“Let the children once see clearly the gross injustice of our present land system and when they grow up, if they are allowed to develop naturally, the evil will soon be remedied.” – Elizabeth Magie, inventor of “The Landlord’s Game”, the precursor to Monopoly.

For a game about rampant, exploitative capitalism and a race to deliberately bankrupt your mates, in some ways Monopoly looks remarkably egalitarian compared to modern Britain

“Tomorrow’s GDP figures will confirm whether or not Scotland entered a second quarter of economic downturn in the first three months of 2017.” – Scottish Conservatives. 4th July 2017.

The quarterly Scottish GDP figures were released today after a long build up in a press anxious to see if Scotland was on, as the Express put it, the “BRINK OF RECESSION” (their emphasis).

The headline figures are that in Q1 2017, Scotland’s economy grew by 0.8% which is up substantially on the -0.2% contraction seen in Q4 2016. This positive growth also means that the two successive quarters of negative growth which define a technical recession were not met.

The UK’s GDP growth over Q1 2017 was 0.2% though in my last blog post I put substantial attention onto the point that we should treat such comparisons with a great deal of care given the large regional inequalities within the UK. I’d very much like to see the GDP of the UK broken down across its regions (especially London) before commenting too much on it.

And before we all start patting ourselves on the back at avoiding our “predicted” recession, it’s worth actually diving into the numbers and seeing what they do and do not tell us about the Scottish economy.

“Annual income twenty pounds, annual expenditure nineteen nineteen and six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.” – Dickens, David Copperfield

The shape of the next UK economic crisis has become apparent. It may have already begun and it’s not at all clear how it can be avoided or mitigated.

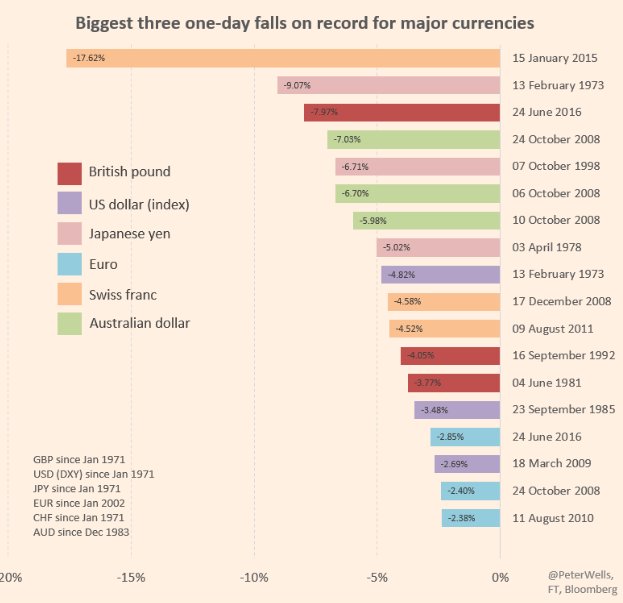

On the 23rd June 2016, the United Kingdom, for a variety of reasons, voted to leave the European Union. The immediate impact of this was an almost unprecedented drop in the value of the pound with respect to its major trading partner currencies.

Not much of a problem, the defenders said, as a weakened currency has its merits as well as demerits. Exports should become cheaper, which would boost foreign trade.

This may have been true in times gone by but economies have grown vastly more complex than this. Many products manufactured in the UK consist of sub-components drawn from multiple countries and globalised supply chains have grown STAGGERINGLY complex.

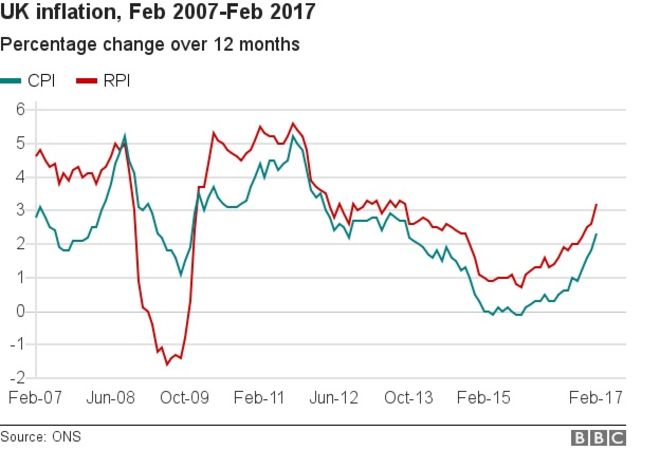

What this has meant is that even the goods that Britain manufactures here have seen their “input prices” increase, which has pushed up the price of goods even despite the fall in currency strength. Add to that, the fact that the UK imports far more than it exports – it has one of the largest trade deficits as %GDP in the OECD – and it becomes clear why prices have started rising again in Britain. After five years of declining inflation rates and almost a year of zero price increases, inflation has returned with a vengeance.

