The EU flag flying beside the French national flag over the Hôtel de Ville in Paris.

The referendum on the UK’s membership of the EU is fast approaching and, now that the Scottish parliamentary elections are out of the way, we are now shifting our focus upon it. I know that, especially amongst the activists, election fatigue is high but we really must not let this event pass us by.

For my own part, I am decided. I shall be voting to Remain within the EU and will be doing so out of rejection of both the official Remain and Leave campaigns. Whilst I have written about some of the issues important to me previously, it’s time to expand upon them whilst commenting on the issues important to both of the official campaigns. I shall attempt to outline these as objectively as I can whilst also laying out my own hopes and opinions on those issues.

In this article, I shall first outline the structures of the EU and some of what it actually does before moving on in a subsequent article to look at the issues being discussed in the referendum itself.

What is the EU and how does it work?

First, before the issues themselves, it’s best to understand just what the EU is, how it came about and what it does now. To help with this, the Green/EFA group in the European Parliament produced the following guide. Whilst some points are highlighted with the Green viewpoint on things, the document is largely objective and highly readable. I suggest that all voters who have any doubts or vagueries give it a good look through certainly before the vote and preferably before continuing here. Click the image or here to read.

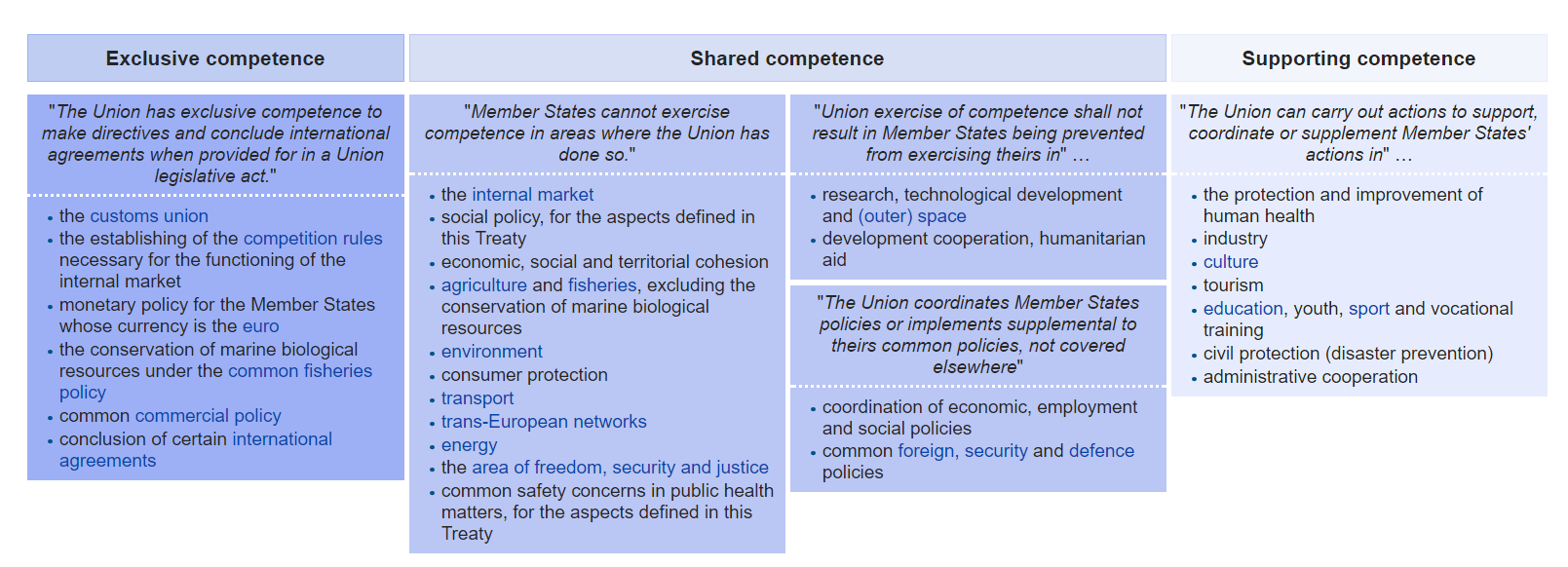

To attempt a brief(-ish) overview, the EU is an ongoing project which rose from the ruins of WWII initially as an attempt to arrange the politics of Europe such that war between the European nations, particularly between France and Germany, would never again be possible. This process began with the gradual interlinking of the French and German economies via the Coal and Steel Community in 1953 and gradually expanded into other economic areas and into the political sphere beginning with the 1957 Treaty of Rome (the preamble of which includes the first use of the now widespread adage and long term goal of the EU