Qualifier: The following article shall cite political views which represent, to the best of my understanding, the positions of the Official Remain and Leave campaigns. As such they may not necessarily represent the views held by myself or by any organisations or political parties of which I am a member. My own views shall be indicated throughout.

Likely to be one of the “softer” issues in this debate as unlike immigration and unlike the economy it’s one that doesn’t render down so easily into simply numbers. This doesn’t mean it’s any less important. How we feel about the concept of “Europe” plays a very large part both in what we will want out of that relationship, what we will want Europe to become and what we want ourselves to become either within or outwith the Union. It also tells us a lot about how we see our relationship with our governments which means that the result on Thursday may well have deeper ramifications on how the United Kingdom itself is governed. Sovereignty, who controls the locus of power and where it resides, is a policy on which your position may well lie in how you define it.

This is just a quick side note to my Are EU In or Out? series as a response to Vote Leave‘s recently published Leaving Framework, their plans for what comes after a Leave vote. If you will, it’s their White Paper moment. You can read it here (or here).

Qualifier: The following article shall cite political views which represent, to the best of my understanding, the positions of the Official Remain and Leave campaigns. As such they may not necessarily represent the views held by myself or by any organisations or political parties of which I am a member. My own views shall be indicated throughout.

Are EU In or Out? – Part 1: What is The EU? can be read here

Are EU In or Out? – Part 2: A Brief History of Brexit can be read here

Are EU In or Out? – Part 3: The Issues – Immigration can be read here

Are EU In or Out? – Part 4: The Issues – Trade, Economy and Finance can be read here

Brexit Negotiations

One of the more contentious moments of the 2014 Scottish Independence campaign came about within the discussions over “what comes next?”. The post-vote negotiations over the unstitching of Scotland from the rest of the UK would have represented challenge at least on par with the separation of Ireland or the decolonisation process, if not greater. This may not have been helped by the fact that the British Union does not contain a formal legal mechanism for constituent member nations to leave, the Edinburgh Agreement and all that came after was essentially invented ad hoc. In contrast, the European Union does have a formal leaving mechanism in the form of Article 50 of the Treaty of the European Union, albeit that this mechanism has not been put into practice and was drafted only after the experience of Greenland’s process of leaving the European Communities in 1985. As this paper points out though, the comparison between Greenland and any UK leaving process is unlikely to be more than superficially similar as Greenland’s economic and political interaction with the EC at the time revolved very substantially around their fishing industry whereas the UK is far more economically and politically integrated.

The polls are tight. Neck-and-neck, even. Far too close to call and we’re only a couple of weeks away now. I think we owe it to ourselves to consider the possibility of a Brexit vote and to ask just what the Official Leave campaign wants to get out of their desired result, whether or not it’d be easy – or even possible – to achieve and if it actually chimes with the desires of many of their voters.

Qualifier: The following article shall cite political views which represent, to the best of my understanding, the positions of the Official Remain and Leave campaigns. As such they may not necessarily represent the views held by myself or by any organisations or political parties of which I am a member. My own views shall be indicated throughout.

Are EU In or Out? – Part 1: What is The EU? can be read here

Are EU In or Out? – Part 2: A Brief History of Brexit can be read here

Are EU In or Out? – Part 3: The Issues – Immigration can be read here

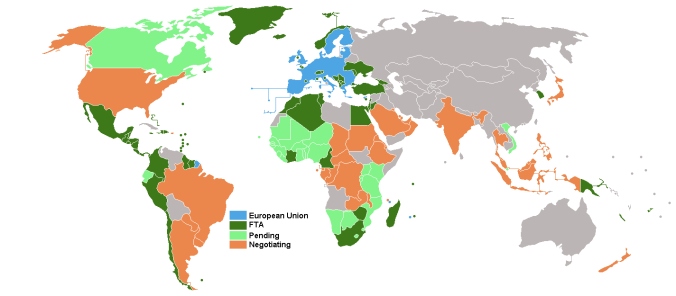

Active, Pending and Proposed Free Trade Agreements involving the EU

Trade, Economy and Finance

If immigration has been the big push card for Leave then the Economy has been the same for the official Remain campaign. Once again, as in the 2014 Scottish Independence Campaign, nothing says “Project Fear” like that Great Leap into the Unknown that comes with trying to predict the state of the economy after a shock event like Brexit (Little tip. In this era of rampant financial speculation, if anyone could actuallypredict the economy, there wouldn’t be one because that person would now have ALL the money). Similarly, Leave, whilst fighting a much weaker campaign in this respect, are promoting the fear of overburdening and uncontrollable regulation which is holding the UK back from its true potential. Of course, the parallels with the 2014 indyref abound on both sides. It certainly shall be interesting if and when a second indyref comes round and the words spoken by several prominent figureheads involved in this current campaign end up held against them (of course, this may well happen to unwary activists on our side too)