But this needn’t be a terrible thing. In fact, inflation can often be quite useful as it erodes the value of debts (which is why creditors and asset holders hate it so much). So long as wages keep up with the rising prices then for those who don’t depend on the rising value of assets or debts it can be manageable. So how are we doing on that point?

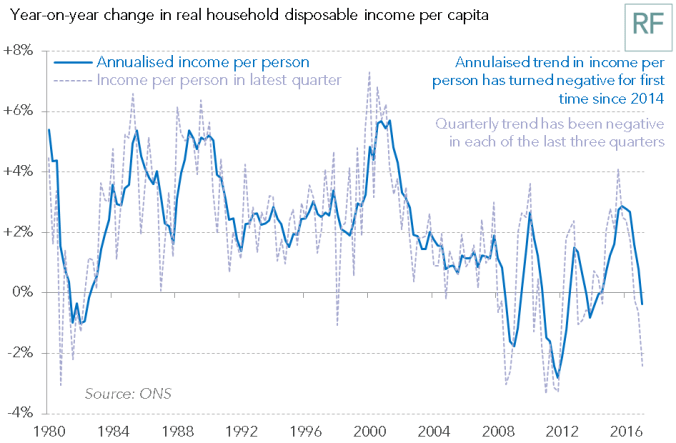

So inflation is rising and wages are declining, so we’re in the situation where meeting our needs and maintain a decent standard of living is becoming more and more difficult. But even this could be mitigated or reversed if the government were to step in and support the economy by investing or by otherwise injecting money into it.

And so this is the root of the coming crisis. Prices are rising, wages are stagnating, savings have been drained, credit cards have been maxed out, and the government is pulling out of the business of providing government and public services so you need to spend even more to replace it. We no longer have enough money to meet our basic needs, never mind the disposable income to buy the widgets we need to consume to keep the wheels of the economy turning.

Up here in Scotland, there are signs that the crisis is already upon us. The Fraser of Allander Institute published a report today warning about the precarious nature of the Scottish economy saying that it was stagnating with relation to the UK economy as a whole. Some will almost certainly be quick to blame this on the Scottish government (the phrase “uncertainty of a divisive second independence referendum” comes to mind). There are certainly some things that the Scottish Government could do to help – a National Investment Bank should be high on the list and a good shake up of the domestic agenda would be welcome – but the ultimate cause of this slow-down does not originate in Scotland nor will its solution come from here (at least until the levers of power are returned to the country upon independence).

The problem, ultimately, is that Britain isn’t Great. Britain is Weird. Britain is a deeply unequal country on a scale which, compared to its neighbours, is utterly baffling.

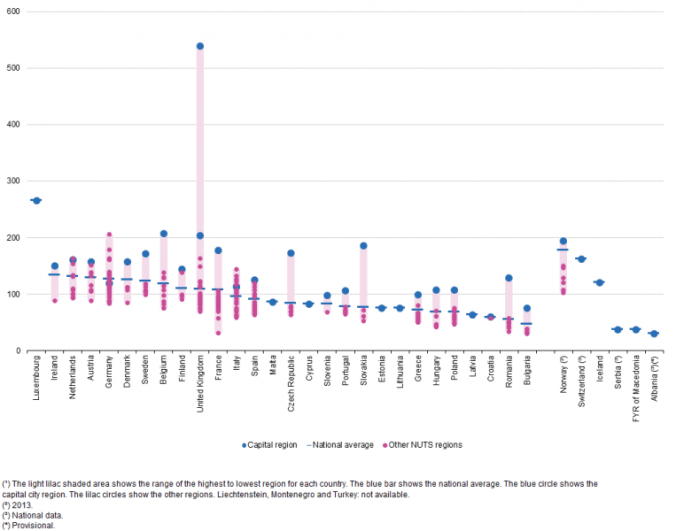

In many countries, the capital city will be the richest region of the nation. This is normal – Money wants to be close to power – but the UK’s disparity really needs to be seen to be believed. Here is the GDP/capita for each of the EU28 and EFTA countries broken down by region. Spot the odd one out.

(Note that the UK has two capital dots. The lower one is London as a whole. The upper one is just Inner London)

Whenever statistics about Scotland are produced, they’re often given with reference to the “UK average” or the “UK as a whole” but the extreme disparity of Britain masks the picture. Detailed analysis by Prof Mike Danson of Heriott-Watt University has shown that Scotland’s GDP per capita is the third highest region of the UK (after London and the South-East) and, if we were an independent state, we’d be the 9th highest in Europe. In fact, we can disaggregate out the Scottish data from the chart above and catch a glimpse what we’d look like as an independent country.