towards “ever closer union”) and the founding of the European Economic Community. In 1993, the Maastricht Treaty created the European Union and the single European currency, the euro, and laid out the powers it would have in areas both intergovernmental (i.e. by agreement of all members but without strictly superceding their national sovereignty) and supranational (i.e. powers directly administered by the Parliament). These became known as the “Three Pillars of the European Union”. This structure was then further amended by the 2009 Treaty of Lisbon which formally created the European Union as we know it today as a distinct legal personality and which laid out exactly where the EU takes exclusive competence preceding national member governments, where competence is shared and where the EU merely “supports” national governments achieve their own distinct policy.

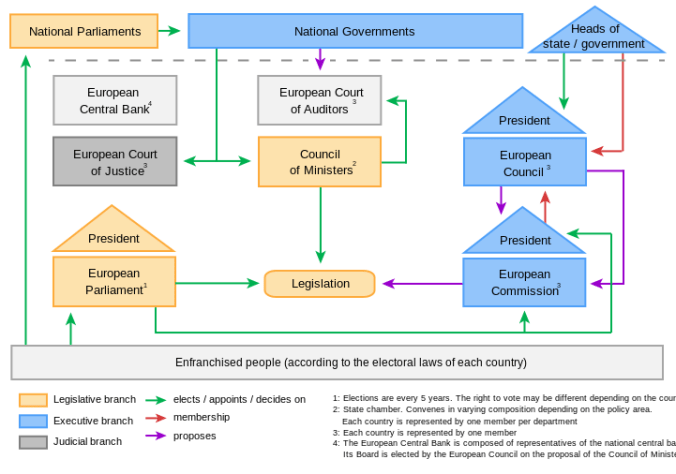

Today, the European Union consists of 28 national members which each take roles of varying degrees of embeddedness with the Union.

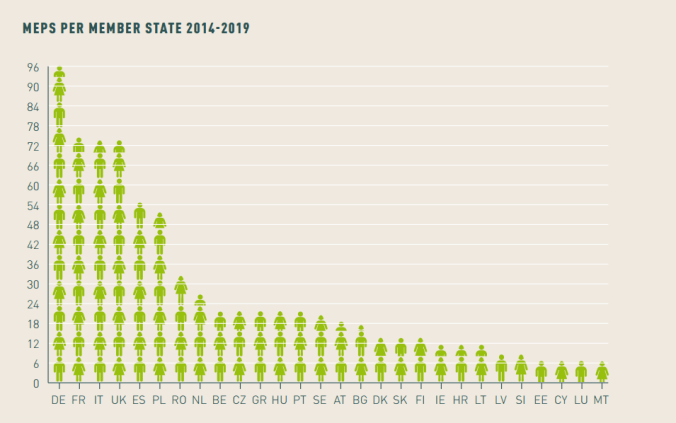

The Legislative Branch of the Union is primarily represented by the European Parliament and Council of Ministers. This Parliament, with 751 members, is the second largest democratically elected legislative body on the planet after the national Parliament of India (the UK’s House of Lords with 803 members and the Chinese National People’s Assembly with 2987 are the only two larger lawmaking bodies but these are not democratically elected) and is elected every five years (the last vote being in 2014) by a system known as “degressive proportionality”. Essentially, each member nation gets an allocation of not less than 6 MEPs and not more than 96 Members to the Parliament, roughly in line with their population as a fraction of the whole EU but arranged so that a few large nations (Especially, Germany, France, Italy and the UK) cannot dominate proceedings.

Within each member nation the MEPs are elected via the proportional d’Hondt system similar to that used in the Scottish parliamentary election regional ballot. which ensures that many more views from within a nation can be heard than would be the case under, say, the First Past the Post system used in the UK General Elections.