Qualifier: The following article shall cite political views which represent, to the best of my understanding, the positions of the Official Remain and Leave campaigns. As such they may not necessarily represent the views held by myself or by any organisations or political parties of which I am a member. My own views shall be indicated throughout.

Are EU In or Out? – Part 1: What is The EU? can be read here

Are EU In or Out? – Part 2: A Brief History of Brexit can be read here

The EU Referendum Issues

I’ll say again that I believe that the “Official” Remain and Leave campaigns in this referendum are almost as dreary and dire as the other. It’s rather depressing how we’re witnessing something as momentous as the potential future of Europe being used as leverage for something as petty as an internal debate about the future leader of the Conservative party. Worse than that though is the attitude towards the issues. It’s almost as if BOTH sides looked at “Project Fear” – the 2014 Scottish anti-independence campaign which, through unrelenting negativity and naesaying, managed to turn a 30 point lead into a 10 point lead and ravaged public trust in both their member political parties (Labour in particular) and in the media which reported for them – and took the very worst aspects of it into their hearts.

It’s been left to the “Unofficial” campaign to speak not only to and for the Scottish dimension (as typified by “The Wee BlEU Book” by Alyn Smith MEP and Ian Hudghton MEP and which I consider to be required reading before the vote) but also for Green and Left voters (as typified by groups such as Another Europe is Possible and DiEM25 which recently held an excellent conference on the Left case for Remain).

This series of articles began as a response to someone I know who was asking for as balanced a case as I could write on the debate. I find that I cannot, given the campaign and my place in it, give a strictly neutral view but I can do as follows. I shall take the primary issues as encountered in the media and shall attempt to lay out the “Official” position on that issue by Leave and Remain. I shall then add my own commentary on that issue. This may result in my agreeing with one or other of the “Official” campaigns or it may have me disagreeing with both and offering an alternative path.

The big hot-button issue of the debate. Immigration. The implications for the UK both in and out of the EU and the positions of the Official Remain and Leave campaigns as well as my own thoughts.

So what happens next if Leave wins? What are our options for future UK-EU relations and which of them come closest to what you want compared to what the Official Leave campaign wants?

A side note on Vote Leave’s Leaving Framework White Paper. In my opinion, it is seriously lacking in several factual areas and deserves widespread media scrutiny.

“It can be concluded that both shale oil and shale gas are unlikely to be economically viable in this current low hydrocarbon price environment and even if there is a return to recent higher prices; it is likely that the industry would require significant subsidy or significant efficiency progression before it could be used at any kind of scale.”

“Even if the extraction can be proven to be environmentally ‘safe’ the experience of the United States shows that it risks bringing boom-and-bust to our communities as waves of temporary jobs move rapidly through without rooting themselves in local economies.”

My first paper written for the Common Weal has been published today. The Economics of Shale Gas Extraction is the first major paper to be published in Scotland focusing on the economic, rather than environmental, impacts of the industry particularly on the local communities which will be hosting the wells.

Key Findings:-

The SGE market in the US and, so far, in the UK is dominated by larger companies occupying the most profitable licences. There is little scope for community owned or small company development to occupy a significant market share.

Individual wells become largely non-productive within a few years of development which, due to market demand for constant production, forces companies to continue drilling new wells in new locations at a rapid pace.

The low recoverable volumes and high capital and running costs of wells may render profit margins comparatively small and extremely sensitive to oil and gas pricing. There appears to be little scope for economic development of SGE in the UK until and unless wholesale prices return to historic highs and even then significant subsidy may be required.

Communities are likely to be significantly adversely impacted by nearby SGE fields. The concentrated pattern of land ownership and comparatively weak situation of local government renders communities vulnerable to being unable to capture wealth generated by nearby wells whereas the burden of environmental degradation or even simply the threat of such degradation can lead to community stress and negative economic effects.