Taken on this view, Scotland no longer looks like a “below average” region of the UK but a fairly normal Western European country. Far more like Finland or Denmark than, say, Greece.

As Prof Danson says, the obsession with comparing Scotland to misleading “UK average” figures leads to commentators ending up unable to take a step back and ask what is happening across and within the UK and where the problems really are. Until this happens, Scotland will continue to stagnate within the UK as the overinvestment of London continues (and is likely to get worse through the Brexit process in a desperate attempt to prop up the financial sector there).

As said earlier, there is a way out of the coming credit crisis but it’s going to involve not more Austerity but a whole lot less. Economists are increasingly coming around to the realisation that the Government’s debt is your surplus and that governments can take on that debt almost without limit (unlike you who have hard limits on credit and the ability to repay it) and – if they have their own currency – can print money in order to provide services (unlike, again, you who would go to jail if you tried that).

Once again, there is a certain amount that the Scottish government can – and should – do at the moment to help but it will always be stymied by the very tight rules of devolution. There’s little to no hope of the UK changing course any time soon (even Corbyn’s Labour is solidly committed to “balancing the budget“) and the hard Brexit the Tories and Labour are both pursuing is being increasingly differentiated by the amount of damage the plans will cause rather than any attempt to prevent it. The Sick Man of Europe seems destined to return to the UK. I only hope that Scotland doesn’t catch its cold.

“Before you can start building [houses] on any scale, every single industry in society has got to be organised and stimulated into production.” – Aneurin Bevan, 1946.

The inferno at Grenfell Tower has claimed many lives (as I write, the official estimate for people dead or missing and presumed dead is 58.), has likely wiped out entire families and will have irrevocably changed an entire community forever.

It’s still too early to be fully deconstructing the causes and blames of this disaster but a few things have become widely reported and will likely play into the debate in the months and years to come.

However the blaze started (early reports suggest a power surge igniting a fridge on the 4th floor) it appears that the flames spread rapidly up the insulating cladding on the outside of the building, engulfing the entire structure in minutes and trapping many inside.

It has also emerged that the cladding involved was the cheaper of two options provided by the supplier and of a construction which would be illegal in several countries including the US and Germany. The fire resistant version of the cladding appears to have cost fractionally more – just £2 per square metre, or £5,000 for the entire block of flats. Further, it appears that at least part of the motivation for the choice of cladding was to improve the appearance of the flats for the benefit of nearby luxury high rises.

The Grenfell Action Group has been warning of a catalogue or failures of construction, maintenance and accountability for years. And the complete failure of leadership in the wake of the disaster, especially from PM May, has been appalling. This interview by MP David Lammy, who lost a friend in the blaze, does much to exemplify the sense of frustration and anger felt by a community which justifiably feels betrayed and it is no wonder at all that protests have occurred (so far peacefully).

Of course, the building contractors will all tell us that they are not to blame as they met all applicable regulations. And they’d almost certainly be correct. This is the nature of the relationship between capitalism and government regulations. It will always be the case that companies will meet regulations by the barest minimum that cost allows and will always lobby for those regulations to be decreased if the cost of lobbying is lower than the savings due to the regulation cut (for, in this case, politics can be reduced to just another form of investment).

I’ve been particularly appalled by one article in Bloomberg which takes on the extreme libertarian approach to this stating that all fire regulations should be scrapped because in the perfect world of the libertarian, any regulation which increases cost is unacceptable. Instead, the people who lived in the tower should have rationally weighed the risks of living in the tower with that cost and, if they wanted to, could have moved to some (presumably more expensive) tower nearby which DID include the safety features.

I shouldn’t need to fully dismantle this worldview. The residents of Grenfell did not have the choice of a hypothetical “safe” building next door into which they could move. Even if they did, humans simply are not the machine-like “rational actors” demanded of libertarianism nor do they always have the perfect information required to make such a choice (Could you identify a flammable cladding from a non-flammable one? If the libertarian landlord tells you, could you completely trust them? Could you tell if they were lying? Without any regulations, how would you hold them accountable if they were?)

I have written before, in less tragic terms, on the need for regulations to go well above and beyond the bare minimum. It will be essential if we wish to meet our targets to reduce energy consumption (which will be good for the environment and save a lot of people a lot of money in heating costs). I now believe it’s time to go much further than this. The private sector will always be an anchor against attempts to increase decent housing stock (especially for the poor) and to get the UK’s housing price inflation under control. It’s time for the government to start intervening and build social housing again.

