. If your job moves you to England, your entire income tax contribution moves from the Scotland side of the budget to the rUK one. Hence, the total income tax revenue estimate is subject to a margin of error, in this case of 1.0%.

The same goes for other taxes to greater or lesser degree to the effect that the margin of error over all of the taxes measured there is 1.6% or ±£570 million.

Remember that the Scottish Government has extremely limited borrowing powers. It can only “overspend” on the current budget by £200 million in a single year and cannot exceed a total current debt of £500 million. And yet income revenue, on which expenditure must be planned, has a margin of error of ±£570 million.

In the event, this year Scotland’s “underspend” was only £150 million. If you think you can plan a budget better than this then please, send it in. If not, might be a good idea to stop reporting and moaning about underspends.

Paying For It

Another little line that seems to have been added to GERS this year (on page 37) is a breakdown of the annual costs of financing Labour’s PFI and the SNP’s replacement NPD loans. There’s been a bit of a milestone reached there with the availability costs of PFI now exceeding £1 billion per year or over 15% of Scotland’s total capital budget and slated to increase even further over the next decade unless something is done about it. Don’t be surprised if this becomes a major issue for the council elections next year.

Of course and once again you wouldn’t know this if all you did was watch our Great British Broadcaster, the BBC. Their recent “investigation” into PFI couldn’t even bring itself to mention the name of the party which lumped this crippling financial burden on us.

Finally

I could go on. We could nip-pick at details like the mysterious addition to the expenditure budget of net EU contributions (there’s always been an annex discussing this but this is first year it has explicitly been counted in a separate line in Total Expenditure) or notice that for the first time in at least five years our debt interest paid has increased as our UK debt increases have started to outweigh the effect of falling bond yields.

It’s all a shell game though. We know that GERS isn’t nearly as important as people hold it to be nor is it nearly as informative as it should be. It’s not going to change many minds on its own nor does it tell us one single thing about the finances of an independent Scotland. If we want to do that, we’re going to need to build a national budget from scratch, taking into account all of the taxes (existing and new) that an independent Scotland might choose to levy. We also need to have a look again at what Scotland actually needs to spend its money on. Could we use Citizen’s Income to create from scratch a welfare system worthy of the name? Would a Scottish Government able to issue its own bonds on its own debt be able to get a better deal than the one we have right now?

Quite simply can Scotland as a nation see ourselves as better than others would prefer us to be seen?

As promised, I can finally reveal my work examining Scotland’s currency options going forward into the next independence campaign.

My report has been published through Common Weal and can be read here or by clicking the image below.

In it I first examine the macroeconomic considerations which go into selecting a currency option, chiefly looking at the interaction between movement of capital, interest rates and exchange rates. It turns out that it is impossible to have full control over all three at any one time so all currency options entail therefore some degree of risk or management requirements including the founding of infrastructure such as a Central Bank. All options have their advantages and disadvantages, their risks and rewards.

{kind=link}