The jobs created by SGE appear to be short-lived and highly mobile. The job demographic of the planning, drilling and production phases are each relatively exclusive meaning that they will move to the next site more rapidly than the wells themselves do. This creates the risk of a “Boom-Bust” effect in communities.

Shale oil and gas is considered a relatively poor source of fuel due to high extraction costs. The UK’s reserves are also likely to have an insignificant impact on global markets and hence a negligible impact on end-user prices.

Significant externalities have been identified in the form of environmental degradation due to methane leaks. The costs to mitigate these may exceed the lifetime revenues generated by the well which produced them. Further, the UK has a poor record in terms of ensuring adequate decommissioning and restoration bonds which may lead to further public funding being required after the SGE companies have left an area.

Whilst much of the attention on the shale oil/gas and fracking industry has been focused on the environmental impact, less attention has been paid to the economic effects. Even if the extraction can be proven to be environmentally “safe” the experience of the United States shows that it risks bringing boom-and-bust to our communities as waves of temporary jobs move rapidly through without rooting themselves in local economies. Scotland’s history of concentrated land ownership and comparatively poor local government also risks creating a vast transfer of wealth benefiting the already wealthy whilst potentially leaving communities to foot the bill for cleaning up. All for a fuel which the government has been told will not even benefit us in the form of lower energy bills.

There should be no place for fracking in Scotland or the UK.

“I would say is that every public-private partnership in Scotland has delivered new hospitals or new schools in Scotland on time and within budget and that’s the sort of success I want to see in every building.” – Jack McConnell, 2002

Oxgangs Primary School, 2016. Built by PFI in 2005

The dramatic news from Edinburgh in the past couple of weeks has put into sharp focus the failures of some of the finance models used by our regional councils to build schools, hospitals and other public buildings in recent years. Public/Private Partnerships (PPP), Private Finance Initiatives (PFI) and, less well known, Lender Option, Buyer Option (LOBO) Loans have burdened our councils with near-crippling financial obligations and, as we now know, have too often failed to deliver on even the basic standards of results required. Just what these deals are and why they have been used is a topic which requires a bit of discussion.

PPP/PFI

Public Private Partnerships, of which Private Finance Initiatives are a specific type, are a form of capital investment introduced to the UK in the early 1990’s by Major’s Conservative government as an alternative to tradition procurement methods of the time. In traditional public investment models a local authority might decide to build an asset such as a school itself in a purely publicly funded model or it might contract a private source to build the school and then take over the full running costs of the project afterwards. The Tories were driven by an ideological pledge to reduce the budget deficit (then known by the catchy title of “public sector borrowing requirement“) and identified the use of PFI as a means to do this.

Instead of paying for a project out of the capital budget either up-front or over the span of the construction phase, PFI would spread the costs over a medium or long term contract, often more than 20 years. This reduced the single year outlay and hence massaged the budget figures.

It was under the Labour government though that PFI really took off as it had the advantage of taking capital debts “off-book” and allowed Gordon Brown to simply stop counting them towards the deficit entirely. This gave the illusion of the fiscal prudence on which he banked much of his reputation. This was doubled down in Scotland by Jack McConnell’s Labour/Lib Dem government which led to Scotland, with 8.5% of the UK population, ending up with some 40% of the UK’s PFI funded schools.

The lie to the illusion can be found in the realisation that the private sector doesn’t work for free. These contracts almost certainly mean that the total cost to the council over the lifetime of the council is significantly larger than the up-front capital costs.

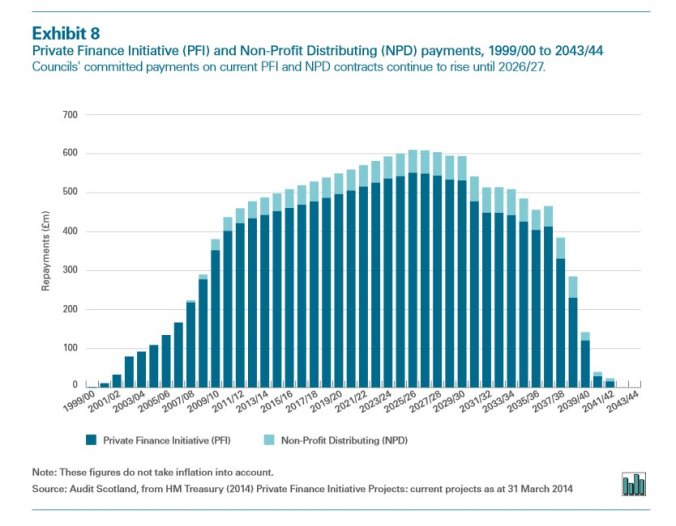

To take a recent example concerning some of the schools in Edinburgh, the private company involved will be paid £12 million per year for 30 years for a project valued at £68 million in up-front costs and an additional £84 million in management costs. Subtracting the running costs, this represents an annualised return on capital investment for the company of 10% per year. For contrast, David Cameron’s offshore tax haven shares “only” earned him about 6.75% per year.