Unconstrained by the needs to seek profit, the government can apply its own regulations, well above the “legal minimum” if need be, and can do some proper planning to ensure that it’s not just housing that’s being built (this has long been the failure of many projects in the past such as the high rises and the out-of-town blocks such as Easterhouse in Glasgow). We need to think about the amenities and the jobs and all the other functions of a town which enables communities to thrive. Common Weal has recently published some proposals on how local areas can control their own land and ensure that their specific needs are addressed on their terms. We can’t keep treating housing as a commodity for the rich, constantly pushing folk to “climb the property ladder”, treating those who can’t to the slums and the land-baggers and simply abandoning them. We can’t keep segregating people and reinforcing the class and wealth divides and then blaming those on the bottom end for “just not striving hard enough“.

This isn’t to say that high-rises don’t have their place – endless suburban sprawls constantly bite into farmland and wild spaces and often fail to engender any sense of community at all, not to mention the health and climate effects caused by having to drive to reach anything other than your own house and the extra costs of delivering services to low density populations. Smart Cities, well designed with these factors in mind, may be a major factor towards a sustainable future (and I say this as someone who lives in a rural area).

And these cities need a lot of work to build. From brickies and plumbers, through planners and designers, past educators and mentors, to the computer experts who’ll get the smart systems going and keep them running, there is vast potential to employ a lot of people in this enterprise and to inject a huge amount economic activity into the country (in a far more productive manner than the zero-hours “gig” jobs that we’re being fed currently). If Austerity is to be ended, this could be one way to do it. And we know it works because the UK has been through exactly this before. An economy shattered by war from without (rather than Austerity from within) was reconstructed in the 1940’s and 1950’s and is still looked back on fondly as one of the UK’s golden ages. Here’s Nye Bevan talking in 1946 about his plans and how he got them started.

“That’s all great”, you say. “But how much will it cost and how do you pay for it?”

Government debt.

Did that put a shiver up your spine? Then you’ve been indoctrinated by the most dangerous ideas of the 21st century. The idea that government debt is a terrible thing.

We’re living in an age where the UK government can borrow on a 30 year bond for 1.7%. Inflation is currently 2.9%. There has never been a better time to invest as right now the debt is (in real terms) cheaper than free!

Applied to the housing market, this could be a major game changer. Not withstanding the ability to directly target areas which badly need investment (preferably by allowing these areas to borrow themselves through a National Investment Bank), the advantages in cost to the occupier are significant.

Right now, a £90,000, 25 year mortgage on a 4% compound rate would cost you about £475 per month and you’d pay back £142,500 over the term. A mortgage based on a government bond at our 1.7% (simple interest, rather than compound) would pay back over the 25 years for a little over £425 per month and, as a particular advantage to the renter, that monthly rate could be fixed for the entire mortgage period (it needn’t even be uprated for inflation as the bond isn’t). Try asking your bank for a mortgage rate fixed beyond five years. Try asking them to predict what the interest rate will be on year six.

(The Bank of England can’t do it, and they’re the ones who SET the rates!)

One the debt is paid off, it could be up to the government to decide whether the house remains as a social house and the occupier continues to pay rent (thus subsidising other housing), continues to live in their home rent free for the remainder of their occupation (thus preserving communities long term), or allows them to purchase the house (which would require the government to replace stock in a way that wasn’t done under Right-To-Buy)

And, of course, you can adjust the numbers as required to ensure that everyone can afford a house, built to far higher standards than the private sector will supply, without the need to make obscene levels of profits while doing so and in a location and surrounded by the services required to make that house a home embedded in a community built by and for all of us.

We didn’t need the Grenfell tragedy to have this conversation. People have been speaking about it for years now. The systemic problems in the UK’s housing industry have been apparent and have been either ignored or actively encouraged for too long. Maybe it’s time we started listening and reassessing.

I don’t recall ever having been so conflicted about a vote than I am about the upcoming general election. This week’s interviews of Theresa May and Jeremy Corbyn did little to help with that.

As a brief review of the interviews themselves. I think Corbyn came across as quietly and surprisingly firm and upright. He had successfully anticipated the questions from both the audience and from Paxman and gave solid, if obviously rehearsed and briefed, answers. The perception of him in the press is that his policies are popular but his own personal factor is rather less so. Paxman attacked that weakness and went for the personal and tried to drag, sometimes fairly; sometimes unfairly, his already well aired skeletons out of their closets. Comparatively few questions from him were on policy. Corbyn probably came out as well as he could in the face of that.