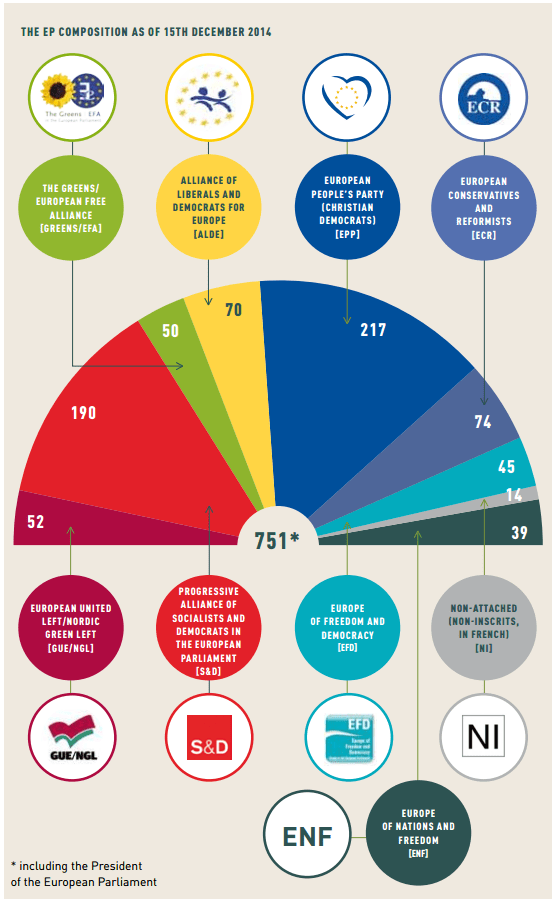

In common with many parliaments throughout the world, the MEPs are also arranged by party affiliation with national political parties banding together with groups of similar ideology such as the Green/European Free Alliance (which includes Green and Regional/Autonomist parties such as the Scottish Green Party, the SNP and Plaid Cymru); The Progressive Alliance of Socialists and Democrats (which includes the Labour party); The Alliance of Liberals and Democrats for Europe (of which the Lib Dems are members); the European Conservatives and Reformists (where the Conservatives, unsurprisingly, find their ideological partners). A study by VoteWatch.eu has found that the group to which a particular MEP belongs is a far greater predictor of voting preference than national identity. MEPs tend to vote on party lines rather than national lines. Though an informal and likely unintentional inclination this, in practice, further serves to dilute the inclination for any particular member nation taking the reigns over the whole continent.

The other major legislative body in the EU is the Council of the European Union (sometimes known as the Council of Ministers) which acts more-or-less as the bicameral segment of the Legislative body and consists of one appointed seat per member state. Unlike the Parliament, however, the person sitting on that seat is decided on a more ad hoc basis depending on the issue being discussed. For example, if a bill on agricultural policy is scheduled then the members may send their national government minister for agriculture. Within the UK this has, on occasion, caused some implication with regard to the structure of devolution whereby an issue which overwhelmingly affects an area either within or controlled by Scotland (for example, fishing) may end up being negotiated by a UK Minister who doesn’t actually have responsibility over that area due to its devolution to the Scottish Government whilst the Scottish government minister who DOES have responsibility may not attend as they are not a member of the national government.

One interesting dynamic within the EU is that whilst the European Parliament and the Council of the European Union votes on whether or not EU laws come into force they don’t themselves generally have the power to initiate legislation (except under very limited circumstances). They cannot themselves propose those laws. Whilst this serves as another check against unbridled power (The President of the Parliament cannot declare themselves Dictator of Europe then have Parliament approve the motion and give them ALL the power) the body which balances this leads us into one of the more maligned and less understood aspects of the governance of the Union.

The Executive Branch of the EU and the area with the power to propose new legislation is the European Commission. Also known as “The unelected, faceless bureaucrats from Brussels”. Yes, it is true that they are unelected by the public (once again, UK citizens should be well used to unelected folk making laws for us. We call them Lords.) but are instead appointed by the national member states, each state taking one chair on the (as of 2016) 28 member council. The UK’s current representative is Baron Hill of Oareford (Yup. Our own unelected, faceless bureaucrat is ALSO an unelected member of the House of Lords. You don’t get much more “British” than that).