And this doesn’t even represent the worst example of increased costs due to PFI. Contracts worth three or four times the capital investment are common. Some have been found to be worth a staggering ten or even twelve times the total outlay.

It is these ongoing payments which are particularly affecting our own regional councils and the problem is only going to get worse with the peak of the outgoing payments not expected to hit till the mid 2020’s.

Whilst one of the advantages of PPP’s often touted is the obligation for the private company to maintain the asset over the lifetime of the contract this can be a double-edged sword. One of the other “advantages”, mentioned in the UN ESCAP video above, is the “realisation of private sector efficiency savings”. That can mean “cutting-corners” to you and me. If the company is required to maintain a school for only 30 years but is then free from that obligation on year 31 then the inducement to build to the minimum possible standards to see out that contract is strong. Indeed, there is some anecdotal eyewitness evidence that exactly this has taken place. Schools which, by today’s standards are insufficient but which nonetheless stood for more than 100 years are being replaced with buildings designed to last less than a quarter of that and, has been seen, sometimes don’t even make it that far. This is not “long term planning”. It is certainly not helped by the generally low standards of our building regulations. A private company will rarely build at anything other than barely above the minimum legal standards so if we’re going to continue involving “the market” in our infrastructure projects then we’re going to need to have a discussion about increasing those standards to something more suitable for the 21st century. Whilst PFI specifically may have been abandoned in Scotland, this discussion over standards remains.

LOBO Loans

Lender Option, Buyer Option loans make up a far smaller proportion of council borrowing than PPP/PFI and have hit fewer headlines but they are still a symptom of the chronic dysfunction of our public borrowing system.

These loans were launched in 2000 as an alternative to the National Loans Fund which, whilst cheap and stable due to being funded by UK gilts, are sometimes quite limited in scope and therefore not always avaliable when required. Instead, the public body can approach a commercial bank for a long term, often more than 40 years, loan which is offered at an initially low “teaser rate” but which includes a clause which allows the lender to change the interest rate, usually upwards, are regular, often annual, intervals.

Sometimes these rate adjustments carry with them a contract exit clause but one can imagine the conversation in that case.

Bank: “So, we’re planning on increasing your interest rate from 2% to 5%. Under Section 4 of our contract, you can exit the loan by paying back the outstanding primary plus our exit fee.” Council: “If we had that kind of money, we wouldn’t have needed the loan.” Bank: “Ok. 5% it is. See you next year!”

These loans were often offered to and accepted by councils without the council quite appreciating the potential volatility and uncertainty that these changes would represent, which is quite understandable as these contracts have been criticised as being some of the most complex in the financial world and as our locally elected representatives aren’t necessarily chartered accountants it’s perhaps understandable that some would have simply been sucked in by those teaser rates which, at the time, undercut even those bonds offered by the NLF.

What Next?

I’m not going to pretend I have a magic solution to all of this. Some have discussed simply canceling and renationalising PFI funded assets but whilst I have some sympathy for this I have concerns also. Right now, we simply don’t know how far the record of substandard workmanship within the works built runs and, in fairness to the companies behind this disaster, they are upholding their obligation to pay the costs of repair and, if required, rebuild of these schools. If the contracts were canceled before we know the extend of the repair bill then we might simply be bailing out a huge debt. I can see some kind of scope for some kind of renegotiation over the annual payments or contract terms, perhaps with some kind of profit cap. Perhaps the companies could be offered an exit but made to put up a bond in case future issues arise although as we’ve seen from the coal and, more recently, the steel industry those bonds themselves need to be planned carefully lest they prove insufficient or evadable.