May, on the other hand, showed why she’s been trying hard to run a Presidential campaign without actually appearing in front of people. Evasive and vague answers to questions and defenses of abysmal policies being literally laughed down. One question which particularly struck me was from the older gentleman who was very upset at the prospect of losing his house to pay for social care. Equally striking that when he was asked about it after the debate he admitted that while he was unhappy with the answer, he’d probably still vote for May. This is the calculation she’s made through this whole election campaign. She knows younger folk won’t vote for her (and – hopefully, from her POV, won’t vote at all) but she’s gambling that older voters won’t NOT vote for her (and will certainly turn out). If either or both of these assumptions turn out to be incorrect, she’ll be in for an abrupt surprise on June 9th. It seems incredible to say but my estimates of the impending Tory majority have dropped from 100+…to 6 points in some recent polls.

The whole debate was neatly summed up in a couple of tweets.

So why my conflict?

I don’t have a Green candidate to vote for in my constituency. Between cost, the inherent unfairness of FPTP with regard to smaller parties and a few other factors, we don’t have a candidate for the area and so my vote is up for grabs.

If I lived in England and couldn’t vote for the GPEW, it’d be a fair no-brainer. I’m actually excited by much of the Labour manifesto. Items like the program of nationalisation, the National Investment Bank, and their previous support for a scheme to look at a Universal Basic Income (though it hasn’t made it into the actual manifesto) are all policies that the Greens and Common Weal support and advocate for.

This isn’t to say that the manifesto is perfect. There have been compromises there to keep the ever recalcitrant PLP in line. Corbyn has all but admitted that he doesn’t like not being able to change the party stance on Trident and I certainly do not appreciate the manifesto’s stated opposition to Scottish independence. While reports more recently have somewhat softened that, i’d think it likely that he’d go into that negotiation from a stance of either offered Federalisation or finding some other way to try and “buy off” the nationalists rather than support a referendum.

But this isn’t the largest blocker towards my placing my vote in the Labour box. Quite frankly, I don’t trust Scottish Labour and Kezia Dugdale to support anything that Corbyn offers. Certainly not if opposing Corbyn helps them with their sole and over-riding goal of opposing the SNP at every possible avenue. I could believe that Corbyn would seek a coalition with the SNP to oust the Tories. I could equally believe that Dugdale would sabotage it to frustrate Sturgeon.

So my vote should go SNP then? Well…I can’t say I’m entirely impressed with their manifesto. There’s some good stuff in there – commitment to energy grid reform and the general pushback against Austerity is decent – but there’s a lot missing too. The SNP have been clearly outflanked on the National Investment Bank issue. They could have placed a commitment in there on that with the sweetener that they’d push for it in Scotland even if they couldn’t win power in Westminster. As a negative, I don’t like the continued push towards Carbon Capture – especially now that Scotland is free of coal power. As a technology, it’s looking more and more like another distraction from decarbonisation at best and an excuse to develop technology for ever more oil extraction at worst. The lack of push on corporation tax beyond “opposition to further cuts” is also disappointing.

This last concern brings me to another point. I’m struggling to see the balance between the overall promises to end Austerity and the commitment to “balancing the budget” within the next five years. When asked directly at their manifesto launch about whether these promises were costed, Nicola Sturgeon didn’t give a particularly straight answer. I think the party is still caught in the trap of believing that government deficit spending is a “bad thing” and that we can just grow our way to economic “success”. There are some very good reasons to believe that this economic model is badly flawed.

Overall, this is clearly a manifesto built for a party which knows it can’t win any more seats than it already has and is trying to avoid losing too many. It’s also clearly a manifesto written without much intent of being implemented. The party rhetoric has consistently been one of assuming a Tory majority in which Scotland’s MPs would be ignored.

Away from the national campaign and down to the local I’ve been having a look at who is standing in my own constituency. It’s currently an SNP seat with the Tories in a very distant second. Even if the Tories pick up every single non-SNP voter, they’d still be shy some 7,000 votes. This probably explains why, a week and a half out from the elections, I haven’t seen a single piece of campaign literature from anyone and why my choice of candidates have been…let’s say “less than stellar”. We have the incumbent MP (whom I do like and respect). The Lib Dems and UKIP are both running one of their recently failed council election candidates and, rather more seriously, the Tories and Labour are both running one of their recently ELECTED councilors. I can’t help but think that they’re not taking this election particularly seriously.

So that’s my dilemma. In terms of manifestos, I’m probably most attracted to Labour’s but their opposition to independence and my lack of faith in Scottish Labour’s commitment to their own party is a serious concern. Whilst I’m not quite so enthused by the SNP promises and they look more like a list of nice things than a complete vision of a country, I can more easily believe that they’d work towards them given the chance and that, at heart, they will be thinking of Scotland when making inevitable compromises.

I need to throw things out for advice. To the SNP – I’m yours to lose. Convince me that your numbers add up and you’re trying to build something more than just a list of nice soundbite policies. To Labour – I’m yours to win. Convince me that your party still has a place in politics north of the border.