The Commission is backed by some 23,000 employed civil servants who do all that background paper shuffling and departmental stuff involved in running a continent spanning government with over 500 million citizens. This said, if that sounds like a lot of people, the UK Government’s civil service (not including devolved administrations) employs some 423,000 people.

The European Commission is also backed by the European Council (not to be confused with the Council of Europe which is a non-legislative body more similar to the United Nations and which helped codify democratic ideals such as the European Convention on Human Rights nor should it be confused with the Council of the European Union). The European Council is, again, a body of 28 members, one each per member state, and is comprised of either the heads of state or heads of government of each of those members. The UK’s representative here is the Prime Minister, currently David Cameron. This body formally exists to “provide the Union with the necessary impetus for its development” and essentially guides the strategic overview and crisis management of the Union as well as allowing an outlet for the overall view and attitudes of the governments of the member countries (although, as previously noted, at the Parliament level political party remains a greater predictor of overall voting intention of individual MEPs).

The Court of Justice of the European Union functions as the Judicial Branch of the European Union and acts to ensure that member states apply agreed treaties and rules within the EU equally, ensure that member states do not pass laws which run contrary to the rules of EU membership and protect the rights of EU citizens under those rules. A good recent example of the functioning of this body occurred when the Court issued guidelines to Scottish and UK courts over the implementation of alcohol minimum unit pricing in Scotland.

Number six in the list of institutions within the EU is the European Central Bank which administers the monetary policy of the Eurozone, the 19 member countries of the EU which are in formal currency union with each other and use the euro as their currency. The euro has been one of the major creative exercises of the European Union in that it is a response to the stated goal of attempting to create financial stability within the Union and to allow as few internal barriers to trade as possible.

There exists a macroeconomic principle known as the “Impossible Trinity” which states that a country cannot completely have free control over internal interest rates and monetary policy, completely fix exchange rates and have free capital flow all at the same time. Historically, many countries kept a stable exchange rate and have kept control of the interest rates but had to tightly control capital flow to do so (Some readers may remember the tourist travel allowances in use up until the early 1970’s).

Many countries, the UK included, now allow capital to flow freely and keep the right to control money printing and interest rates but accept that exchange rates between currencies will now be volatile which will impact the prices of imports and exports to and from that country.

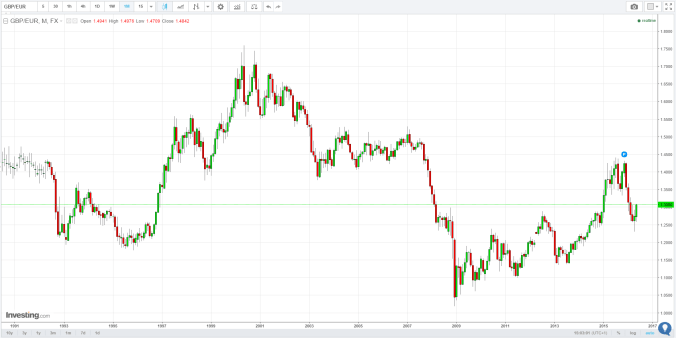

The exchange rate between the £ and € since the latter’s launch.

The Eurozone is an example of an attempt by countries to lock their mutual exchange rates (A euro in France is worth exactly the same as a euro in Germany), whilst allowing capital to flow freely around the continent but at the price of individual countries no longer being able to set their own interest rates or freely increase or reduce their internal money supply.

The system is not without its flaws, of course, (no monetary system can be) and the comparative advantages and disadvantages of monetary union as well as the specific structures of the Eurozone are topics of extremely heated debate (and likely always will be).

Whilst the eventual joining of the Eurozone is expected (although not, strictly, actually enforcably required) of EU members, some members, the UK and Denmark, enjoy a formal opt-out from membership of the Eurozone whilst others, like Sweden, have simply no intention of joining until their citizens demand a referendum on joining. Still others, like newest member Croatia, have stated a desire to join the Eurozone but do not currently meet the strict criteria for entry. (For comparison, even without the opt-out, the UK would also fail to meet the euro convergence criteria unless it could reduce both budget deficit and total debt to GDP ratios by more than a third).