In future, a more sustainable method of public borrowing and investment needs to be examined. The Common Weal has a proposal to use a mutual limited company to leverage funds backed by Scottish issued bonds to invest in our public infrastructure which is perhaps one of the better ways to go about this issue although it is acknowledged that Scotland’s very limited borrowing powers even under the “new powers” of the Scotland Act 2015 will likely cap the viability of such a scheme. Obviously, an independent Scotland wouldn’t have that problem but until that’s sorted, we may need to think of something else.

Economics: The art of explaining why all of your models fail to predict either the future or the past.

Click image above for data

It’s that time of year again when everyone starts looking at the first page of a dense booklet of economic data and uses it to wildly forecast despite long known limitations in doing so. So it’s also, once again, time for me to try looking a little further to tease out some details that others might have missed.

First, to get some of the headline figures out of the way. There has been a slump in offshore oil revenue due, largely, to the crash in the oil price resulting from the ongoing economic conflict going on between Saudi Arabia and the US.

This has caused oil revenues to drop from £4.0bn in 2013-14 to £1.8bn in these current figures. And thus came sic a cry of a “>£2 billion BLACK HOLE” from certain sources…

…except…total current revenue is only down £600 million. Down from £54.050 billion last year to £53.443 billion this year. That’s just a touch over 1% of a change and is comparable to some of previous year’s “budget underspends“, thus it could even be said to be within the margin of error of budget estimates. So what is going on?

The European Court of Justice has released its judgment of the Scottish Government’s proposals to introduce a minimum unit price on alcohol.

Their judgment, published here, states that the proposals as written would be illegal on the grounds of being discriminatory towards cheap alcohol imports and thus would be a restriction on the free movement of goods within the EU.

They have, however, upheld the Scottish Governments arguments that MUP would lead to substantial health and social benefits and have agreed that it would, indeed, meet the goals of both reducing hazardous alcohol consumption and alcohol consumption in general (in an earlier article I noted that Scottish consumption of alcohol can be seen as substantially higher than the UK average simply by examining the tax records).

The court has therefore not banned MUP completely but has ruled that it cannot be implemented until and unless the national courts (i.e. Edinburgh and then the inevitable appeal to the Supreme Court in London) rule that the same alcohol reductions cannot be achieved via taxation. This sets out a test to be met by the Scottish Government.

But if that test is failed and taxation ruled appropriate, what form could it take?

The obvious first step would be alcohol duty but this is currently a reserved power and its devolution was ruled out of the Smith Agreement and the subsequent Scotland Act 2015 Bill. I would think it unlikely, given the current track record, that an amendment to devolve alcohol duty would succeed at this point so I think I’m safe in assuming that it will remain in Westminster hands. Nor, do I suspect, will George Osborne be keen to adjust his own plans for the UK simply to allow the Nationalists even a moment of victory so I can’t see him being amenable to changing alcohol duty at UK level either.

There is another way though, as pointed out by Andy Wightman on Twitter today, the Scottish Government currently DOES have the power to create new LOCAL taxes. If the courts ultimately agree with the ECJ that taxation would be just an effective method of reducing alcohol consumption as MUP then this would be a method within the competence of the Scottish Government to implement without further devolution or delay.

Such a tax need not be set locally, national legislation could fix the rate, though the advantages to doing so are quite strong. By keeping money within areas particularly blighted by alcoholism and alcohol abuse and by allowing the rates to be set to particularly target these areas the greatest good could be done the fastest. Conversely, those areas which perhaps see a lot of through traffic, people traveling into town for a responsible night out say, but suffer little actual harm from chronic abuse may wish to set rates somewhat lower so as to avoid driving away too much business.

While we’re looking at locally devolved alcohol sales taxes we could also take the advantage of the discussion to bring back proposals for alcohol production taxes too. Scotland is perhaps best known for its whisky exports but what is lesser known is the fact that many of the most famous distilleries actually employ comparatively few people and yet produce vast sums of money for their generally multinational corporate owners without doing all that much for a local area which often gives their very name to that drink. Given that these distilleries, and many brewers and other manufacturers, cannot easily move elsewhere (and certainly cannot move out of Scotland) then a local production tax seems particularly apt. Again, by setting it locally and by allowing local people a say in how it is set then they are in a position of power again and can directly benefit from our renowned exports.

Personally, I welcome the prospect of minimum unit pricing and do believe that it would be an effective aid to our national alcohol problem but my challenge to the government is that if the courts rule otherwise, there is still something we can do. Indeed, even if they don’t….why not both?

{kind=link}

{kind=link}

{kind=link}