“We bailed out the City 10 years ago when the crash came, we poured hundreds of billions of pounds into it. Since then £100bn has been given out in bonuses in the City. So we are asking for a small contribution…to fund our public services.” – John McDonnell MP

Last night, Labour announced one of their keynote policies ahead of the 2017 General Election. A financial transaction tax on the City of London. Time for a blog to outline just what in the name of Jim it actually is and what it’s supposed to do.

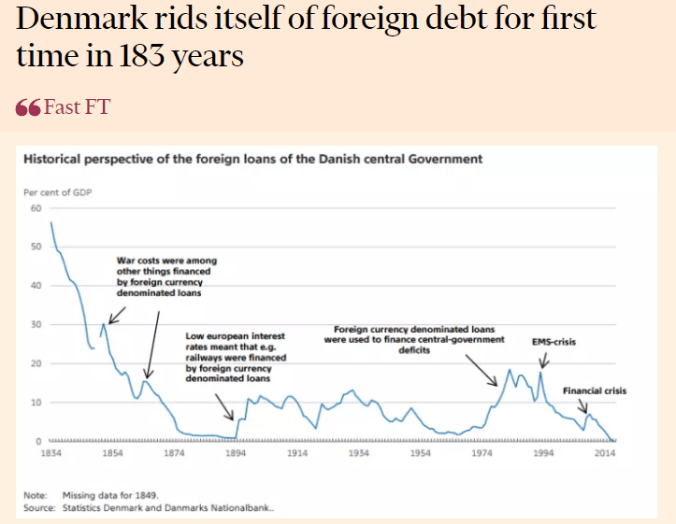

There’s an interesting wee story doing the rounds that moment regarding Denmark and their foreign debt.

I’ve seen a few folk get a bit over excited about the story and have misinterpreted it as saying that Denmark is now debt free. First up, it’s not. Their national debt is at about 38% of GDP (compared to the UK’s 85.4%). This isn’t about the Danes paying off all of their national debt, it’s just saying that they no longer have any debt which is denominated in foreign currencies. All of the Danish national debt is, for the moment, denominated in Danish krone.

There’s a more interesting story under here about why it has happened though. It’s the story of managing one’s currency and maintaining a currency peg with regard to another. This is something that folk in Scotland should be watching closely as our own debate about currencies heats up again.

Not long ago I wrote an article on defending one’s currency against speculative attacks but many of the lessons also apply to more gradual changes in currency value and the effects are being borne out in Denmark as we speak.

Recently the instability in the Eurozone and reduction in confidence in the euro has seen investors selling euros and buying krone, seeing it as a safer investment. This is pushing up the value of krone which, if it was freely floating, would affect the exchange rate between it and the euro. But Denmark seeks to maintain a stable exchange rate between the krone and the euro (At a rate of 7.46038 DKK/EUR ± 2.25%) so its central bank must intervene to prevent the rise in value. It does this by cutting interest rates (to make further purchases less attractive) and selling DKK and buying foreign currencies. This influx of foreign currency has allowed it to pay off foreign denominated debt but has also caused its foreign reserve holdings to boom from 200,000 million krone in 2008 to over 400,000 million krone today.

If the opposite case had been true, if the DKK was weakening with respect to the EUR, we might expect the levers to be pulled in the opposite direction. Interests rates would increase to attract investment and foreign reserves would be drawn down as foreign currencies were sold to buy up krone holdings and support the value of the currencies and we might see the central bank issue bonds marked in foreign currencies rather than paying them off.

It may well be that Denmark can continue do defend its currency peg for some time, although some have eyed the possibility of a break similar to the one Switzerland went through in January 2015. A couple of years on from the Swiss break the risk of Denmark following suit appears to have receded for the moment.

All in Denmark – currently the 2nd happiest county on Earth – is showing what happens when a small country of 5-and-a-bit million people, its own currency and the will to manage it can do and whether or not Scotland specifically chooses a path similar to this (by pegging a £Scot to the GBP or, indeed, the EUR), Denmark should be taken as an example of what can be done. A small island of light and clarity in a world where the people of Scotland are about to be told repeatedly and in detail what some folk think we can’t do.

“[I]f there is to be meaningful debate on this issue then the SNP have a lot of work to do to produce best possible data. The last thing they should do is trust that from London.” – Richard Murphy

Tax expert Richard Murphy, who is currently most notable for exposing the UK’s massive £120 billion per year tax gap, has written an article warning of relying on UK economic data to make the case against Scottish independence.

Before he gets attacked too badly by hacks telling him that the Scottish economic data is produced by Scottish civil servants (Edit: I may already be too late on that) I thought I’d write a parallel piece pointing out what those civil servants have told me about the limits of some of their stats.