The final institution of the European Union is probably the least sung of all. The European Court of Auditors is a final check and balance within the governance of the union and continuously reviews the spending of the EU’s budget. Once again, its membership is appointed based on one member per member state.

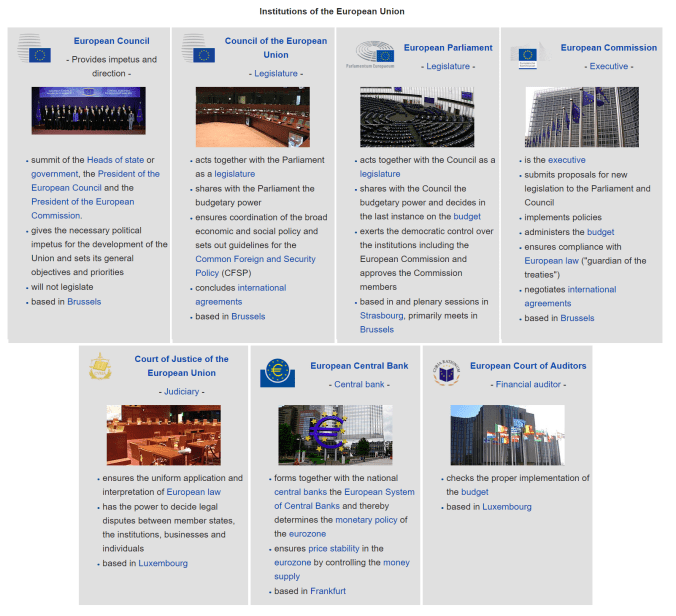

A summary of the Institutions of the European Union and how they interact.

I’m an EU Citizen. What’s in it for me?

From the passing of the Maastricht Treaty in 1992, the concept of EU Citizenship was born and granted to (almost) every citizen of a member nation (for exceptions, see the Youtube video near the top of this article). This citizenship is stated to be supplementary to national citizenship and grants a citizen several rights to do with the EU. These include:

The right to vote in and stand for positions in the European Parliament in any EU state depending on your residence.

The right to vote in and stand for positions in local elections (In Scotland, this means Community Council, Regional Authority and Scottish Parliamentary elections) under the same conditions as nationals of this state. Note that this does not guarantee (but also does not forbid) the right to vote or stand in national elections or referendums which is why EU citizens were permitted to vote in the 2014 Scottish independence referendum (which was a “regional” referendum) but have been blocked by the UK Government from voting in the upcoming EU referendum.

Access to EU Government documents and to petition the EU Parliament, including the right to request information in any of the official languages of the EU and to receive a reply in that same language.

The right to free movement and residence. You may move to and within any EU member nation as freely as one of their nationals and may claim residence there just as freely. You have the right to move anywhere within the EU for the purposes of bettering you standards of living and are not tied to reasons of employment to do so. This right also forms the basis of the Schengen Agreement which removes border controls between participating countries.

Somewhere almost exactly on the Austria-Germany border.

The right to consular protection. One of the lesser known perks of EU membership. If you happen to be in a country which does not host an embassy belonging to your home nation and you are in need of their assistance then you may visit the embassy of any other EU member nation and they will be required to give you the same treatment as they would one of their own citizens. This right is perhaps under-appreciated by British citizens due to the size of the UK’s diplomatic network but there are still countries around the world in which the UK is not represented but in which your EU citizenship would grant you this protection. Examples include the Central African Republic (which has a French embassy), Liberia (In which you would visit the German embassy) and Lesotho (in which Ireland maintains an embassy).

Of all of these personal rights, perhaps the one most under scrutiny and debate within the context of the upcoming referendum is the right to free movement. For some, this is a freedom to move labour to where it is needed and to move and potentially retire and countries with rather more sun than the UK enjoys. For others, it is a gateway for rich nations to be flooded by economic migrants from poorer nations or, worse, for the economically inactive to take advantage of comparatively generous welfare systems and to mooch off the labour of others.

In Part 2: – A Brief History of Brexit, I shall outline the UK’s personal history with Europe and how we got to point of holding the referendum on our membership.