The first thing to remember in all of this is that the UK is not a federation or a confederation, it considers itself to be a unitary state of which Scotland is just one region of twelve (plus the “extra-regio” offshore regions). Therefore there is currently no real obligation to even gather the distinct statistics for Scotland and it really only has become important because of the independence campaign.

Tax Revenue

As I’ve pointed out in my paper Beyond GERS, the issue of apportioning tax revenue is fraught with subtle difficulty. GERS itself has updated its methodologies multiple times over the years (particularly since the SNP took the government in 2007. The GERS of today is no longer very closely related to the GERS created by Ian Lang to discredit Scotland in the early ’90’s). There are still differences in the results presented straight by HMRC and the data eventually “Scottishised” [To use the stats folk’s term] and presented in GERS.

Onshore corporation tax is a good example of this. Where an overall UK stat may simply count the location of the HQ of a company for the purposes of assigning corporation tax and this may make sense from a unitary state perspective (albeit this is becoming less true as globalisation increases the ability for multi-national companies to move resources across borders).

For many companies though, the profits one which corporation tax are paid are not generated at the HQ. This is obvious in the case of, for example, a large retail chain which has stores across the country. To correct for this, HMRC and GERS both use different methodologies to apportion the tax more evenly. Various measures (and the weighting applied to those measures) such as estimating volume of sales, number of employees, amount of capital spent in the region and overall population are all used in different ways to reach slightly different estimates. As a result, HMRC estimates that in 2015-16 Scotland produced 7.1% of the UK’s corporation tax compared to 7.3%% estimated by GERS – a gap of about £100 million.

One can also see possible limits of these methodologies especially if taken individually. For example if one looks at employees then one could probably consider a company (and, it should be stressed that this is a completely hypothetical company) which employs a dozen people in Scotland to make, say, a high value, highly exportable product with a geographic link (call it a similarly hypothetical product like “Scotch blisky”) and then employs a couple of hundred people in London to market it. It may be very difficult to properly apportion the “value” of that product and its profits based on employees alone. It’s possible, after all, to find a market without marketing but a bit harder to drink an advertising campaign.

VAT is another issue where these figures can differ for similar reasons. The UK doesn’t demand point of sale ID to determine the location of VAT spend (If you nip down the road to Carlisle for your shopping, then that results in VAT paid in England but Tesco neither knows nor cares where you came from to get there). Again, various methodologies are used to try to estimate the proportions paid and the estimates are slowly aligning (HMRC claims Scotland paid 8.4% of the UK’s VAT compared to GERS’ 8.6% – a gap of £110 million). There is also a further complication wherein the results between HMRC and GERS are simply presented in a different manner (HMRC measures the cash receipts, GERS measures the accruals)

A third prominent example is Income Tax, and is going to become pertinent now as IT is largely devolved to Scotland and all Scottish residents are to be assigned a distinct Scottish tax code and especially now that the income tax bands in Scotland will soon start to diverge from the UK bands. However, HMRC has been recently criticised for a series of administration issues which is making it difficult to roll out this tax code. As with the difficulties in rolling out devolved welfare, this won’t be nearly so much of an issue once Scotland is independent but highlights the difficulty in trying to run a devolved situation from a centralised unitary setup. This said, both HMRC and GERS arrive at a proportion of about 7.2% of the UK’s income tax coming from Scotland although this may change as the new systems are launched (even if tax rates are kept the same).

It is not possible to say whether the HMRC or GERS estimate is “better” or “worse” than the other. The Institute of Fiscal Studies has commented saying, especially of corporation tax:

“Neither of these estimates is clearly superior to the other, and both may be some way off. Profits are not necessarily generated in proportion to the number of employees, or their wages. Some employees may be more instrumental in generating profits than others; and profits also arise from capital assets – both physical (such as buildings and equipment) and intangible (such as intellectual property and brand value) – the location and contribution of which may differ from the location and wages of employees. Calculating how much of a company’s profits are attributable to economic activity in different locations is conceptually and practically difficult and is the source of many problems in international corporate taxation”

Balance of Trade

This is the big one that has attracted a lot of shouting in the past few months. Once again, the UK’s status as a unitary state causes much of the furore over the published numbers to be based on false premises and over-massaged numbers. The UK’s balance of trade figures are published here and probably do do a decent job of estimating the UK’s position in the world. What it doesn’t do is show the internal movements of trade within the UK. As a unitary state it simply doesn’t matter to the external balance of trade whether or not Yorkshire is a net exporter to Sussex. The UK does produce figures which try to estimate the trade balance between the regions with the rest of the world but it only covers goods, not services (hence excludes nearly half of the UK’s total trade) and it does not cover internal trade. For that internal trade, we turn to ESS – Export Statistics Scotland – which surveys exporting companies in Scotland and asks them where they send their goods and services (contrary to a semi-popular belief, these statistics don’t care how the goods reach their destination so it doesn’t matter if they physically leave the UK via an “English port“). There are some limits, again, to this methodology.

First, not all companies know where their goods are going (see the example of Tesco again. If someone from Carlisle buys a crate of beer in Glasgow then goes home then that’s a Scottish export but Tesco wouldn’t be able to record it easily) so they won’t appear in the survey. Goods which are shipped to England then either re-packaged or used as a sub-component before being exported from England to somewhere else (or even back to Scotland) would be counted only as far as their export to England and there may be some cases where service “exports” are caused by, for example, someone in London buying insurance for their house in London from the London branch of a provider who just happens to have a brass plate in Edinburgh. The total proportion of these anomalies in the data is simply unknown at this point and unlikely to be knowable until after independence.

Beyond the Horizon

And this takes us to the most important point in this whole article. Even if the methodologies above all align and all can capture the full economic picture of Scotland and everyone can agree on the figures produced and everyone agrees that they produce an accurate and complete picture of Scotland’s economy within the Union there is a fact which should be utterly indisputable (and certainly is within the team which put together these stats).

Independence. Changes. Everything.

None of these figures have any validity if you try to use them to project beyond the independence horizon. Corporation tax may change due to the redomiciling of businesses post-independence. Both those seeking to remain within the UK and those seeking to remain within the EU or EEA may shift operations. Trade exports may suddenly become a lot easier to assign (whether there’s a “hard border” or not) and that “extra-regio” oil which is often excluded from stats due to historical and supply chain accounting issues suddenly has to be accounted for. Those tax streams which are simply too embedded to discuss in any terms other than by a population share have to be audited. And all of this is before Scotland starts to make changes to the tax system to optimise it for the Scottish economy or to do things like close the tax gap.

As with everything in science and in economics, statistics are based on models, models are only ever as strong as their underlying assumptions and projections are only ever as strong as the person making the prediction’s understanding of the limits of those assumptions and the models.

(One day I’ll write an article about the “Porcupine Plots” which get created when inappropriate models are used year after year in spite of reality)

I don’t mind discussing the economy of Scotland within the Union. I don’t even mind speculating on the economy of an independent Scotland. But I sense that the next two years of campaigning will get very frustrating if pundits continue to stretch their own models past the point of credibility in a quest to push their political point. This, I should warn, goes for both sides. We need a more meaningful economic debate than we saw last time. Let’s get beyond the headlines to create one.

“We haven’t commissioned to the best of my knowledge any independent research of our own. If committee wishes me to look at that, I will certainly consider that absolutely.” – Derek Mackay on the Government’s (lack of) analysis into the proposed ADT cut.

The Scottish Government put out a call for evidence for their proposal to cut and eventually eliminate air passenger duty (or, as it’s now going to be known, Air Departure Tax).

Common Weal duly obliged and updated our previous work on the topic to account for the impact of Brexit. You can read the new report here or by clicking the image above.

It’s just as well that we’ve done this as it has since been reported that the Government itself has done precisely zero economic analysis of the impact of the tax cut and, as it turns out, our report is the only economically based submission which is against the tax cut (The RSPB have submitted an objection on the grounds of a very well founded environmental impact analysis). More than half of the other submissions and the bulk of those in favour of the cut are from companies and groups within the airport and airline industry. There is a great deal of concern that unless the government does pull its weight and do the maths itself then this policy could pass through simply on the say so of those who stand to benefit directly from the tax cut and at the expense of those who will lose out due to the impact on tourism and the lost revenue to public services.

Don’t want to read 2600 words? Twitter version: None of the things people say will be hard are. Few are talking about things which will be.

Only in the madhouse world of UK politics that a government which is actually embarking on the process of taking Scotland out of the EU against its will while claiming that this would be a wonderful thing could somehow contrive to simultaneously try to sell us that line that an independent Scotland would be out of the EU against its will and that would be terrible.

Whilst this is going on, the same several year old phony war surrounding Scotland’s membership of the EU continues with a great many people still claiming that we would a) be forced to join the euro and b) Scotland would be punted to the back of the accession “queue” doomed to wait till all other potential members (including, possibly, Turkey) have joined before we’ll get a look in.

This week has seen the publication of a couple of commentators on Scotland’s precise position regarding our EU membership, independence and the interaction with Brexit which has sent every man and their dug howling at the moon and trying to spin themselves into position to get another shot in.

So lets take the opportunity here to take a slightly more sober, honest and open look at how things work in the EU and plot out a couple of likely (that is, actually possible) pathways from which Scotland goes from here, through Brexit and independence and to an independent Scotland within the EU.